Up to date on March twenty ninth, 2024 by Bob Ciura

Buyers searching for high-quality dividend progress shares ought to focus, partly, on corporations that preserve lengthy histories of dividend will increase.

Regular dividend raises from 12 months to 12 months, whatever the financial local weather, is an indication of an organization with sturdy aggressive benefits and long-term progress potential.

With that in thoughts, yearly, we evaluate every of the Dividend Aristocrats, a gaggle of 68 corporations within the S&P 500 Index, with 25+ consecutive years of dividend will increase.

You possibly can obtain your copy of the Dividend Aristocrats record, together with necessary metrics like dividend yields and price-to-earnings ratios, by clicking on the hyperlink under:

Disclaimer: Certain Dividend just isn’t affiliated with S&P International in any means. S&P International owns and maintains The Dividend Aristocrats Index. The knowledge on this article and downloadable spreadsheet relies on Certain Dividend’s personal evaluate, abstract, and evaluation of the S&P 500 Dividend Aristocrats ETF (NOBL) and different sources, and is supposed to assist particular person buyers higher perceive this ETF and the index upon which it’s based mostly. Not one of the info on this article or spreadsheet is official knowledge from S&P International. Seek the advice of S&P International for official info.

The following Dividend Aristocrat within the collection is healthcare large Medtronic (MDT).

Medtronic has a powerful historical past of dividend progress. The corporate has elevated its dividend for 46 years in a row. With an roughly 3.2% yield, Medtronic just isn’t precisely a high-yield inventory.

Nevertheless, the inventory’s yield continues to be increased than the common yield of the S&P 500.

And, Medtronic usually raises its dividend at a excessive price every year, due to its robust earnings and management place inside the medical units {industry}.

These qualities make Medtronic a sexy dividend progress inventory for long-term buyers.

Enterprise Overview

Medtronic was based in 1949 as a medical gear restore store by Earl Bakken and his brother-in-law, Palmer Hermundslie. At this time, Medtronic is likely one of the largest healthcare corporations on this planet.

Medtronic PLC is the biggest producer of biomedical units and implantable applied sciences on this planet. Medtronic at the moment has 4 working segments: Cardiovascular, Neuroscience, Medical Surgical, and Diabetes.

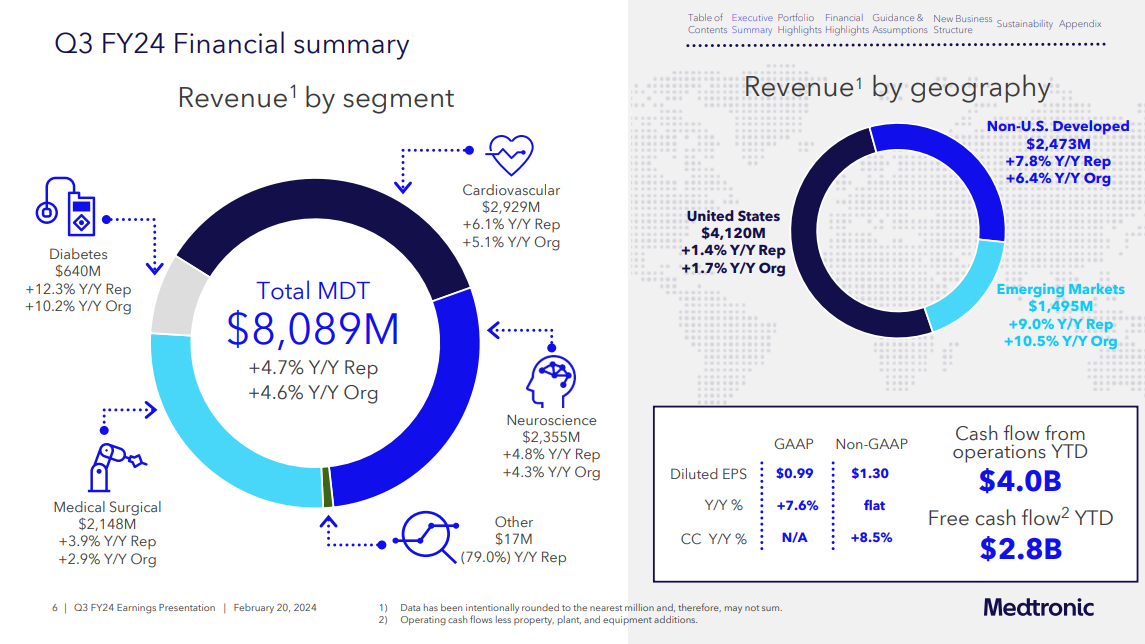

In mid-February, Medtronic reported (2/20/24) monetary outcomes for the third quarter of fiscal 12 months 2024.

Supply: Investor Presentation

Natural income grew 5% over the prior 12 months’s quarter due to broad-based progress in all of the 4 segments. Earnings-per-share remained flat at $1.30 attributable to an -8% foreign money headwind however exceeded the analysts’ consensus by $0.04.

Because of improved enterprise momentum, Medtronic raised its steering for fiscal 2024. It expects 4.75%-5.0% natural income progress (vs. 4.75% beforehand) and earnings-per-share of $5.19-$5.21.

Progress Prospects

Medtronic is investing in progress, each organically through R&D and thru acquisitions. The primary catalyst for Medtronic is the getting old inhabitants. There are ~70 million Child Boomers within the U.S., these aged 51-69 years. Hundreds of persons are getting into retirement day by day. Mixed with longer life expectancy and rising healthcare spending, the working surroundings may be very engaging for Medtronic.

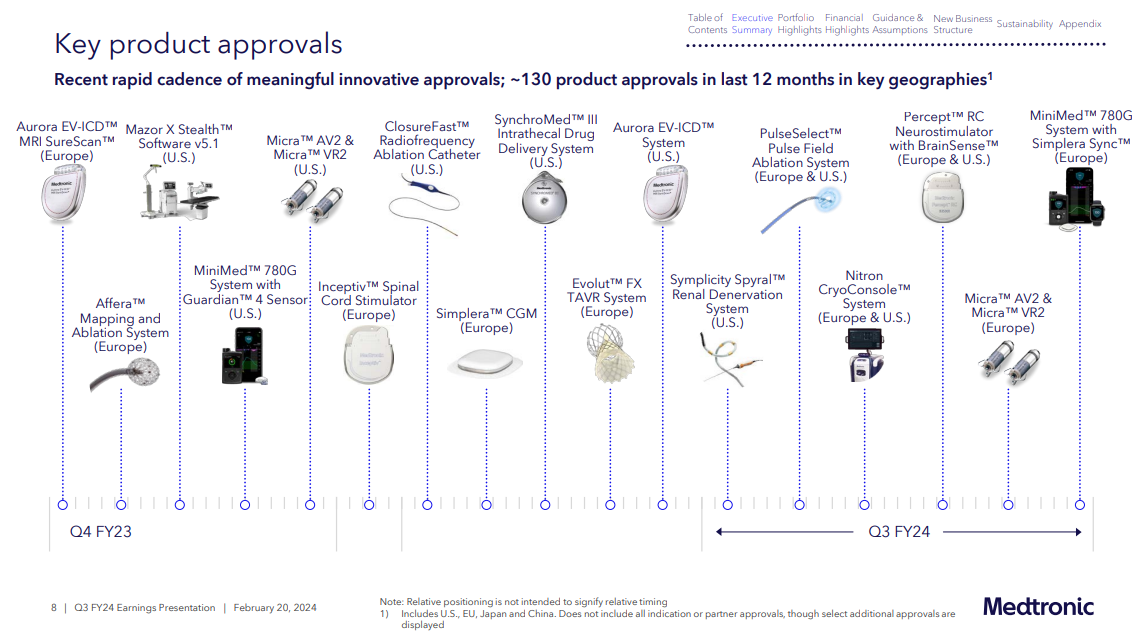

The corporate has had many regulatory product approvals prior to now 12 months. The brand new merchandise ought to drive progress, permitting the corporate to take care of and even achieve market share.

Supply: Investor Presentation

Medtronic additionally has a serious progress alternative in new geographic markets. Particularly, Medtronic has a presence in a number of rising markets, equivalent to China, India, Africa, and extra. These international locations have giant populations and excessive financial progress charges.

Medtronic’s rising market income has constantly grown at a double-digit price for a few years. Whereas the U.S. at the moment accounts for simply over half of Medtronic’s income, rising markets are rising sooner.

Medtronic is buying tuck-in acquisitions and has spent greater than $3.3 billion on 9 acquisitions since 2021. These corporations embrace Acutus Medical, Medicrea, RIST, Avenu Medical, Companion Medical, Sonarmed, intersect ENT, AFFERA, and AI Biomed.

Total, we count on Medtronic to develop its earnings-per-share by 7.0% per 12 months on common till 2029.

Aggressive Benefits & Recession Efficiency

The primary aggressive benefit for Medtronic is its analysis and improvement capabilities. The corporate spends closely on R&D every year, which supplies it with product innovation. Medtronic’s R&D investments over the previous few years exceed $2 billion every year.

The results of all this spending is that the corporate has an enormous mental property portfolio with almost 86,000 awarded patents. This reality has allowed Medtronic to construct a robust product pipeline throughout every of its enterprise segments.

As well as, Medtronic advantages tremendously from its world scale. The corporate operates in over 140 international locations world wide. It has the operational flexibility to generate industry-leading revenue margins, which helps gasoline its progress.

One other aggressive benefit for Medtronic is that it operates in a defensive {industry}. Customers usually can not forego medical therapies, even when the financial system is in recession.

Medtronic’s earnings-per-share through the Nice Recession are as follows:

2007 earnings-per-share of $2.61

2008 earnings-per-share of $2.92 (12% improve)

2009 earnings-per-share of $3.22 (10% improve)

2010 earnings-per-share of $3.37 (5% improve)

Medtronic had the uncommon achievement of earnings progress every year through the recession. The corporate additionally confirmed exceptional energy through the pandemic. This demonstrates its recession-resistant enterprise mannequin.

Medtronic ought to have the ability to proceed rising its dividend every year in each financial recessions and expansions.

Valuation & Anticipated Returns

Based mostly on the latest share value of ~$87 and anticipated earnings-per-share of $5.20 in fiscal 2024, Medtronic inventory trades for a price-to-earnings ratio of 16.7. The inventory’s present valuation is under that of the broader S&P 500 Index and modestly under its long-term common.

Within the final decade, shares of Medtronic have traded palms at a median price-to-earnings ratio of 17.0. We consider that it is a honest valuation baseline.

Consequently, Medtronic shares look like barely undervalued at present. If the inventory valuation expands to our honest worth estimate by 2029, the corresponding a number of growth will enhance shareholder returns by roughly 0.4% per 12 months over this era.

We count on 7% annual earnings progress for Medtronic via 2029, and the inventory has a 3.2% dividend yield. There may be loads of room for continued dividend will increase every year.

With a dividend payout ratio of simply over 50%, and a constructive earnings progress outlook, Medtronic ought to proceed its streak of annual dividend will increase.

Whole returns would encompass the next:

7.0% earnings progress price

0.4% a number of growth

3.2% dividend yield

Medtronic is predicted to return 10.6% yearly over the subsequent 5 years. That is a sexy potential price of return, giving the inventory a purchase ranking.

Ultimate Ideas

Medtronic has nearly all the qualities dividend progress buyers ought to search for. It possesses a extremely worthwhile enterprise, a management place in its core markets, and long-term progress potential. It additionally has a number of catalysts for future progress and the flexibility to continue to grow its dividend even throughout recessions.

Medtronic has elevated its dividend for greater than 4 a long time, which is very spectacular given the continued headwinds from a tricky macroeconomic surroundings.

Medtronic inventory seems to offer a compelling funding alternative for long-term dividend progress buyers.

Moreover, the next Certain Dividend databases comprise probably the most dependable dividend growers in our funding universe:

Should you’re searching for shares with distinctive dividend traits, take into account the next Certain Dividend databases:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

")