Wall Road have been little modified final Friday amid subdued strikes within the Treasury yields, whereas the US greenback noticed additional firming (+0.3%) following latest sell-off. Some reservations proceed to linger round mega-cap tech shares forward of a number of key earnings this week within the likes of Alphabet, Microsoft and Meta Platforms, as latest releases from Netflix and Tesla recommend that earnings expectations could also be priced near perfection. Overbought technical circumstances and ‘excessive greed’ sentiments as proven from the CNN Concern & Greed Index could name for some cooling within the latest equities rally, though the broader pattern nonetheless leans in the direction of an upward bias.

The beginning of the brand new buying and selling week may doubtlessly result in some indecision, earlier than volatility picked up on the onslaught of massive tech earnings and the FOMC assembly in the direction of the latter half, alongside conferences from the European Central Financial institution (ECB) and the Financial institution of Japan (BoJ). Up right now, a collection of world flash buying managers index (PMI) information will probably be on watch, with consensus largely for world financial circumstances to remain comfortable.

With the pick-up within the US monetary sector these days on earnings releases (XLF +3.1% over previous week), maybe one to observe would be the SPDR S&P Regional Banking ETF, which has just lately damaged above the neckline of an inverse head-and-shoulder formation. The neckline projection suggests an eventual goal of the 56.10 degree, with instant resistance to beat on the 46.94 degree for now. Rising shifting common convergence/divergence (MACD) and a transfer above its 100-day shifting common (MA) appear to assist some upward momentum in place.

Supply: IG charts

Asia Open

Asian shares look set for a optimistic open, with Nikkei +1.32%, ASX +0.04% and KOSPI +0.27% on the time of writing. Chinese language equities have been searching for their footing final Friday, with the Nasdaq Golden Dragon China Index eking out a 0.4% achieve, following a 0.8% up-move within the Dangle Seng Index within the earlier session. Current stimulus measures to spice up consumption of vehicle and electronics gadgets failed to offer a lot conviction that they are going to be enough to uplift the downbeat development circumstances, with mounting hopes on the China Politburo assembly this week for extra follow-through.

Nearer to dwelling, Singapore’s client value index (CPI) will probably be on the radar right now, with additional moderation in pricing pressures prone to be the story. Headline inflation is predicted to ease to 4.6% from earlier 5.1%, whereas the core side is predicted to move to 4.2% from the earlier 4.7%, general reflecting some progress in inflation and supply room for an prolonged pause in tightening from the Financial Authority of Singapore (MAS).

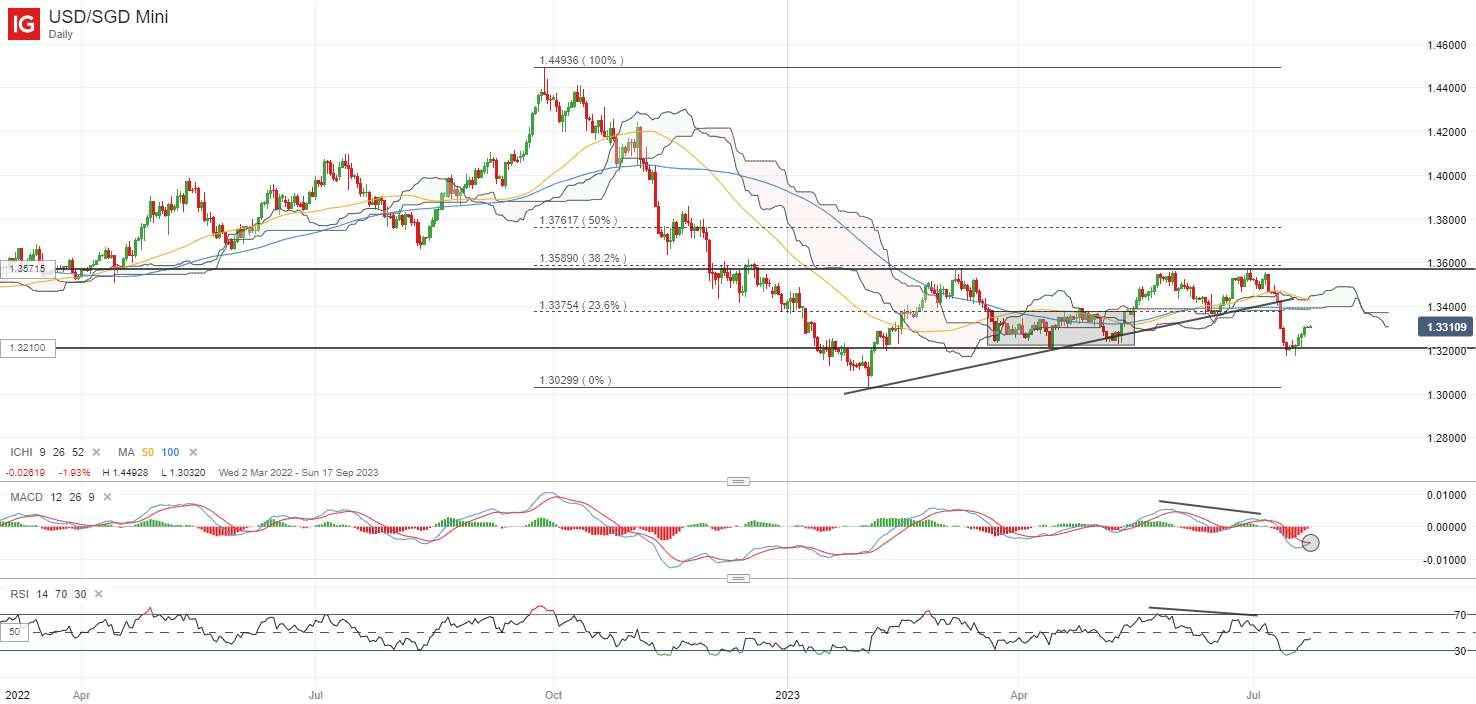

The USD/SGD has been largely buying and selling inside a rectangle sample because the begin of the 12 months, just lately searching for assist off the decrease base on the 1.320 degree. A bullish crossover on MACD and growing RSI could level to near-term upward momentum as a reversion from oversold technical circumstances performs out, however the broader consolidation sample may nonetheless level in the direction of wider indecision. Close to-term, any softer-than-expected learn in inflation determine may doubtlessly go away the 1.338 degree on watch as instant resistance to beat.

Supply: IG charts

On the watchlist: Gold costs on watch in lead-up to FOMC assembly this week

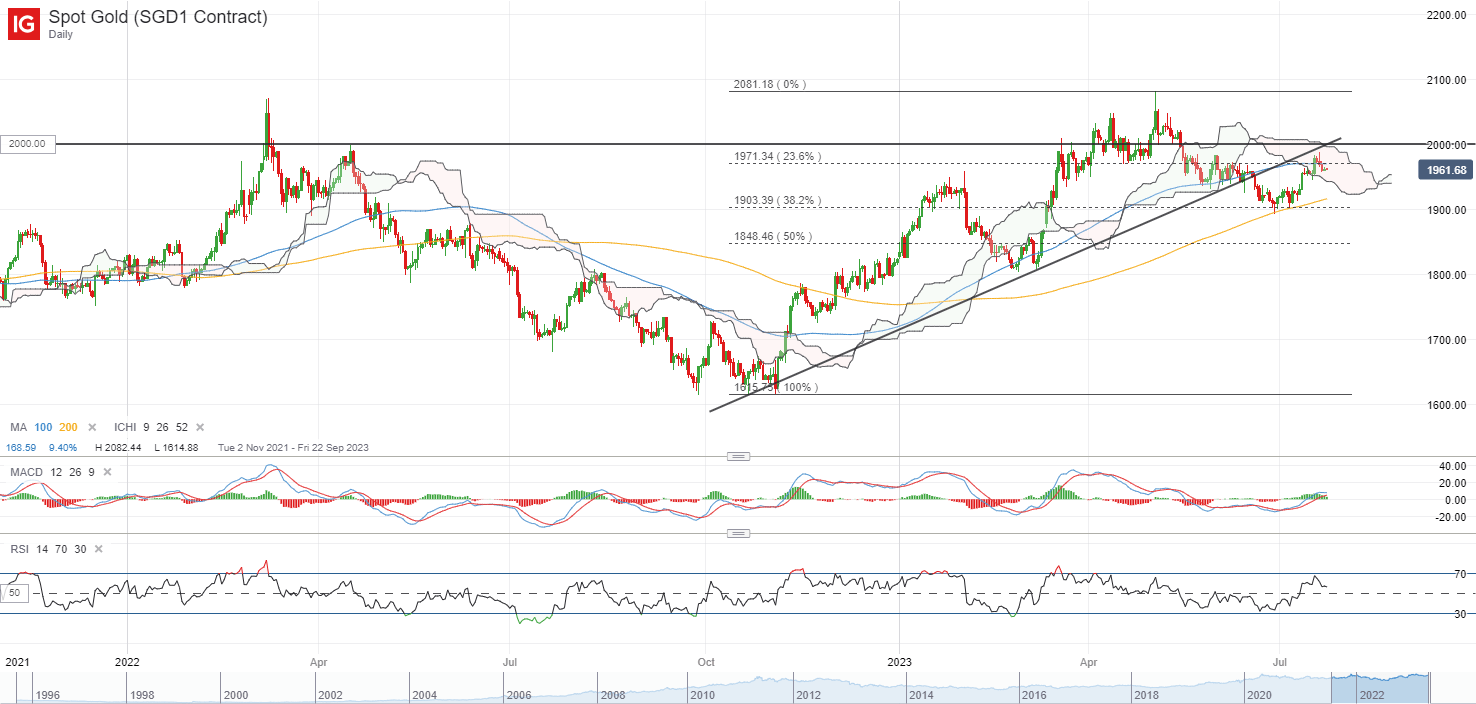

Into the FOMC assembly this week, expectations have been priced for the Fed to ship its final 25 bp fee hike earlier than a protracted pause in its mountain climbing cycle by the remainder of the 12 months. Any emphasis on a extra data-dependent stance from the Fed on the upcoming assembly could possibly be considered as much less hawkish, which can support to restrict the draw back for gold costs. To date, gold costs have recovered as a lot as 4.5% in July on a softer US greenback and decrease Treasury yields, however are going through some resistance on the US$1,980 degree.

The latest CFTC information has revealed a pointy build-up in net-long positions amongst cash managers to its two-month excessive final week (135,907 contracts, up from 100,619 contracts the week earlier than). For now, its weekly Relative Energy Index (RSI) has additionally managed to defend its key 50 degree. Better conviction for patrons could have to come back from a reclaim of its key psychological US$2,000 degree, with any profitable try doubtlessly putting its 2023 excessive again on the radar for a retest.

Supply: IG charts

Friday: DJIA +0.01%; S&P 500 +0.03%; Nasdaq -0.22%, DAX -0.17%, FTSE +0.23%

Article written by IG Strategist Jun Rong Yeap

factor contained in the factor. That is most likely not what you meant to do!

Load your software’s JavaScript bundle contained in the factor as an alternative.

Source link

")