Wall Road posted modest declines in a single day (DJIA -0.38%; S&P 500 -0.20%; Nasdaq -0.18%), following its return from the vacation break. Late final week, the Worry and Greed Index has reverted again to ‘excessive greed’ territory, which can level to near-term overextended worth ranges. That mentioned, seasonality over the previous 20 years stays in favour for a continuation of the upward pattern, with the month of July delivering the second-highest common return and constructive frequency throughout different months.

The Fed minutes got here with not an excessive amount of of a shock, largely serving as a reinforcement for the Fed’s hawkish stance, which have been offered within the collection of Fedspeak beforehand. The extra color is that ‘virtually all’ Fed officers indicated that additional tightening is probably going, however settled at a pause on the earlier assembly to purchase time in assessing the lagged affect of present insurance policies.

Price expectations stay largely unswayed by the Fed minutes, with a continued lean in direction of an extra 25 basis-point charge hike after July to conclude the Fed’s mountaineering course of. However, US Treasury yields discovered their manner increased, with the 10-year yields surging to a brand new three-month excessive. The US greenback acquired an uplift (+0.2%) in a single day as nicely, seemingly headed again to retest the important thing 103.12 degree of resistance as soon as extra. The formation of upper highs and better lows since mid-June displays patrons trying to take again some management, whereas the RSI has defended its key 50 degree to this point. Additional upmove above the 103.12 degree might place a retest of its Might 2023 excessive in sight.

Supply: IG charts

Forward, the US ISM providers PMI will likely be on the radar, which is anticipated to indicate a slight uptick to 51.0 following the shock underperformance in Might. With the Fed having their eyes on the core providers ex-shelter costs, additional indicators of progress within the providers sector’s costs knowledge will present extra conviction for an impending charge pause. The lead-up to the US non-farm payroll report this week can even depart US job openings knowledge in focus at present, together with the preliminary jobless claims and ADP report. Any resilience on that entrance might level to energy within the US labour market which helps soft-landing hopes, however a lot will nonetheless revolve round a continued moderation in wage pressures, which is able to solely be offered within the US non-farm report tomorrow.

Asia Open

Asian shares look set for a detrimental open, with Nikkei -0.94%, ASX -0.63% and KOSPI -0.58% on the time of writing. Regardless of the stellar file of outperformance within the China’s Caixin providers PMI for the reason that begin of the yr (outperform 5 out of 6 events), the most recent knowledge has disenchanted with a lower-than-expected learn (53.9 versus 56.2 forecast). That joined the listing of financial knowledge pointing to a extra lacklustre development image on the planet’s second largest economic system, which suggests extra to be completed within the second half of the yr. The comparatively quiet financial calendar within the area will depart Australia’s commerce steadiness in focus forward.

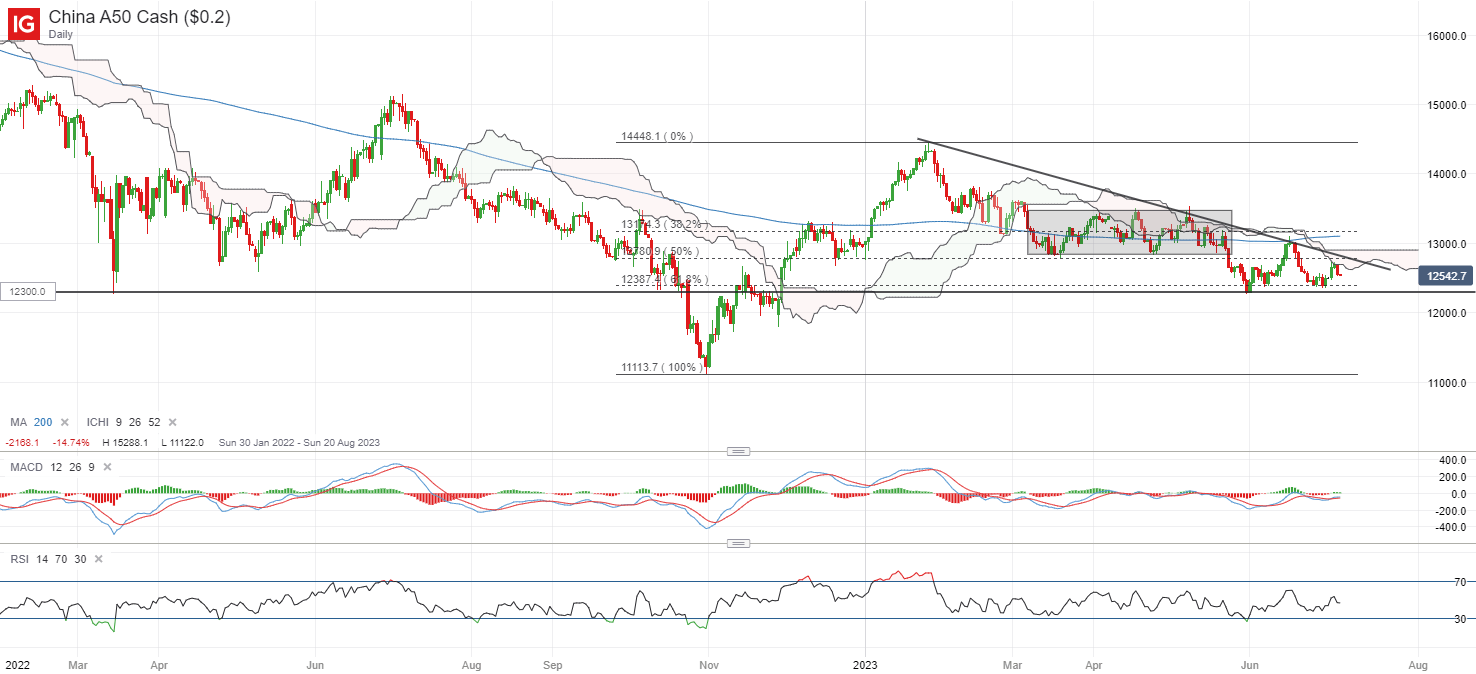

The China A50 index continues to indicate a downward pattern in place to this point, buying and selling on a collection of decrease highs and lows for the reason that begin of the yr. On the upside, a downward trendline and Ichimoku cloud resistance appears to be in the way in which, with the RSI nonetheless hovering beneath the important thing 50 degree. Additional draw back could depart the 12,300 degree on watch as near-term help, with any failure to carry the extent probably paving the way in which in direction of the 11,700 degree subsequent.

Supply: IG charts

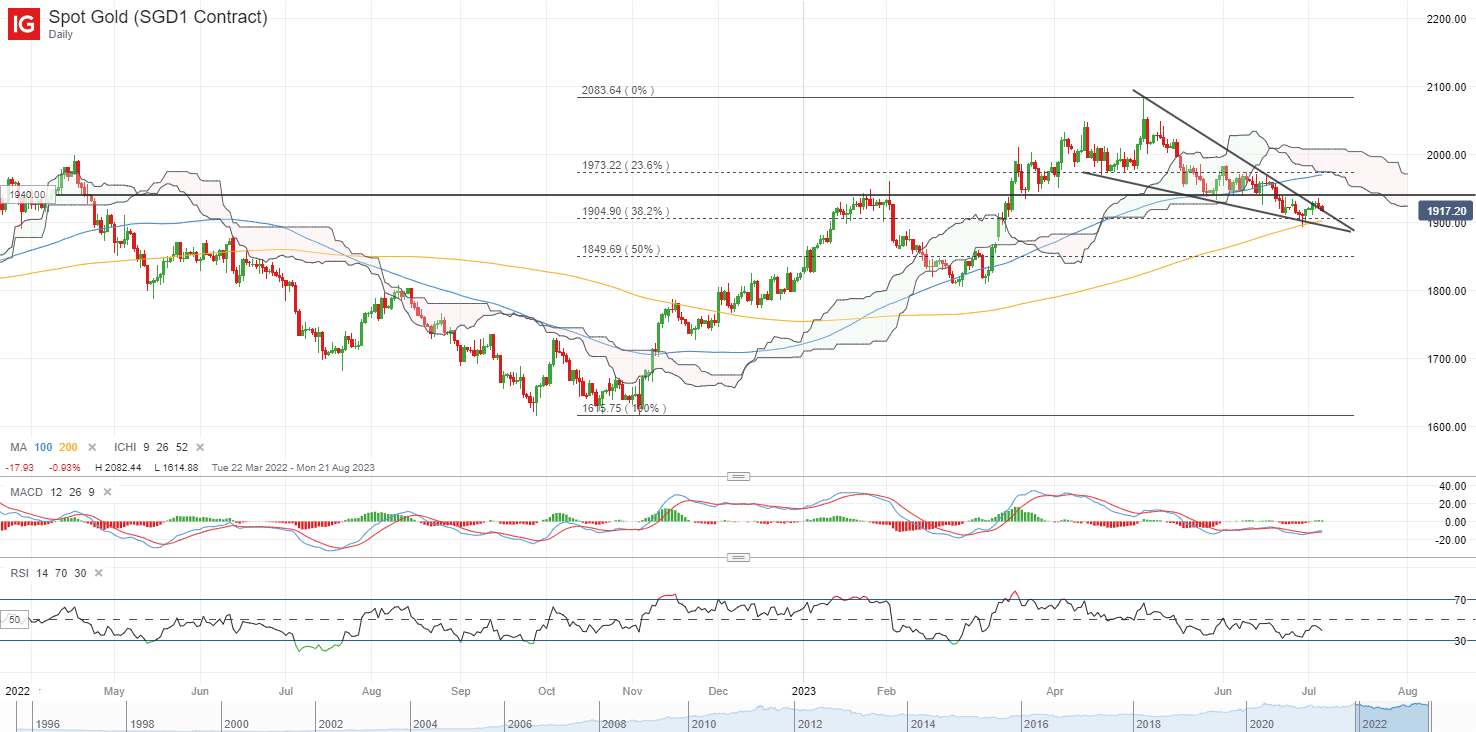

On the watchlist: Gold costs proceed to indicate indicators of exhaustion

An upmove in US Treasury yields and a stronger US greenback has not been well-received by gold costs in a single day, which did not discover a lot conviction for a transfer again above the US$1,940 degree. Up to now, abating recession issues have curtailed safe-haven flows, whereas charge expectations proceed to cost for charge cuts solely in 2024, with the pushback in rate-cuts timeline in comparison with the beginning of the yr driving some unwinding in gold from earlier bullish build-up.

On the technical entrance, its RSI continues to hover beneath the important thing 50 degree as a mirrored image of sellers in management, bolstered by a breakdown of earlier key help confluence on the US$1,940. Additional draw back could depart the US$1,900 degree on watch, the place earlier dip-buying drove the formation of a bullish pin bar final week on the day by day chart. Failure to carry this degree might pave the way in which to retest the US$1,850 degree subsequent.

Supply: IG charts

Wednesday: DJIA -0.38%; S&P 500 -0.20%; Nasdaq -0.18%, DAX -0.63%, FTSE -1.03%

Article written by IG Strategist Jun Rong Yeap

aspect contained in the aspect. That is most likely not what you meant to do!

Load your utility’s JavaScript bundle contained in the aspect as a substitute.

Source link