The second quarter has concluded with an additional pull-ahead in danger sentiments final Friday, with the S&P 500 closing at its highest stage in 14 months whereas the Nasdaq has turned in its second consecutive quarter of positive factors. Bettering market breadth recently means that market positive factors have been broadening out, as a pushback in financial knowledge towards recession fears introduced traction in the direction of different economically delicate sectors for some catch-up efficiency. The equal-weighted S&P 500 index is at its highest since February this 12 months.

Small-cap shares have been seeing some indicators of life as effectively, with the Russell 2000 index again to retest its current June 2023 excessive on the 1,900 stage. Up to now, its Relative Power Index (RSI) has retained above the 50 stage, together with the formation of a brand new greater low final week, which saved the general upward bias intact. The 1,900 stage will function speedy resistance to beat. Reclaiming this stage might anchor in a brand new greater excessive and probably pave the best way for the index to retest the important thing psychological 2,000 stage subsequent, the place its year-to-date excessive resides.

Supply: IG charts

On the financial knowledge entrance, market contributors appear to take consolation in a lower-than-expected learn from the US core PCE value index (4.6% versus 4.7% consensus), however extra notably, the core providers ex-housing element has are available at a brand new 10-month low on a month-on-month foundation. Being highlighted beforehand by the Federal Reserve (Fed) as a gauge for inflation persistence, promising progress on that entrance has allowed the Fed extra room to contemplate a fee pause after the July assembly. Fed funds futures proceed to cost for one final 25 basis-point fee hike from the Fed to conclude the mountaineering cycle.

The US greenback didn’t take the US inflation knowledge effectively final Friday, delivering 0.45% decrease regardless of some resilience in US Treasury yields. That allowed gold costs to see some reduction (+0.53%) from current sell-off, whereas silver costs try to defend its 200-day transferring common (MA) with some dip-buying in the direction of the tip of final week. Forward, the US Independence Day vacation tomorrow could put a lighter buying and selling session to begin the week, with some give attention to the US ISM manufacturing PMI knowledge launch tonight.

Asia Open

Asian shares look set for a constructive open, with Nikkei +1.35%, ASX -0.01% and KOSPI +1.13% on the time of writing. Following a retracement from earlier overbought technical situations, the Nikkei has fashioned a brand new greater low on the each day chart, with long-legged candles pointing to some dip-buying at across the 32,300 stage. The index is simply 1% away from June 2023 excessive, which can depart any formation of a brand new greater excessive on watch over the approaching days to reiterate its total upward development.

Throughout the area, a sequence of PMI knowledge was met with some hits and misses, notably with Japan’s manufacturing unit actions falling again into contractionary territory in June (49.8 versus earlier 50.6) whereas South Korea’s PMI additionally marked a deeper contraction (47.8 versus earlier 48.4) as a mirrored image of the worldwide financial slowdown. The day forward will depart China’s Caixin PMI studying in focus. Following the subdued learn within the official manufacturing PMI final week, the Caixin PMI is anticipated to bolster the lacklustre financial situations in China, which can help extra to be performed by authorities.

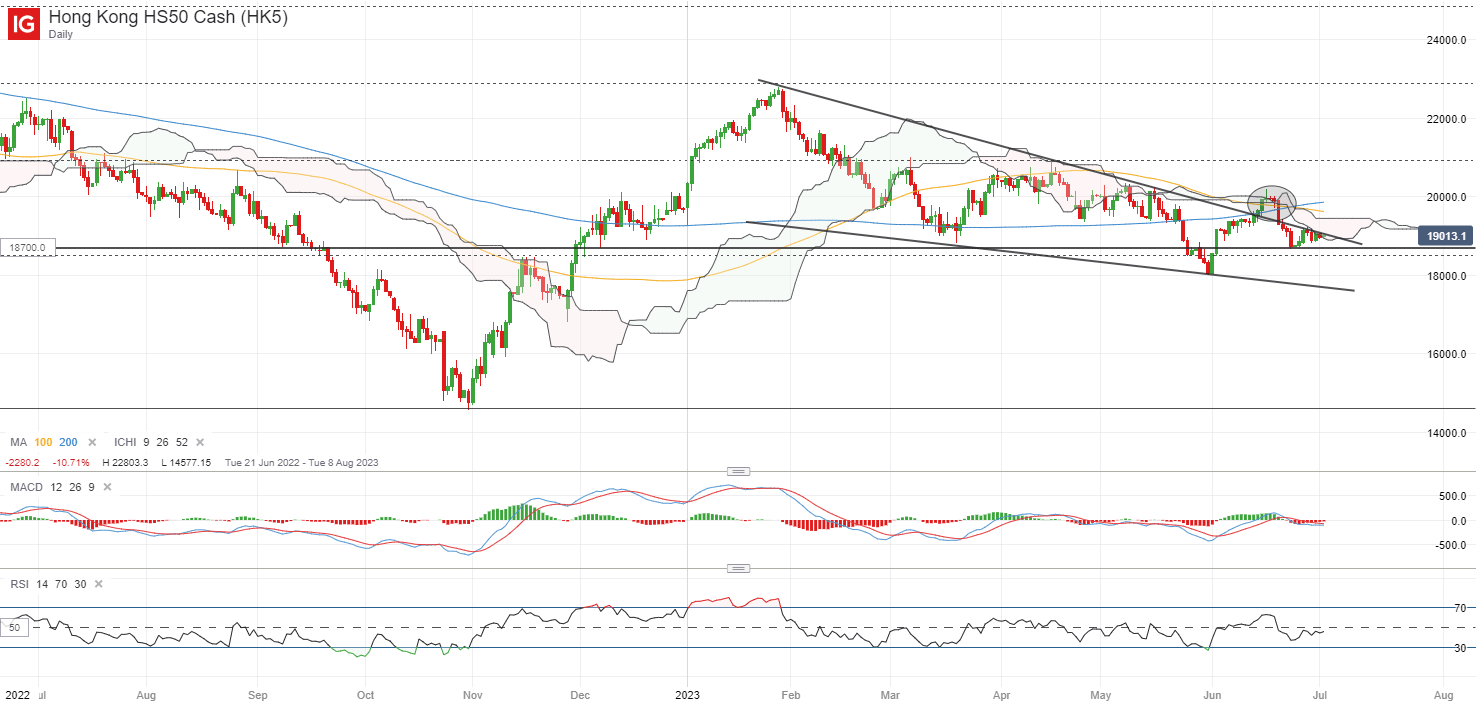

Up to now, the Hold Seng Index stays exhausted, with its RSI again beneath the 50 stage whereas a descending wedge sample stays in place after a short-lived try for a breakout. On the upside, evidently a sequence of resistance should be overcome to replicate higher management from consumers, notably the psychological 20,000 stage, the place the higher fringe of the Ichimoku cloud resides on the weekly chart.

Supply: IG charts

On the watchlist: AUD/USD on watch forward of RBA’s rate of interest determination this week

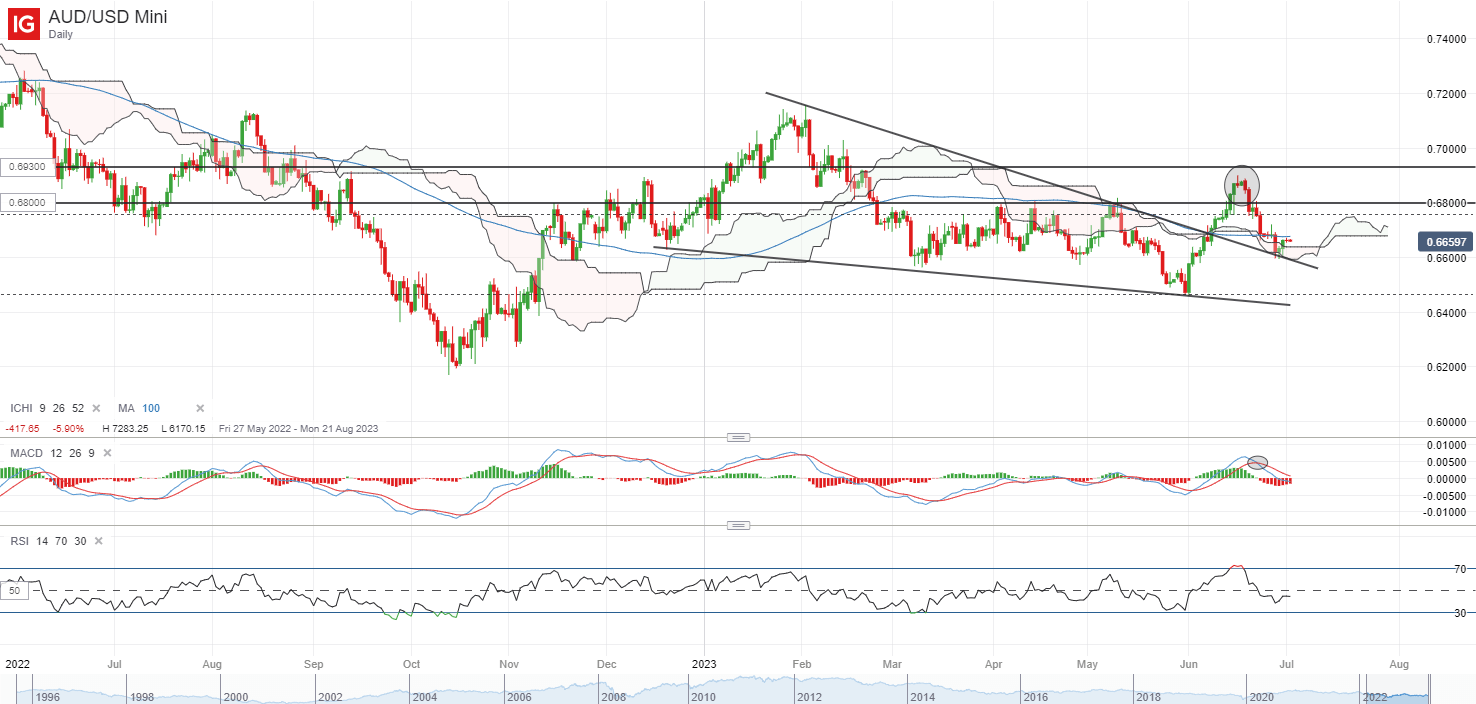

The AUD/USD has managed to the touch its three-month excessive in mid-June, solely to have a dovish shock within the Reserve Financial institution of Australia (RBA) assembly minutes set off a pointy retracement again beneath the 0.680 stage. The robust pushback towards earlier hawkish expectations has pressured a transfer again beneath its key 100-day MA for the pair, with the RSI hovering beneath the 50 stage.

Because the RBA assembly looms tomorrow, a considerably lower-than-expected Australia’s inflation knowledge final week has left expectations leaning in the direction of a fee pause however it might doubtless be an in depth name, with market nonetheless pricing for any pause to be a short lived transfer as in comparison with the tip of tightening. The AUD/USD is at the moment again to retest a downward trendline help on the each day chart on the 0.660 stage however a lot awaits. A sequence of resistance could should be overcome to offer conviction of bulls taking again management, which incorporates its 100-day MA and the 0.680 stage of resistance.

Supply: IG charts

Friday: DJIA +0.84%; S&P 500 +1.23%; Nasdaq +1.45%, DAX +1.26%, FTSE +0.80%

Article written by IG Strategist Jun Rong Yeap

component contained in the component. That is in all probability not what you meant to do!

Load your software’s JavaScript bundle contained in the component as an alternative.

Source link