Market Recap

The conclusion of the June assembly has seen the Federal Reserve (Fed) conserving charges on maintain at 5.00%-5.25% in a widely-anticipated transfer, however there may be much less conviction for markets that right this moment’s transfer will mark the top of its tightening marketing campaign.

A hawkish takeaway got here from the Federal Open Market Committee (FOMC) dot plot, with peak price for 2023 revised to five.6% from earlier 5.1%, which suggests one other 50 basis-point (bp) of tightening by the top of this yr. Price forecasts for 2024 and 2025 had been revised upwards as effectively, which appears to place a high-for-longer price outlook on the horizon. The justification could come on the again of some persistence in inflationary pressures, with the Fed’s core PCE forecasts seen larger at 3.9% for 2023 in comparison with the three.6% anticipated in March.

Feedback from Fed Chair Jerome Powell appear so as to add to the hawkish equation, saying that Fed price cuts are a ‘couple years out’, at a time when broad market expectations had been pricing for price cuts by the top of the yr. With July assembly being deemed as a ‘stay’ assembly from the Fed Chair, it’s going to depart any price choice to only a handful of inflation and labour knowledge forward. Present Fed funds futures proceed to lean in direction of a 25 bp transfer in July, however its pricing for terminal price at 5.25%-5.5% are nonetheless much less hawkish than what the Fed has guided, which leaves any additional recalibration on watch.

Treasury yields had been on a combined tone, reflecting some indecision within the aftermath of the FOMC assembly. However, a high-for-longer price outlook has not been well-received by gold costs, which noticed a pointy paring in preliminary features in a single day. Intermittent bounces over the previous one month have failed to seek out a lot of a follow-through, with costs hovering again close to its two-month low across the US$1,940 degree. Any breakdown to a brand new decrease low could also be in sight, which may reinforce its near-term downward bias. Its Relative Energy Index (RSI) continues to pattern under the important thing 50 degree, whereas a key trendline assist in place since November 2022 has been invalidated, reflecting sellers in management for the current.

Supply: IG charts

Asia Open

Asian shares look set for a slight constructive open, with Nikkei +0.17%, ASX +0.31% and KOSPI +0.30% on the time of writing as market individuals proceed to digest the most recent FOMC assembly. The financial calendar this morning has seen first-quarter gross home product (GDP) learn from New Zealand dragging the nation right into a technical recession. A 0.1% decline quarter-on-quarter in 1Q, following a 0.7% decline in 4Q, is probably going to supply additional justification that the Reserve Financial institution of New Zealand (RBNZ) is completed with tightening, which interprets to some downward strain on the NZD.

The day forward will convey focus to Australia’s employment knowledge, adopted by a sequence of financial knowledge out of China (industrial manufacturing, retail gross sales, mounted asset funding). Current cuts to China’s short-term borrowing prices could drive hopes of an identical adjustment to the one-year MLF price later right this moment, with the upcoming financial knowledge possible so as to add to the latest sequence of draw back surprises and reinforce a low-for-longer development outlook in China. All three above-mentioned knowledge are anticipated to show some moderation in year-on-year development from April.

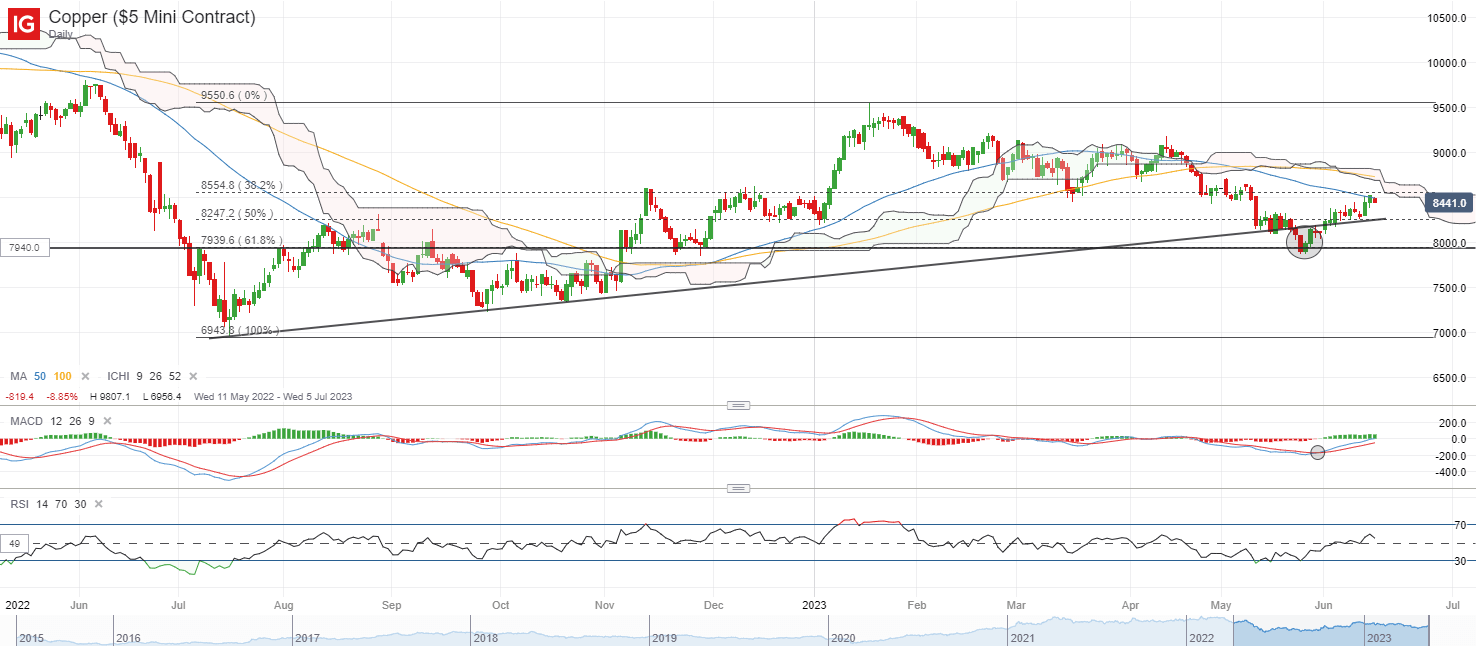

Copper costs have managed to get well greater than 8% since discovering assist on the US$7,940/tonne degree. A reclaim of the RSI above the 50 degree, together with a bullish crossover on transferring common convergence/divergence (MACD) could level in direction of some upward momentum within the close to time period. That mentioned, rapid resistance nonetheless stands on the US$8,600/tonne degree for now. Higher conviction for a extra sustained upside could have to come back from a transfer above the Ichimoku cloud to sign an upward pattern in place. On any draw back, the US$8,250/tonne degree could convey some assist from an upward trendline in confluence with a Fibonacci retracement degree.

Supply: IG charts

On the watchlist: Knee-jerk response within the US greenback however extra indicators wanted

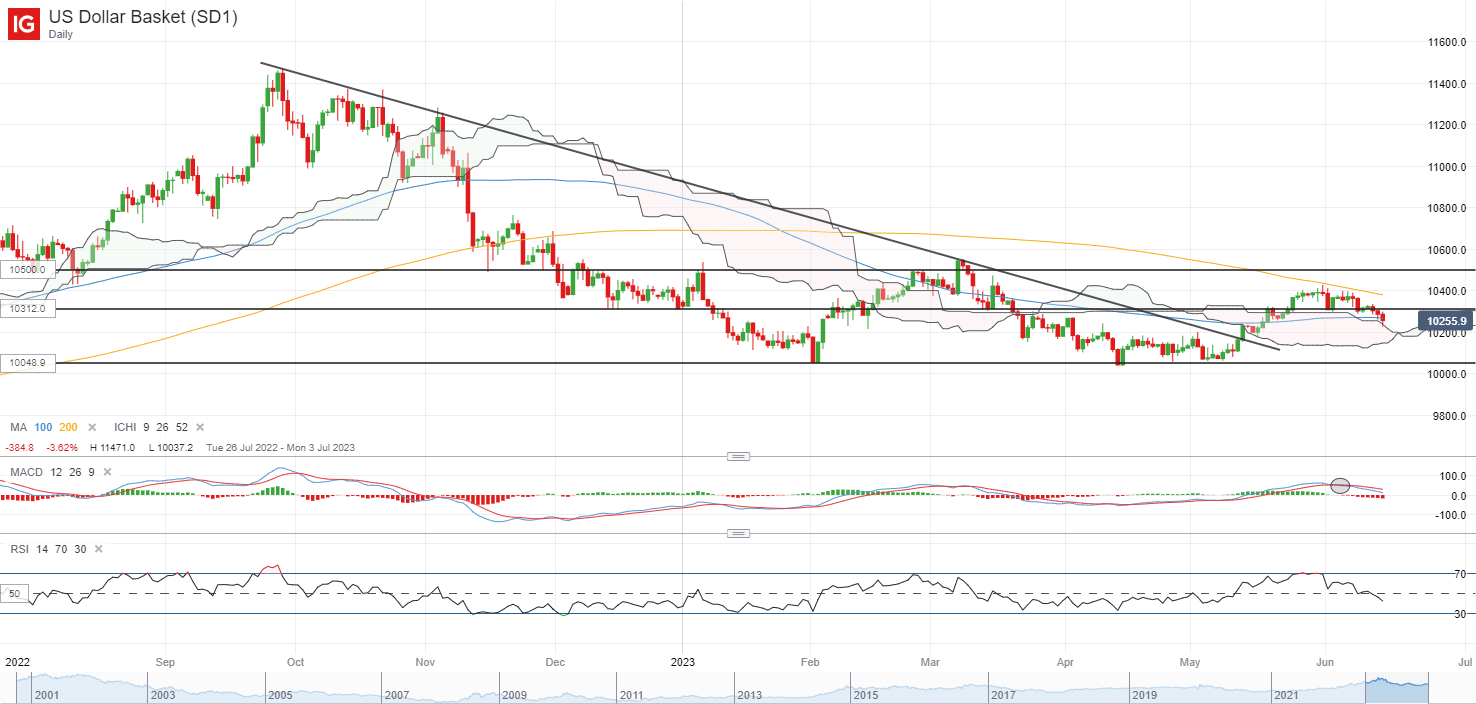

The FOMC assembly has caused some volatility within the US greenback in a single day, with the discharge of the dot plot triggering a 0.5% knee-jerk response mid-day earlier than some features had been pared in the course of the Fed press convention. Higher conviction for the bulls could have to come back from an overturn of the lower-highs-lower-lows formation on the four-hour chart because the begin of the month, with rapid resistance to beat on the 103.12 degree.

For now, its RSI has headed under the important thing 50 degree, together with a declining MACD, which requires the necessity of a major build-up in upward momentum to supply some conviction for the bulls as effectively. Any failure to faucet on the hawkish tone from the FOMC assembly for any transfer larger over subsequent days may level in direction of ongoing exhaustion, which may place its Might backside in sight for a retest subsequent.

Supply: IG charts

Wednesday: DJIA -0.68%; S&P 500 +0.08%; Nasdaq +0.39%, DAX +0.49%, FTSE +0.10%

component contained in the component. That is most likely not what you meant to do!

Load your utility’s JavaScript bundle contained in the component as an alternative.

Source link