mikkelwilliam

Creator’s Notice: This text was revealed to iREIT on Alpha in Mid-Might of 2023.

Expensive subscribers,

Safehold (NYSE:SAFE) is an attention-grabbing REIT. We very not too long ago had an replace article by Brad Thomas in regards to the firm, which you’ll find right here. He showcased his numerous returns over completely different durations of time – constructive from 2018, unfavorable since 2021, and considerably constructive, although underperforming, since April of 2023.

My very own final piece on SAFE was revealed again in October of final yr. I’ve a modest place within the enterprise, and I am going to clarify to you right here why I am shopping for extra – some related causes to Brad, but additionally another issues.

Let’s get going.

SAFE stays fantastically protected – here is why and why I am at a “BUY”

SAFE is not the best REIT to know and requires some in-depth studying earlier than what to anticipate and what the corporate does.

It is a “Land lease REIT”. Not lots of them on the market, however that is what Safehold does and the enterprise it is in. SAFE is New York-based, it is externally managed (extra on that later), and comes with an attention-grabbing enterprise thought. It is the one public floor lease firm obtainable at the moment, and it focuses strictly on investment-grade floor lease corporations, with the intention to enhance its security and handle solely an institutional quality-level portfolio.

So what precisely is a Land-lease REIT?

The corporate acquires, manages, and capitalizes on floor leases. On this enterprise thought, the tenants personal their buildings, however not the land that the constructing is constructed upon. The lease entails undeveloped industrial land that in flip is leased to tenants, given the suitable to develop the property at some point of the lease.

instance of an organization that makes use of floor leases is Macy’s (M). The corporate’s buildings are owned by Macy’s, together with issues like parking, however the tenant nonetheless pays hire on the land.

Structurally and organizationally, a floor lease is similar to every other form of lease. The tenant makes month-to-month hire funds. With a floor lease REIT like Safehold, the leases are web leases, which implies that tenants assume accountability for taxes, insurance coverage, and CapEx/OpEx at some point of the lease.

It does not take a lot explaining past this as to why that is a gorgeous enterprise mannequin. The corporate, not like many different REITs in places of work, residences, or different segments, additionally does not maintain any large overexposure to anybody space.

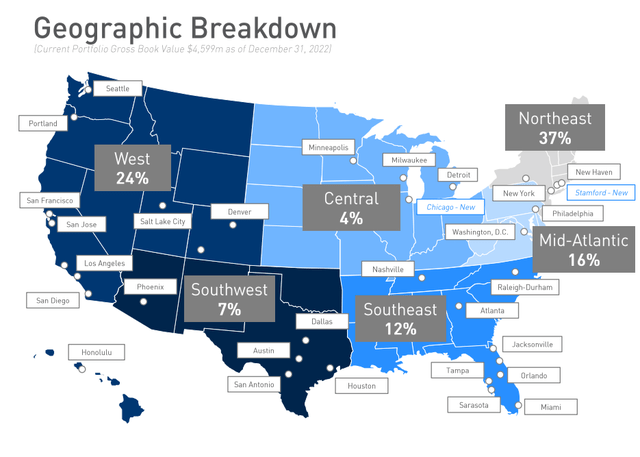

SAFE IR (SAFE IR)

The enhancements that might be made contain extra publicity to sunbelt and central – however aside from that, that is a gorgeous mannequin.

The enchantment of the mannequin for the tenant is that it does not require the corporate leasing the land to place up large quantities of capital for the land itself. As a result of these leases include very lengthy leasing phrases – not unusual to see over 50 years right here – it allows corporations to basically optimize their capital combine by not having to make use of important quantities of its personal capital or debt to develop – whereas the homeowners of the lands, the REIT, get important and long-term security from recurring hire checks. They get a long time’ price of earnings safety and might ultimately, often approach off sooner or later, gather a lump sum fee for the property.

The tenant can even get entry to land that they in any other case would haven’t any entry to. For this reason the mannequin is utilized by retail tenants akin to Macy’s, but additionally McDonald’s (MCD) and Starbucks (SBUX).

I am going extra into the varied lease varieties and why landlords need unsubordinated versus subordinated leases from their tenants. However that’s how floor leases work, and why they’re enticing. And Safehold has been rising massively.

Over the previous few quarters, Safehold has been managing fairly properly. The quarterly outcomes ought to be taken with a fair proportion of salt, as a result of present prices of the incoming merger with iStar, inc.

There appear to be two methods to view this play. One aspect, the extra bearish aspect, views SAFE as uncovered to what are basically Workplace-type properties in an actual property bubble/setting that isn’t conducive to places of work, as we have seen from the valuations for Workplace REITs. They are saying regardless of the corporate declining considerably in worth, this firm just isn’t going anyplace close to an upside, and the corporate’s elevated publicity to floating-rate debt together with its merger makes all the play an unappetizing potential.

On the opposite aspect, extra a constructive observe, say (and level out) that SAFE lacks the fairness danger of managing actual property – it is a capital supplier with none precise property obligations, making the comparability to an Workplace-type firm or REIT utterly moot. Whereas the leases it holds might be stated to be beforehand particular to places of work, it does not dictate that places of work need to be constructed there.

Moreover, any debt danger must be put within the context of its maturities – and these are a few of the longest within the trade, at a debt-to-book fairness of beneath 2x and a complete debt to Fairness market cap of beneath 2.5x. The typical maturities listed here are over 22 years, and no maturities coming due till 2026.

So, as is considerably typical with me, I say that the pessimist is just too pessimistic, and the unbridled optimism is just too optimistic. The reality is, as I see it, someplace in between.

Over the previous few quarters, SAFE earnings have been beneath the forecasted charge. 1Q got here in at ~80% decrease YoY, however in fact, this was principally because of merger prices, which we are able to web out. Other than these, the earnings decline was principally a product of accelerating publicity to floating charges and debt load.

Anybody investing in SAFE wants to pay attention to what occurs when financing prices change because of rate of interest adjustments, no matter lengthy maturities, both because of float publicity or because of refis. That is sure to offer some downward strain in earnings, each GAAP and FFO, that would see the corporate go even decrease right here.

Whereas I will not declare that I foresaw the precise nature of this again 1-2 years in the past after I obtained my eyes opened to SAFE, I did see the danger in rates of interest, and this precipitated me to remain out of the inventory till it fell beneath $26/share. The bubble we noticed in 2020-2022, which ended when SAFE fell from grace and from a share worth of over $60/share was by no means one thing I noticed as sustainable.

Nevertheless, claiming in the identical vein that the corporate’s present debt combine/composition is untenable and can trigger a downfall goes too far. The argument is being made as a result of near-billion in debt that SAFE has placed on an unsecured revolver – not usually the power you’d need to use for that quantity as a result of rate of interest price of such an answer. These latest strikes have left the corporate a bit cash-strapped and with rates of interest going up. We’re seeing notes at over 5%, and one more $100M revolver at LIBOR + 1.5%, which is important on this setting. LIBOR was properly beneath 3% a yr in the past, and the corporate’s curiosity funds are actually over 6% on common for that barely north of $1B.

If a criticism might be levied on the analysts following SAFE and their forecasts from march-April 2022, is that they anticipated rates of interest to remain the identical, and utterly didn’t forecast this large delta in debt-related funds.

The present rate of interest setting additionally implies that something the corporate tries to do on the debt combine/finance aspect goes to be influenced by present market circumstances. There aren’t any “good” or “straightforward” hedges to get out of this case, akin to floating to fastened swaps or some refinancings. The dangers financiers take will come at a value, and that leaves me with the next expectation for earnings for the subsequent few years – that they will not be massively rising.

On the identical time, the bearish aspect takes far too unfavorable a view and sometimes forgets what the corporate has really achieved – and the way it operates – such because the essential variations in its principal security.

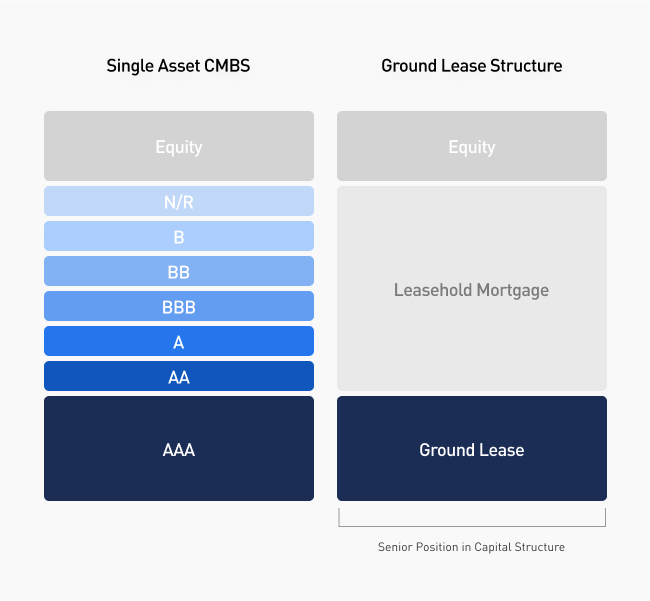

Safehold IR (Safehold IR)

The corporate’s working mannequin entails an AAA-like place within the capital construction, just about immune from the sorts of dangers you see in single-asset CMBS. Even with contractual inflation captures, the corporate’s inflation-adjusted yield is over 6% at 3% long-term inflation.

Bears additionally neglect, or underestimate (in our opinion) the worth of the CARET construction and the worth it affords – each when it comes to monetization and different considerations. For these unfamiliar with it, the CARET program is an innovation when it comes to making an attempt to worth future cap appreciation, with CARET unit reflecting unrealized capital appreciation the corporate expects to obtain as soon as leases terminate or expire.

Who would need to purchase these, you might ask?

Clearly, loads of educated traders, provided that 3% have been offered to institutional traders, akin to sovereign wealth funds and household places of work that are recognized to put money into long-term stable development and security potential. These holders are entitled to take part in any proceeds above the fee foundation as soon as property are offered.

The maybe greatest “downside” I see when it comes to danger is the focus of its land portfolio to Manhattan, which nonetheless makes up round 24% of the corporate’s gross e book worth or GBV. SAFE has been diversifying right here, but it surely nonetheless has a variety of work to do with the intention to discover worth in areas that I’d take into account to be “enticing” relative to considerably riskier west and east-coast areas.

Bears additionally characterize the corporate as an workplace landholder – that is false. 44% is Workplace, however multifamily is over 35%. This makes the corporate a diversified holder with a tilt towards Workplace.

The corporate’s robust fundamentals, together with its BBB+, give a totally completely different image than a few of the bears telling us to not put money into the corporate wish to convey. They’re additionally rated in a different way than a REIT, which can be not coated in a few of the bearish reviews.

Let us take a look at valuation.

Safehold – The valuation may be very tough

Every time somebody says “Effectively, this firm cannot be measured historically”, I are likely to take about nineteen steps again.

Usually, I actually do not belief any enterprise that claims that with the intention to worth it “correctly”, it’s important to do X and Y.

Why? As a result of there are 100 enticing funding alternatives that don’t require us to take distinctive approaches to one thing so simple as a valuation for a enterprise.

So, perceive that after I say this firm is enticing and might be purchased, it comes with a sure danger profile that may be thought of in a different way than your conventional corporations – and by completely different, I imply increased in some methods.

In terms of SAFE, there may be some sound reasoning behind why it would want some variations when it comes to its metrics – and a few of the ones are talked about above. The corporate’s debt is sky-high – over 12.5x web debt/EBITDA. However on the identical time, SAFE has no obligations to its properties within the type of CapEx. The belief is that when that extraordinarily long-maturity debt comes due in over 25-30 years, the compounding nature of its money flows can have achieved wonders. It is not a mistaken assumption to have both.

To be able to see the protection, you want solely take a look at what the corporate has achieved already to enhance its metric. Again 5 years in the past, the payout was 90%+ of web. That’s now lower than 35% of web at a yield of virtually 5%.

Put up the merger, and given its difficult peer state of affairs (no different direct friends exist), evaluating this firm is probably the toughest a part of this text and of wanting on the firm.

We are able to take a look at some analyst estimates. In terms of S&P World, estimates right here put the corporate at round $24-$25/share on common, however given the low protection, I are likely to ascribe this to a lack of information of the corporate’s earnings potential and upside.

That isn’t to say that I count on SAFE to return to $60/share or anyplace near it, no less than not within the close to time period. With the latest internalization of its administration and the method is at the moment in, coupled with the near-zero years of precise publicly-traded historical past, I are likely to say that SAFE is difficult to conservatively forecast expectations from – however a 13-16x P/FFO charge, coming to a 2025E of round $29-$33/share appears the baseline minimal of what I’d count on from the corporate right here.

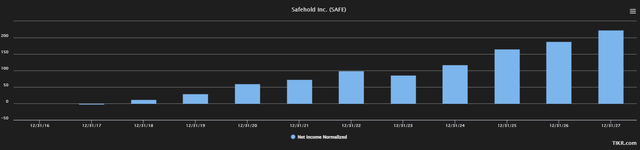

Once I final wrote in regards to the firm, we have been at lower than $26/share, which I considered as fairly enticing with a possible long-term upside within the triple digits. I nonetheless view this as being totally attainable. And I’m removed from alone on this. Right here is the anticipated web earnings development past the 2023E dip.

TIKR.com SAFE forecast (TIKR.com)

And you’ll see the identical traits in different measures – be it income, EBITDA, EBIT, EBT – vendor’s selection, it is forecasted to rise. The curiosity expense I discussed, that is anticipated to remain at or in regards to the degree it at the moment is, anticipating administration to type it out at or barely above the degrees we’re at the moment at, with rising bills as the corporate grows. (Supply: S&P World)

If this seems to be the case, then I consider this to be a catalyst for additional upside. Many analysts have very constructive targets for the enterprise – upwards of $50/share. If sure optimistic views materialize, that is totally attainable. However I are likely to view this with a wholesome dose of skepticism and would common it out to a PT of round $32/share, which might nonetheless be a double-digit upside from present ranges.

One other argument, and one well-covered in Brad’s latest article, is insider data and CEO data.

Coupling all of this, I see a little bit of danger and maybe not as unerringly a powerful purchase as for another qualitative REITs on the market – however I positively see an upside to the corporate.

My place in SAFE is not large – but it surely’s within the inexperienced, and I am open to increasing it right here.

I am at a “BUY”, and I give it a present PT of $32/share.

Questions? Let me know!