Up to date on April twenty sixth, 2023 by Bob Ciura

Buyers trying to generate increased earnings ranges from their funding portfolios ought to have a look at Actual Property Funding Trusts or REITs. These are firms that personal actual property properties and lease them to tenants or spend money on actual property backed loans, each of which generate a gradual stream of earnings.

The majority of their earnings is then handed on to shareholders by way of dividends. You possibly can see all 200+ REITs right here.

You possibly can obtain our full record of REITs, together with necessary metrics akin to dividend yields and market capitalizations, by clicking on the hyperlink beneath:

The fantastic thing about REITs for earnings traders is that they’re required to distribute 90% of their taxable earnings to shareholders yearly within the type of dividends. In return, REITs sometimes don’t pay company taxes.

Consequently, most of the 200+ REITs we monitor supply excessive dividend yields.

However not all high-yielding shares are automated buys. Buyers ought to fastidiously assess the basics to make sure that excessive yields are sustainable. Many (however not all) high-yield securities have a major threat of a dividend discount and/or deteriorating enterprise outcomes.

With that in thoughts, we created a listing of protected REITs which have premier enterprise fashions and robust property portfolios. In flip, their dividends must be thought of extra sustainable than the overwhelming majority of REITs.

Particularly, the next 9 protected REITs have no less than 10 years of annual dividend will increase, Dividend Danger Scores of ‘C’ or higher, dividend yields above 3% utilizing information from the Positive Evaluation Analysis Database.

The shares are ranked by dividend yield, from lowest to highest. The desk of contents beneath permits for straightforward navigation.

Desk of Contents

You possibly can immediately bounce to any particular part of the article by utilizing the hyperlinks beneath:

Protected REIT No. 9: American Tower Corp. (AMT)

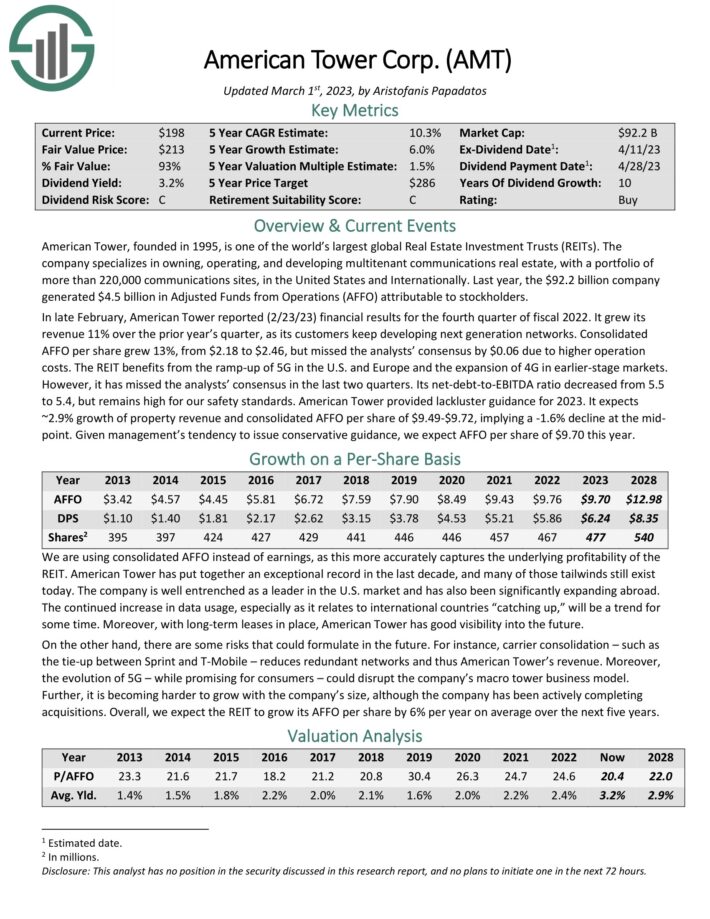

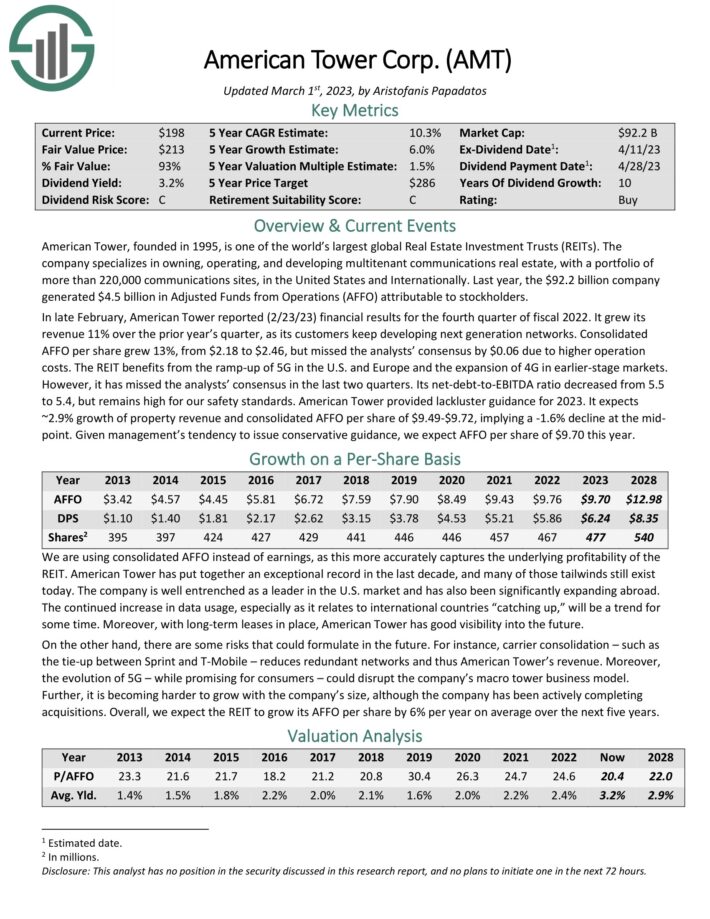

American Tower focuses on proudly owning, working, and creating multi-tenant communications actual property, with a portfolio of greater than 220,000 communications websites, in america and Internationally. Final yr, the $92.2 billion firm generated $4.5 billion in Adjusted Funds from Operations (AFFO) attributable to stockholders.

Supply: Investor Presentation

In late February, American Tower reported (2/23/23) monetary outcomes for the fourth quarter of fiscal 2022. It grew its income 11% over the prior yr’s quarter, as its prospects hold creating subsequent technology networks. Consolidated AFFO per share grew 13%, from $2.18 to $2.46, however missed the analysts’ consensus by $0.06 resulting from increased operation prices.

The REIT advantages from the ramp-up of 5G within the U.S. and Europe and the growth of 4G in earlier-stage markets. Its net-debt-to-EBITDA ratio decreased from 5.5 to five.4.

American Tower supplied steering for 2023. It expects ~2.9% development of property income and consolidated AFFO per share of $9.49-$9.72, implying a -1.6% decline on the midpoint.

Click on right here to obtain our most up-to-date Positive Evaluation report on American Tower (preview of web page 1 of three proven beneath):

Excessive-Yield REIT No. 8: CubeSmart (CUBE)

CubeSmart is a self-managed REIT centered totally on the possession, operation, administration, acquisition, and improvement of self-storage properties in america. The corporate owns 611 self-storage properties, totaling roughly 44.1 million rentable sq. ft within the District of Columbia and 24 different states.

As well as, the corporate manages 663 shops for third events bringing the whole variety of shops that it owns and/or manages to 1,279. CubeSmart has over 340,000 prospects and generated round $1 billion in revenues final yr.

Supply: Investor Presentation

On December seventh, 2022, CubeSmart raised its dividend by 14% to a quarterly charge of $0.49. On February twenty third, 2023, CubeSmart reported its This fall-2022 and full-year outcomes for the interval ending December thirty first, 2022. For the quarter, revenues grew by 9.5% to $200.7 million year-over-year.

Increased revenues have been primarily attributable to elevated rental charges on our same-store portfolio in addition to revenues generated from property acquisitions and not too long ago opened improvement properties.

Particularly, same-store NOI rose 12.1% year-over-year, pushed by 9.5% same-store income development in opposition to only a 2.3% same-store improve in property working bills. Accordingly, FFO grew by a considerable 72.2% to $152.6 million. Nonetheless, resulting from an elevated variety of shares excellent as a useful resource of funds for the corporate’s acquisitions, FFO/share grew by 68% to $0.67. Identical-store occupancy on the finish of This fall was 92.1%, barely decrease from final yr’s 93.3%.

For the yr, FFO/share jumped by 19.9% to $2.53. Administration launched its fiscal 2023 steering, anticipating to attain FFO/share between $2.64 and $2.71. We’ve utilized the midpoint of this vary in our estimates, which suggests year-over-year development of about 6%.

Click on right here to obtain our most up-to-date Positive Evaluation report on CubeSmart (preview of web page 1 of three proven beneath):

Excessive-Yield REIT No. 7: Essex Property Belief (ESS)

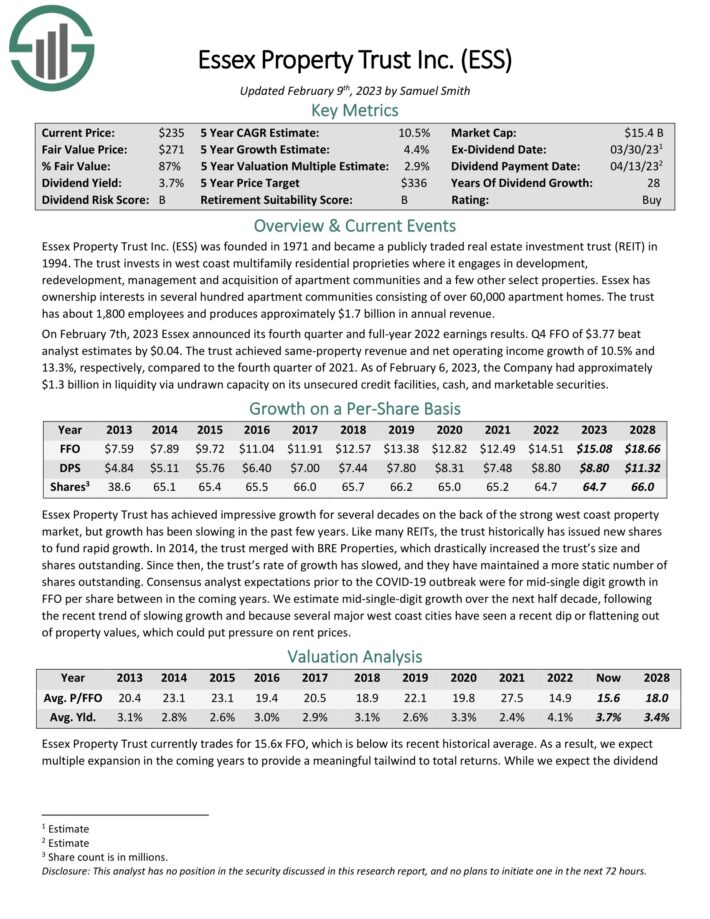

Essex Property Belief was based in 1971. The belief invests in west coast multifamily residential proprieties the place it engages in improvement, redevelopment, administration and acquisition of condominium communities and some different choose properties.

Essex has possession pursuits in a number of hundred condominium communities consisting of over 60,000 condominium houses. The belief has about 1,800 staff and produces roughly $1.6 billion in annual income.

Supply: Investor Presentation

On February seventh, 2023 Essex introduced its fourth quarter and full-year 2022 earnings outcomes. This fall FFO of $3.77 beat analyst estimates by $0.04. The belief achieved same-property income and web working earnings development of 10.5% and 13.3%, respectively, in comparison with the fourth quarter of 2021.

As of February 6, 2023, the corporate had roughly $1.3 billion in liquidity through undrawn capability on its unsecured credit score amenities, money, and marketable securities.

Click on right here to obtain our most up-to-date Positive Evaluation report on ESS (preview of web page 1 of three proven beneath):

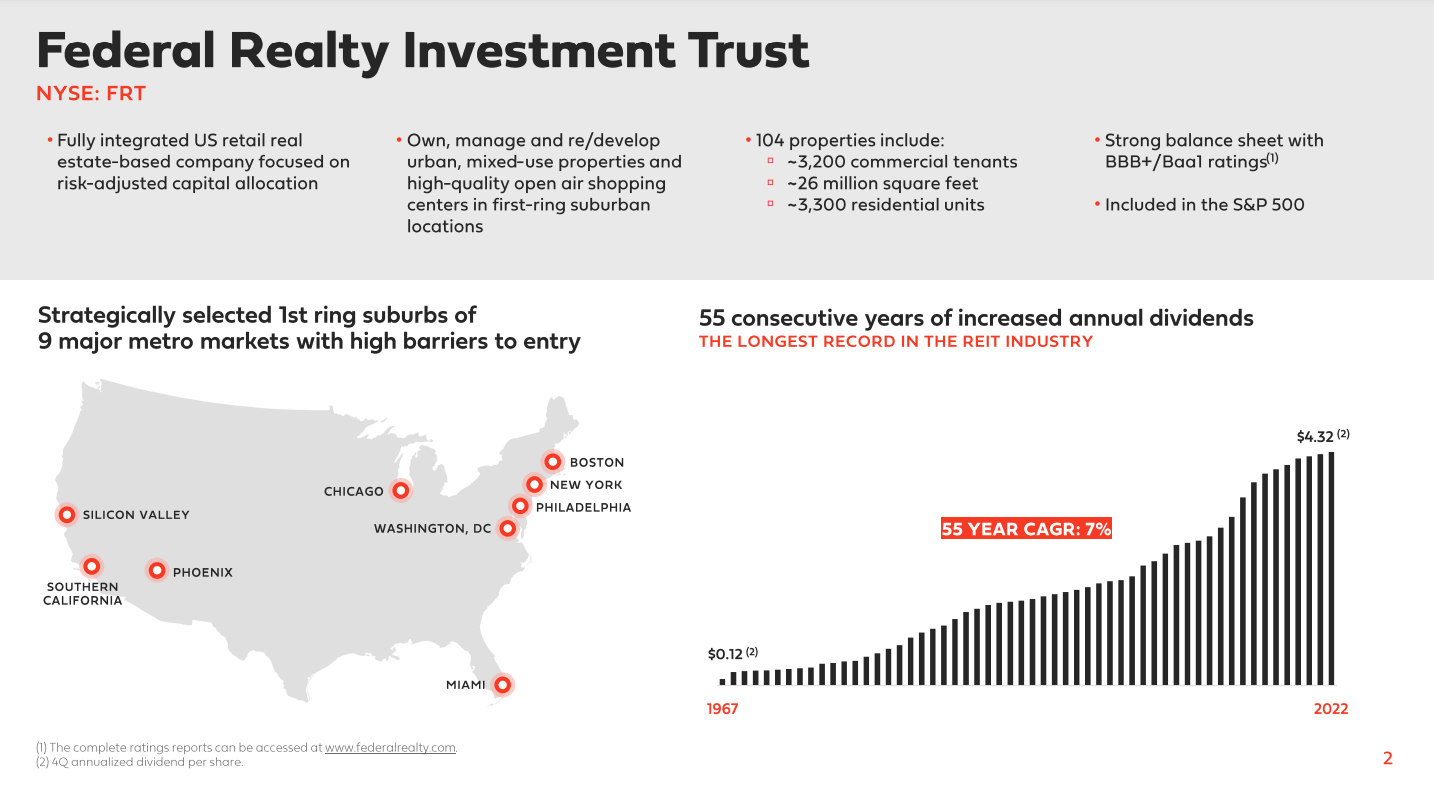

Excessive-Yield REIT No. 6: Federal Realty Funding Belief (FRT)

Federal Realty primarily owns procuring facilities. Nonetheless, it additionally operates in redevelopment of multi-purpose properties together with retail, flats, and condominiums. The portfolio is extremely diversified when it comes to tenant base.

Supply: Investor Presentation

On February eighth, 2023 FRT reported working outcomes for its yr and quarter ended December 31, 2022. For the yr ended December 31, 2022 and 2021, web earnings accessible for widespread shareholders was $4.71 per diluted share and $3.26 per diluted share, respectively. For the three months ended December 31, 2022 and 2021, web earnings accessible for widespread shareholders was $1.40 per diluted share and $1.44 per diluted share, respectively.

For the yr ended December 31, 2022 and 2021, Federal Realty reported working earnings of $526.4 million and $394.7 million, respectively. For the three months ended December 31, 2022 and 2021, working earnings was $155.1 million and $147.5 million.

FRT has elevated its dividend for over 50 years, making it a Dividend King. It’s the solely Dividend King on the record of protected REITs.

Click on right here to obtain our most up-to-date Positive Evaluation report on Federal Realty (preview of web page 1 of three proven beneath):

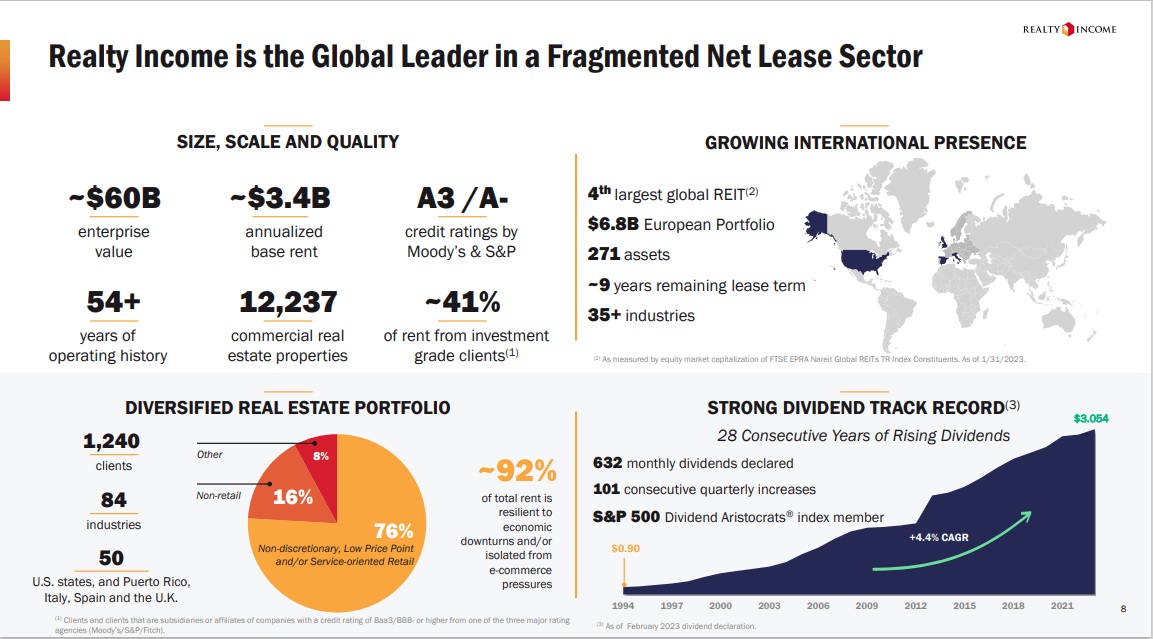

Excessive-Yield REIT No. 5: Realty Earnings (O)

Realty Earnings owns greater than 11,000 properties and has a market capitalization in extra of $40 billion. Realty Earnings focuses on standalone properties reasonably than ones linked to a mall, as an example. That will increase the flexibleness of the tenant base and helps the belief diversify its buyer base.

The belief has earned a sterling fame for its dividend development historical past. A part of its attraction actually shouldn’t be solely in its precise payout historical past however the truth that these payouts are made month-to-month as a substitute of quarterly. Certainly, Realty Earnings has declared 633 consecutive month-to-month dividends, a monitor report that’s unprecedented amongst protected REITs.

Impressively, the corporate has elevated its dividend greater than 120 instances since its preliminary public providing in 1994. Consequently, Realty Earnings is a member of the Dividend Aristocrats.

Supply: Investor Presentation

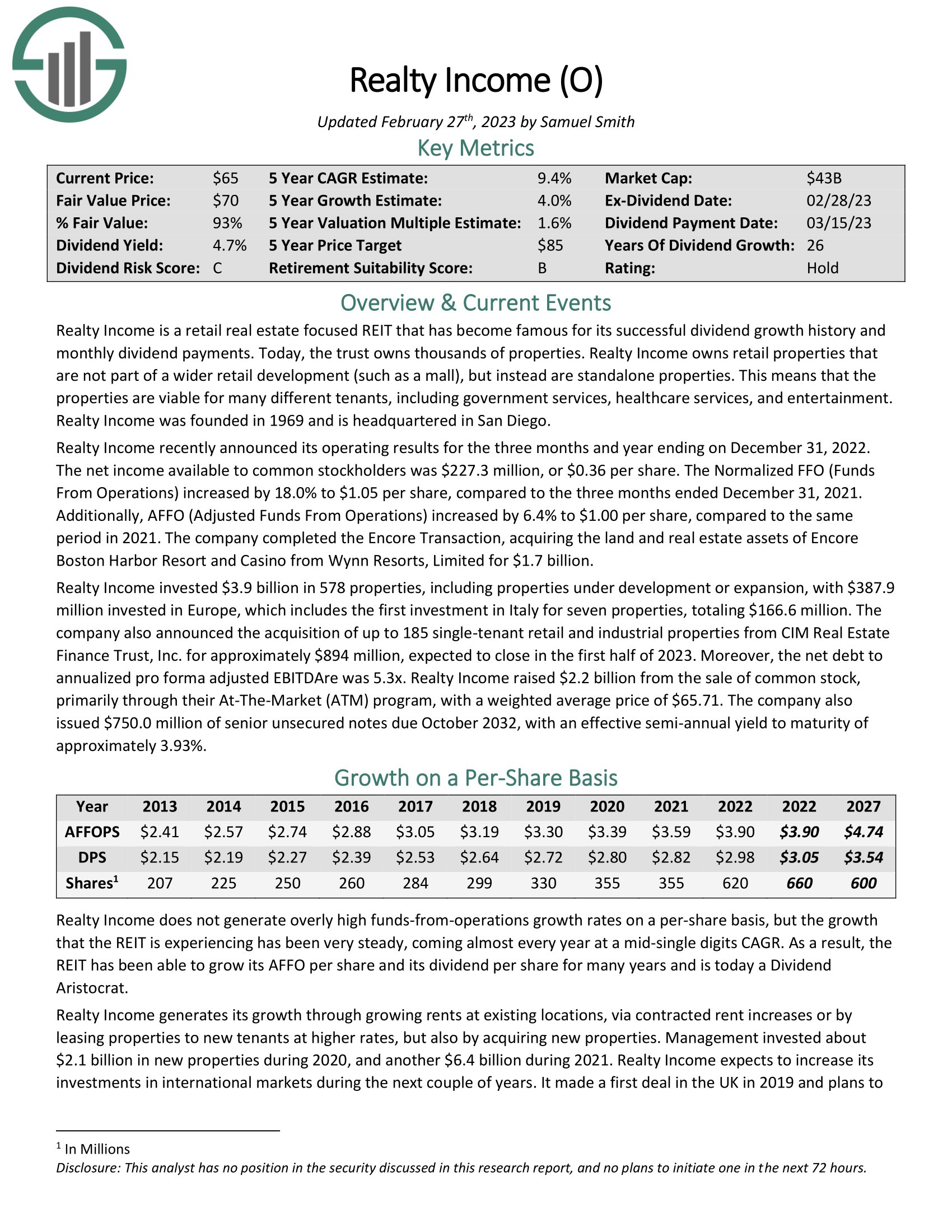

Realty Earnings not too long ago introduced its working outcomes for the three months and yr ending on December 31, 2022. The online earnings accessible to widespread stockholders was $227.3 million, or $0.36 per share. The Normalized FFO (Funds From Operations) elevated by 18.0% to $1.05 per share, in comparison with the three months ended December 31, 2021.

Moreover, AFFO (Adjusted Funds From Operations) elevated by 6.4% to $1.00 per share, in comparison with the identical interval in 2021. The corporate accomplished the Encore Transaction, buying the land and actual property property of Encore Boston Harbor Resort and On line casino from Wynn Resorts, Restricted for $1.7 billion.

Realty Earnings invested $3.9 billion in 578 properties, together with properties beneath improvement or growth, with $387.9 million invested in Europe, which incorporates the primary funding in Italy for seven properties, totaling $166.6 million.

Click on right here to obtain our most up-to-date Positive Evaluation report on O (preview of web page 1 of three proven beneath):

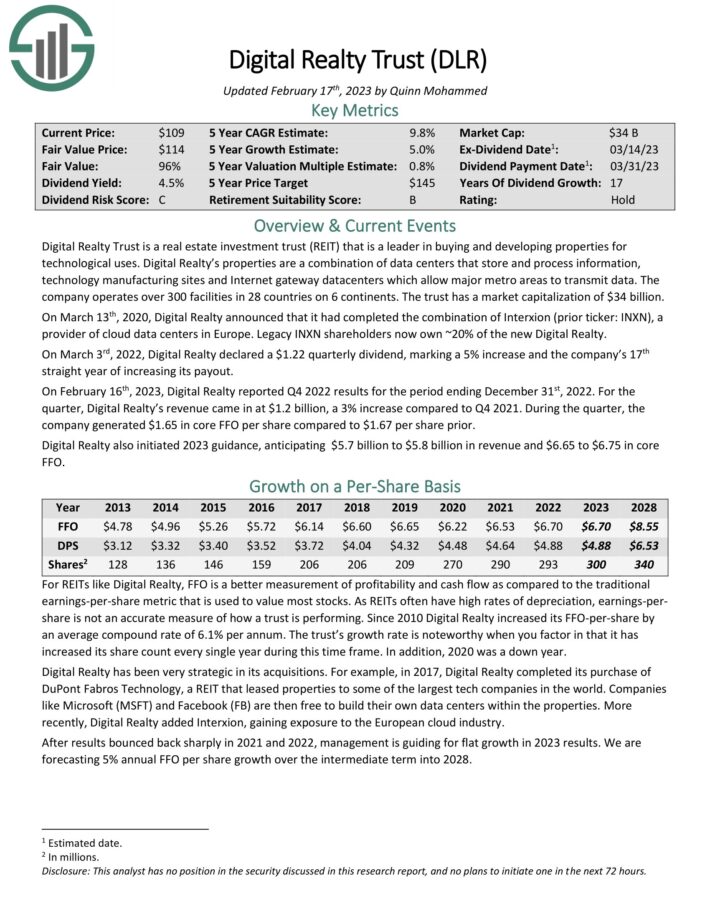

Excessive-Yield REIT No. 4: Digital Realty Belief (DLR)

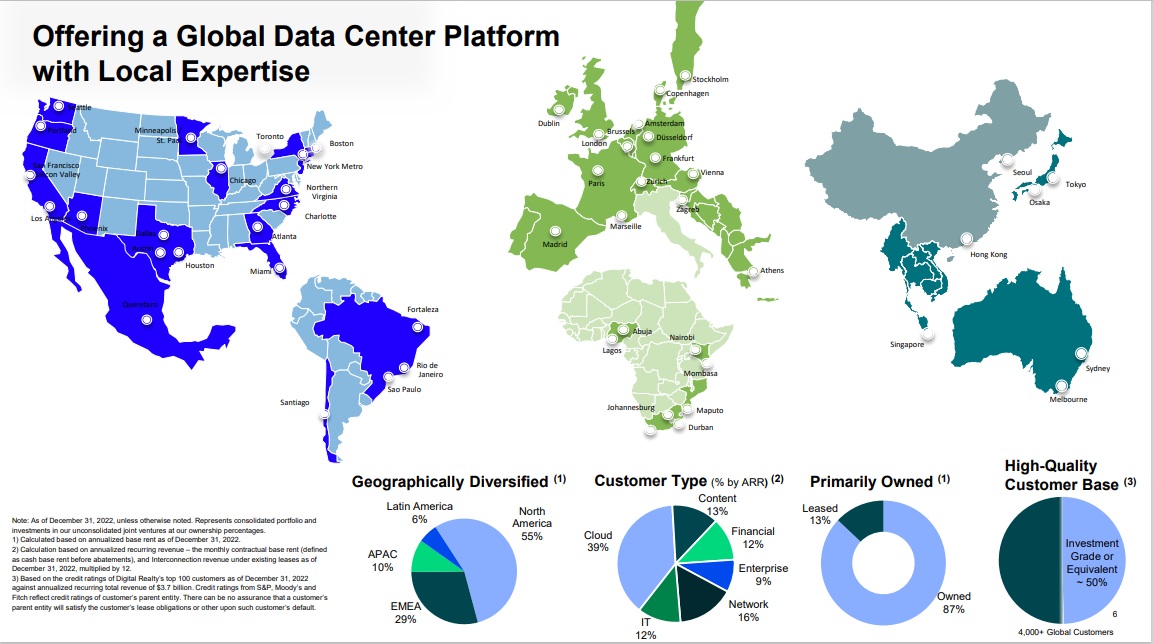

Digital Realty Belief is a REIT that may be a chief in shopping for and creating properties for technological makes use of. Digital Realty’s properties are a mixture of information facilities that retailer and course of data, know-how manufacturing websites and Web gateway information facilities which permit main metro areas to transmit information. The corporate operates over 300 amenities in 28 nations on 6 continents.

Supply: Investor Presentation

On March third, 2022, Digital Realty declared a $1.22 quarterly dividend, marking a 5% improve and the corporate’s seventeenth straight yr of accelerating its payout. On February sixteenth, 2023, Digital Realty reported This fall 2022 outcomes for the interval ending December thirty first, 2022.

For the quarter, Digital Realty’s income got here in at $1.2 billion, a 3% improve in comparison with This fall 2021. In the course of the quarter, the corporate generated $1.65 in core FFO per share in comparison with $1.67 per share prior. Digital Realty additionally initiated 2023 steering, anticipating $5.7 billion to $5.8 billion in income and $6.65 to $6.75 in core FFO.

Digital Realty is exclusive amongst protected REITs in that it affords publicity to the know-how sector.

Click on right here to obtain our most up-to-date Positive Evaluation report on Digital Realty (preview of web page 1 of three proven beneath):

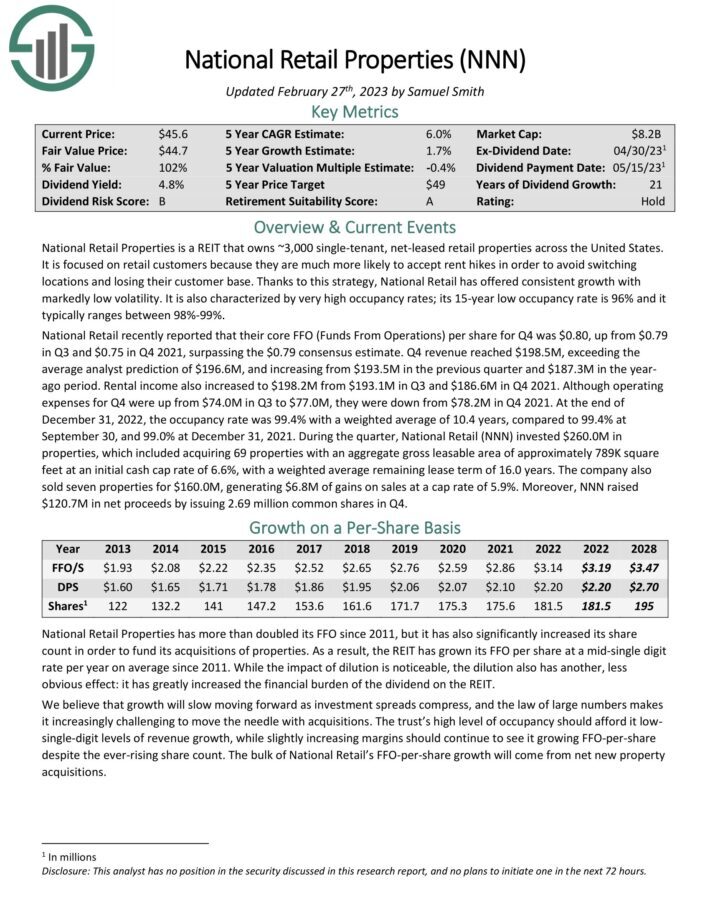

Excessive-Yield REIT No. 3: Nationwide Retail Properties (NNN)

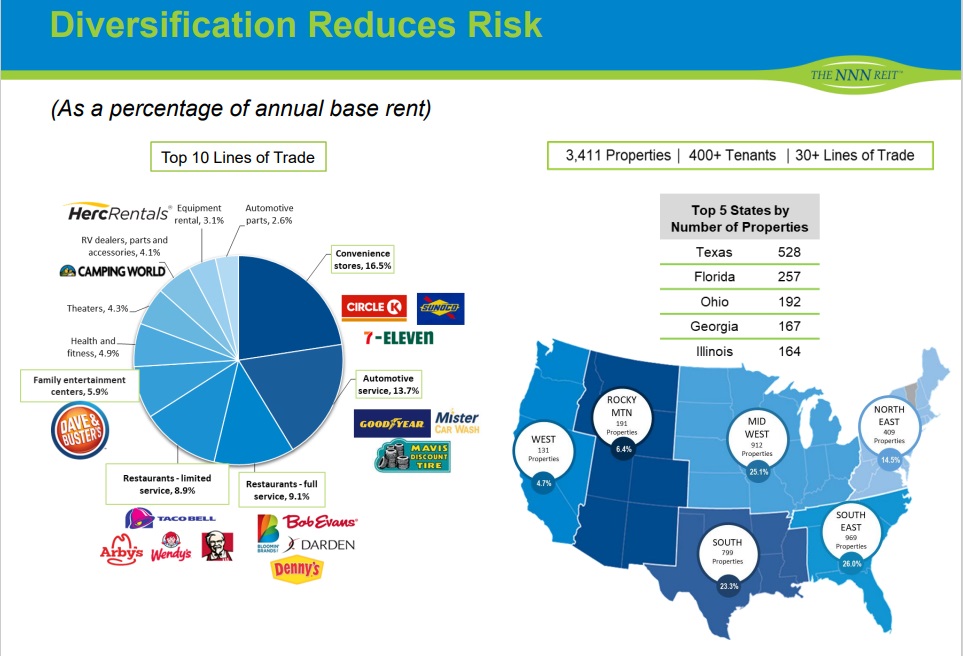

Nationwide Retail Properties is on the record of protected REITs because it owns ~3,000 single-tenant, net-leased retail properties throughout america. It’s centered on retail prospects as a result of they’re much extra more likely to settle for lease hikes with a purpose to keep away from switching areas and dropping their buyer base.

Because of this technique, Nationwide Retail has provided constant development with markedly low volatility. It’s also characterised by very excessive occupancy charges; its 15-year low occupancy charge is 96% and it sometimes ranges between 98%-99%. This is among the strongest occupancy charges among the many protected REITs.

Supply: Investor Presentation

Nationwide Retail not too long ago reported that their core FFO (Funds From Operations) per share for This fall was $0.80, up from $0.79 in Q3 and $0.75 in This fall 2021, surpassing the $0.79 consensus estimate. This fall income reached $198.5M, exceeding the common analyst prediction of $196.6M, and rising from $193.5M within the earlier quarter and $187.3M within the yearago interval.

Rental earnings additionally elevated to $198.2M from $193.1M in Q3 and $186.6M in This fall 2021. Though working bills for This fall have been up from $74.0M in Q3 to $77.0M, they have been down from $78.2M in This fall 2021.

On the finish of December 31, 2022, the occupancy charge was 99.4% with a weighted common of 10.4 years, in comparison with 99.4% at September 30, and 99.0% at December 31, 2021. In the course of the quarter, Nationwide Retail (NNN) invested $260.0M in properties, which included buying 69 properties with an mixture gross leasable space of roughly 789K sq. ft at an preliminary money cap charge of 6.6%, with a weighted common remaining lease time period of 16.0 years. The corporate additionally offered seven properties for $160.0M, producing $6.8M of positive factors on gross sales at a cap charge of 5.9%.

Click on right here to obtain our most up-to-date Positive Evaluation report on NNN (preview of web page 1 of three proven beneath):

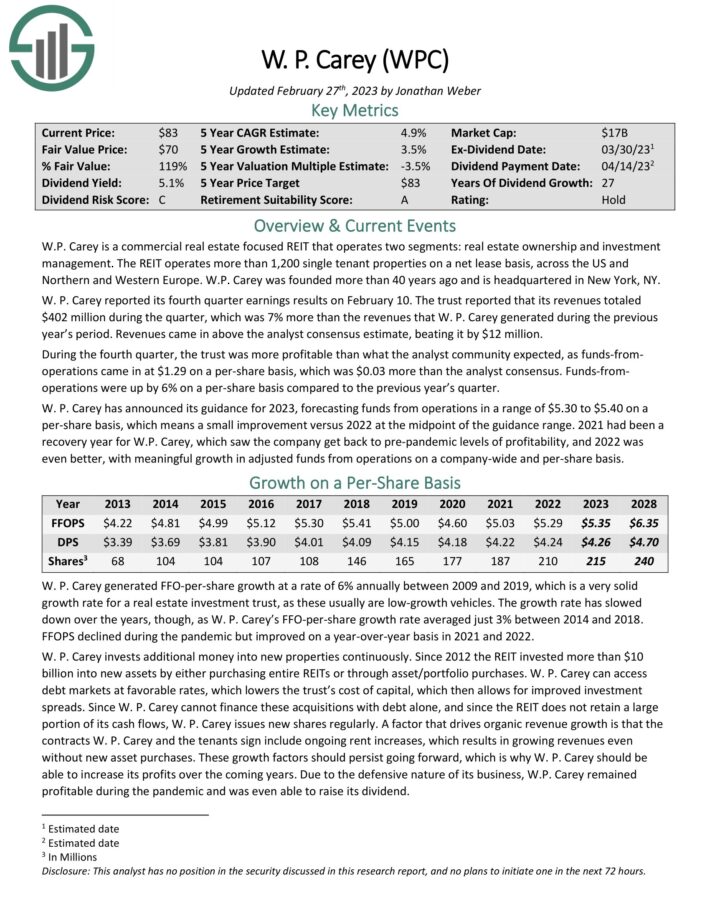

Excessive-Yield REIT No. 2: W.P. Carey (WPC)

W.P. Carey is a Actual Property Funding Belief (or REIT) with two segments: actual property possession and funding administration. The previous is the a lot bigger of the enterprise, with greater than 1,200 single-tenant properties throughout the U.S. and Northern and Western Europe.

W. P. Carey reported its fourth quarter earnings outcomes on February 10. The belief reported that its revenues totaled $402 million through the quarter, which was 7% greater than the revenues that W. P. Carey generated through the earlier yr’s interval. Revenues got here in above the analyst consensus estimate by $12 million.

In the course of the fourth quarter, funds-from operations got here in at $1.29 on a per-share foundation, which was $0.03 greater than the analyst consensus. Funds-from operations have been up by 6% on a per-share foundation in comparison with the earlier yr’s quarter.

W. P. Carey has introduced its steering for 2023, forecasting funds from operations in a variety of $5.30 to $5.40 on a per-share foundation, which suggests a small enchancment versus 2022 on the midpoint of the steering vary.

The belief has spent greater than $10 billion during the last decade buying properties to develop its portfolio. A lot of this acquisition spree has been by way of using share issuance, because the share depend has almost tripled since 2012. That being the case, development has been very regular for W.P. Carey even because the float has gotten bigger.

W.P. Carey raises its dividend barely each quarter, although the five-year CAGR is beneath 1%. Even so, the inventory has a dividend development streak of 28 years, one of many longest streaks among the many protected REITs.

Click on right here to obtain our most up-to-date Positive Evaluation report on W. P. Carey (WPC) (preview of web page 1 of three proven beneath):

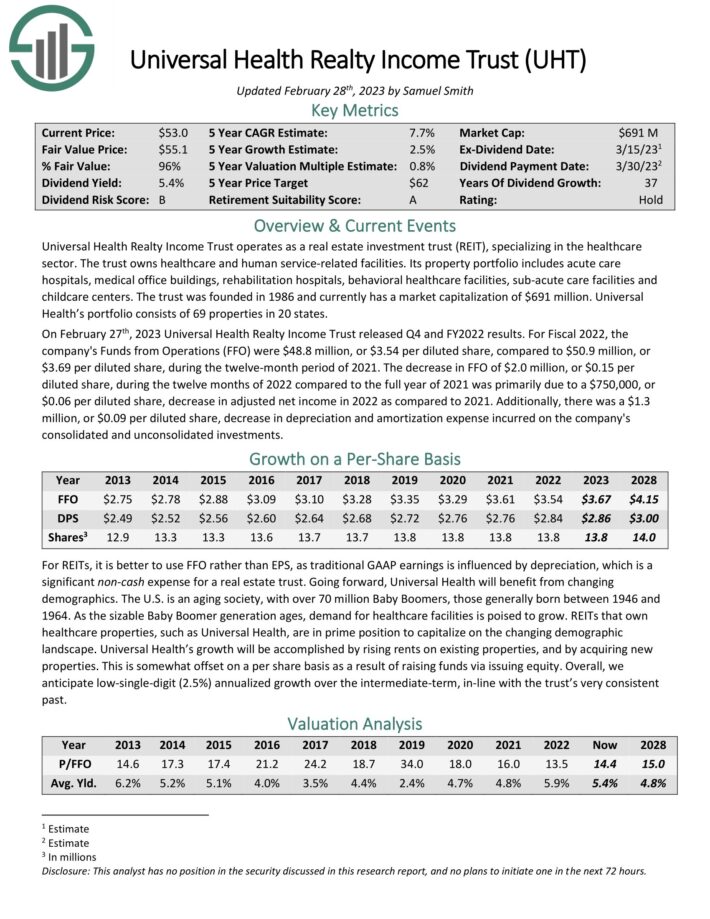

Excessive-Yield REIT No. 1: Common Well being Realty Earnings Belief (UHT)

Common Well being Realty Earnings Belief specializes within the healthcare sector. The belief owns healthcare and human service-related amenities. Its property portfolio consists of acute care hospitals, medical workplace buildings, rehabilitation hospitals, behavioral healthcare amenities, sub-acute care amenities and childcare facilities. Common Well being’s portfolio consists of 69 properties in 20 states.

On February twenty seventh, 2023 Common Well being Realty Earnings Belief launched This fall and FY2022 outcomes. For Fiscal 2022, the corporate’s Funds from Operations (FFO) have been $48.8 million, or $3.54 per diluted share, in comparison with $50.9 million, or $3.69 per diluted share, through the twelve-month interval of 2021.

Going ahead, Common Well being will profit from altering demographics. The U.S. is an growing old society, with over 70 million Child Boomers, these usually born between 1946 and 1964. Because the sizable Child Boomer technology ages, demand for healthcare amenities is poised to develop.

Protected REITs that personal healthcare properties, akin to Common Well being, are in prime place to capitalize on the altering demographic panorama. Common Well being’s development will probably be achieved by rising rents on current properties, and by buying new properties.

Click on right here to obtain our most up-to-date Positive Evaluation report on UHT (preview of web page 1 of three proven beneath):

Last Ideas

REITs are enticing for earnings traders as they sometimes have excessive dividend yields. Nonetheless, earnings traders must also choose protected REITs which have the power to pay their dividends, even when a recession happens over the subsequent yr. These 9 protected REITs have manageable debt ranges, ample money circulate to pay their dividends, and have excessive yields.

If you’re enthusiastic about discovering high-quality dividend development shares and/or different high-yield securities and earnings securities, the next Positive Dividend assets will probably be helpful:

Excessive-Yield Particular person Safety Analysis

Different Positive Dividend Assets

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].