Printed on March twenty eighth, 2023 by Aristofanis Papadatos

Figuring out cheaply valued shares is paramount in attaining excessive funding returns. Shares with low P/E ratios can supply engaging returns even when they don’t develop their earnings at a quick tempo.

On this article, we’ll focus on the prospects of 20 undervalued shares, that are at the moment buying and selling at P/E ratios below 15 and are providing dividend yields above 5.0%.

These shares are appropriate not just for worth oriented buyers but additionally for income-oriented buyers. Now we have ranked the shares by P/E ratio, from lowest to highest. For REITs, we use P/FFO rather than the P/E ratio. And for MLPs, we use P/DCF (which is distributable money flows). These are comparable metrics much like earnings for widespread shares.

You’ll be able to obtain your free copy of the Dividend Champions checklist, together with related monetary metrics like price-to-earnings ratios, dividend yields, and payout ratios, by clicking on the hyperlink under:

#1: Workplace Properties (OPI) – P/E ratio of two.5

Workplace Properties Earnings Belief is a REIT that at the moment owns greater than 160 buildings, that are positioned in 31 states and are primarily leased to single tenants with excessive credit score high quality.

Supply: Investor Presentation

The portfolio of the REIT at the moment has a 90.6% occupancy charge and a median constructing age of 17 years.

Workplace Properties generates 63% of its rental earnings from investment-grade tenants. This is likely one of the highest percentages of hire paid by investment-grade tenants within the REIT sector. Furthermore, the U.S. Authorities tenants generate roughly 20% of rental earnings whereas no different tenant accounts for greater than 4% of annual earnings. Total, Workplace Properties has an distinctive credit score profile of tenants, which leads to dependable money flows and thus constitutes a big aggressive benefit.

However, Workplace Properties has a excessive debt load, with its curiosity expense at the moment consuming basically all its working earnings. Consequently, the belief is within the strategy of promoting belongings to scale back its leverage. The deleverage course of has been taking its toll on the efficiency of the REIT over the last three years.

Attributable to its excessive debt load, Workplace Properties is susceptible to the present setting of rising rates of interest, which elevate the curiosity expense of the REIT. The market is effectively conscious of this vulnerability and thus it has punished the inventory with a 55% plunge over the past 12 months.

On the brilliant aspect, Workplace Properties has change into remarkably low-cost. The inventory is buying and selling at an all-time low price-to-FFO ratio of two.5 and is providing an all-time excessive dividend yield of 19.2%. The payout is wholesome, at 49%, however the dividend is just not protected because of the weak steadiness sheet of the REIT. However, even after a dividend reduce, the inventory shall be providing an above common yield. Total, Workplace Properties appears extremely engaging from a long-term perspective.

Click on right here to obtain our most up-to-date Certain Evaluation report on Workplace Properties (OPI) (preview of web page 1 of three proven under):

#2: Brandywine Realty Belief (BDN) – P/E ratio of three.3

Brandywine Realty Belief is a REIT that owns, develops, leases and manages an city city heart and transit-oriented portfolio which incorporates 163 properties in Philadelphia, Austin and Washington, D.C. The REIT generates 75% of its working earnings in Philadelphia, 19% of its working earnings in Austin and the remaining 6% in Washington.

Supply: Investor Presentation

As Brandywine Realty Belief generates the huge portion of its working earnings in Philadelphia and Austin, it enormously advantages from the distinctive benefits of those two areas. In accordance with official reviews, Philadelphia has the very best development charge of extremely educated residents since 2008 whereas Austin is the fastest-growing metropolitan space, the perfect place to begin enterprise and it has retrieved all the roles misplaced because of the pandemic.

Identical to most REITs, Brandywine Realty Belief is at the moment going through a powerful headwind, particularly the influence of fast-rising rates of interest on the curiosity expense of the REIT. Because of this, the inventory has plunged to a 14-year low, buying and selling at an all-time low price-to-FFO ratio of three.3.

As well as, the inventory is providing an all-time excessive dividend yield of 17.8%. The payout ratio is respectable, at 66%, however Brandywine Realty Belief has a excessive leverage ratio (Internet Debt to EBITDA) of seven.0. It additionally has a debt maturity in October-2024 and one other one in June-2026. Because of this, the dividend is more likely to come below stress within the occasion of an unexpected downturn. The excessive debt load is the first cause behind the freeze of the dividend for 17 consecutive quarters. Furthermore, Brandywine Realty Belief is delicate to recessions on account of its weak steadiness sheet and the sensitivity of its tenants to recessions. However, even when the REIT cuts its dividend, it’s going to nonetheless offer an above common yield. As well as, every time inflation and rates of interest revert to regular ranges, the inventory is more likely to rebound strongly due to its depressed valuation.

Click on right here to obtain our most up-to-date Certain Evaluation report on Brandywine Realty Belief (BDN) (preview of web page 1 of three proven under):

#3: SL Inexperienced Realty (SLG) – P/E ratio of three.7

Based in 1980, SL Inexperienced Realty is a REIT that’s centered on buying and managing business properties in Manhattan. It’s the largest workplace landlord in Manhattan, with 61 buildings which have a complete floor space of 33 million sq. ft.

SL Inexperienced Realty has been severely harm by the coronavirus disaster, which has resulted in a work-from-home development. The pandemic has subsided since final yr, however workplace house occupancy in New York stays close to historic lows. Consequently, SL Inexperienced Realty is going through an unprecedented tenant-friendly setting, and therefore it has been pressured to supply materials concessions to its tenants.

The persistence of the work-from-home development has elevated the uncertainty over the longer term development prospects of SL Inexperienced Realty. Nonetheless, we anticipate this development to attenuate within the upcoming years, because the financial slowdown will most likely enhance the negotiation energy of employers over their staff.

SL Inexperienced Realty is buying and selling at an all-time low price-to-FFO ratio of three.7 and is providing an all-time excessive dividend yield of 15.9%. The corporate has a wholesome payout ratio of 59%, however its dividend is just not protected on account of its materials debt load. However, even after a dividend reduce, the inventory will supply a beautiful yield. Total, SL Inexperienced Realty has been severely harm by a persistent work-from-home development and high-interest charges, which have elevated the curiosity expense of the REIT, however the inventory appears deeply undervalued from a long-term perspective.

Click on right here to obtain our most up-to-date Certain Evaluation report on SL Inexperienced Realty (SLG) (preview of web page 1 of three proven under):

#4: Douglas Emmett (DEI) – P/E ratio of 6.0

Douglas Emmett is a REIT that was based in 1971. It’s the largest workplace landlord in Los Angeles and Honolulu, with a 38% common market share of workplace house in its submarkets. The REIT generates 86% of its income from its workplace portfolio and 14% of its income from its multifamily portfolio. It has roughly 2,700 workplace leases in its portfolio and generates annual income of $1 billion.

The deserves of being the biggest workplace landlord in Los Angeles are apparent, as Los Angeles County is the third-largest metropolis on the earth, with GDP of $1 trillion, behind solely Tokyo and New York. The dominant place of Douglas Emmett creates operational synergies. As well as, the REIT advantages from excessive limitations to entry, which scale back competitors. Furthermore, the proximity to premier housing attracts prosperous tenants, who supply dependable money flows to the corporate.

The markets of Douglas Emmett are characterised by excessive hire development and comparatively low volatility. Rents within the West Los Angeles submarkets of the REIT have grown 150% over the past 25 years, at a 3.7% common annual charge, the very best development charge amongst all of the U.S. gateway markets. Douglas Emmett actually advantages from this development, as its leases embody 3%-5% annual hire hikes.

Supply: Investor Presentation

Sadly, Douglas Emmett has not recovered from the coronavirus disaster but, because the work-from-home development has persevered longer than initially anticipated. As well as, the REIT is harm by elevated curiosity expense, which has resulted from rising rates of interest.

Nonetheless, we view these headwinds as momentary and imagine that the inventory has change into exceptionally low-cost. Douglas Emmett is buying and selling at a 10-year low price-to-FFO ratio of 6.0, which is lower than half of the 10-year common price-to-FFO ratio of 15.5 of the inventory. Furthermore, the inventory is providing a virtually 10-year excessive dividend yield of 6.7%, with a strong payout ratio of 40%. To chop a protracted story quick, every time inflation subsides, Douglas Emmett is more likely to supply extreme returns to the buyers who can preserve a long-term perspective through the ongoing downturn.

Click on right here to obtain our most up-to-date Certain Evaluation report on Douglas Emmett (DEI) (preview of web page 1 of three proven under):

#5: Annaly Capital Administration (NLY) – P/E ratio of 6.1

Annaly Capital Administration is a diversified capital supervisor that invests in and funds residential and business belongings. The belief invests in varied varieties of company mortgage-backed securities, non-agency residential mortgage belongings, and residential mortgage loans. The belief has elected to be taxed as a REIT.

Supply: Investor Presentation

Annaly borrows funds at short-term rates of interest and invests in long-term securities. Because of this, the corporate is extraordinarily delicate to the underlying rates of interest and the yield curve, i.e., the distinction between long-term and short-term rates of interest.

Annaly is at the moment going through an ideal storm because of the aggressive rate of interest hikes carried out by the Fed in an effort to revive inflation to regular ranges. As a result of efforts of the Fed to chill the financial system, short-term rates of interest have risen above long-term rates of interest. In different phrases, the market predicts {that a} recession will present up eventually.

As Annaly borrows funds at short-term rates of interest and invests funds at long-term charges, it has change into extraordinarily exhausting for the corporate to make worthwhile new offers below the prevailing circumstances. However, the corporate is more likely to stay worthwhile due to its existent funding portfolio. As well as, many of the harm has most likely been achieved in reference to the inventory worth, because the Fed is just not more likely to elevate rates of interest a lot additional.

Annaly is at the moment buying and selling at a price-to-earnings ratio of solely 6.1 and is providing an exceptionally excessive dividend yield of 13.7%. Whereas its dividend is much from protected, it’s more likely to stay excessive even within the occasion of a dividend reduce. Given a budget valuation of the inventory, its excessive dividend and the truth that the more severe appears to be behind, Annaly is more likely to extremely reward affected person buyers within the upcoming years.

Click on right here to obtain our most up-to-date Certain Evaluation report on Annaly Capital Administration (NLY)(preview of web page 1 of three proven under):

#6: Chimera Funding Company (CIM) – P/E ratio of 6.1

Chimera Funding Company is a REIT that could be a specialty finance firm. It invests by its subsidiaries in a diversified portfolio of mortgage belongings, together with residential mortgage loans, non-agency residential mortgage belongings, and different actual property associated securities.

Supply: Investor Presentation

The revenue of Chimera is set by the distinction between the yield of its investments, which is dependent upon long-term rates of interest, and the rate of interest paid for its borrowed funds, which is dependent upon short-term rates of interest. Because of this, the corporate is extraordinarily delicate to the underlying rates of interest and the yield curve, i.e., the distinction between long-term and short-term rates of interest.

Identical to Annaly, Chimera has been severely harm by the aggressive rate of interest hikes carried out by the Fed since early final yr. As a result of efforts of the Fed to chill the financial system, short-term rates of interest have risen above long-term rates of interest. In different phrases, the market expects a recession to indicate up within the close to future.

The adverse slope of the yield curve has made it extraordinarily exhausting for Chimera to make a revenue in new transactions. However, the corporate is more likely to stay worthwhile due to its existent funding portfolio. As well as, many of the harm has most likely been achieved, because the Fed is just not more likely to elevate rates of interest a lot additional.

Chimera is buying and selling at a remarkably low P/E ratio of 6.1 and is providing a 10-year excessive dividend yield of 16.9%. Given the intense payout ratio of 102% and the vulnerability of Chimera to the present investing setting, its dividend is much from protected. However, even after a dividend reduce, the inventory will nonetheless offer an above common yield. Because of its low-cost valuation, the inventory is engaging from a long-term perspective, significantly provided that the more severe appears to be behind the corporate.

Click on right here to obtain our most up-to-date Certain Evaluation report on Chimera Funding Company (CIM) (preview of web page 1 of three proven under):

#7: Walgreens Boots Alliance (WBA) – P/E ratio of seven.3

Walgreens Boots Alliance is the biggest retail pharmacy in each the U.S. and Europe. By its flagship Walgreens enterprise and different enterprise ventures, the corporate is current in additional than 9 international locations, with greater than 13,000 shops within the U.S., Europe and Latin America.

Walgreens has grown its earnings per share by 7.6% per yr on common over the past decade nevertheless it has stalled over the past 5 years, principally on account of heating competitors, which has taken its toll on the margins of the corporate. As well as, the revenue margins within the pharmaceutical enterprise have change into an object below scrutiny lately. Because of this, buyers shouldn’t anticipate significant margin enlargement for the foreseeable future.

Walgreens can be going through one other headwind, particularly the fading constructive impact of the pandemic. Within the first quarter of 2023, the corporate executed solely 8.4 million vaccinations, which have been a lot decrease than the 11.8 million vaccinations within the second quarter of 2022. Because of this, whole revenues decreased 1.5% and adjusted earnings per share plunged 30% over the prior yr’s quarter.

Supply: Investor Presentation

It is usually exceptional that Walgreens did not obtain a beautiful bid for its Boots enterprise. Attributable to its lackluster development prospects, Walgreens has been punished to the intense by the market. The inventory is at the moment buying and selling at a 10-year low P/E ratio of seven.3, which is about half of its 10-year common P/E ratio.

Furthermore, Walgreens has raised its dividend for 47 consecutive years and is at the moment providing a virtually 10-year excessive dividend yield of 5.9%. The corporate has a strong payout ratio of 42%, a wholesome steadiness sheet and it has proved resilient to recessions due to the important nature of its enterprise. Subsequently, buyers can lock within the exceptionally excessive dividend yield of the inventory and relaxation assured that the dividend is protected. Given additionally the extraordinarily low-cost valuation of Walgreens, we view the inventory as extremely engaging for affected person buyers.

Click on right here to obtain our most up-to-date Certain Evaluation report on Walgreens Boots Alliance (WBA) (preview of web page 1 of three proven under):

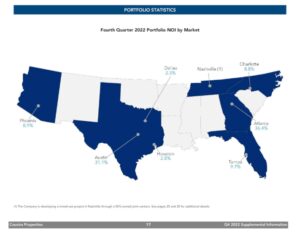

#8: Cousins Properties (CUZ) – P/E ratio of seven.4

Cousins Properties is a self-managed REIT that was based in 1958 and acquires, develops and leases workplace buildings in high-growth Solar Belt markets.

Supply: Investor Presentation

The belief generates 36% of its working earnings in Atlanta and 31% of its working earnings in Austin. Solar Belt markets are engaging due to their superior financial development in comparison with most different areas of the U.S.

Cousins Properties has been harm by the coronavirus disaster, which has led many firms to undertake a work-from-home mannequin. This downturn has caught the REIT with a excessive debt load and therefore the belief has been pressured to promote some properties to be able to endure the disaster. Its whole rentable sq. ft have decreased in every of the final three years. Furthermore, the belief has a excessive leverage ratio (Internet Debt to EBITDA) of 4.9. However, we imagine that the more severe is behind the corporate.

Aside from the work-from-home development, Cousins Properties is now going through one other sturdy headwind, particularly rising curiosity expense on account of fast-rising rates of interest. Administration just lately supplied steering for an approximate 5% lower in FFO per unit in 2023, primarily on account of larger curiosity expense.

Whereas Cousins Properties is going through hostile enterprise circumstances proper now, buyers ought to be aware that the inventory has change into remarkably low-cost. The REIT is buying and selling at a 10-year low price-to-FFO ratio of seven.4, which is much decrease than the 10-year common price-to-FFO ratio of 12.7 of the inventory. As well as, the inventory is providing a 10-year excessive dividend yield of 6.7%, with a wholesome payout ratio of 49%. As a result of weak steadiness sheet of the corporate, the dividend is just not totally protected. Nonetheless, every time inflation and rates of interest revert to regular ranges, Cousins Properties is more likely to extremely reward buyers off its present depressed inventory worth.

Click on right here to obtain our most up-to-date Certain Evaluation report on Cousins Properties (CUZ) (preview of web page 1 of three proven under):

#9: AT&T (T) – P/E ratio of seven.6

AT&T is a diversified, world chief in telecommunications, serving greater than 100 million clients. Nearly a yr in the past, AT&T accomplished the spin-off of WarnerMedia.

AT&T is a colossal enterprise, which generates roughly $120 billion of annual revenues. Nonetheless, the corporate has grown its earnings per share by solely 0.3% per yr on common over the past decade. Because of this, the inventory has dramatically underperformed the broad market over the past decade; it has shed 33% whereas the S&P 500 has rallied 153%.

The poor efficiency of AT&T has resulted primarily from some markedly poor investing selections. AT&T acquired DirecTV for $65 billion in 2015, near the height of the enterprise of the acquired firm. After having misplaced about 10 million subscribers, AT&T spun off DirecTV, with an implied enterprise worth of solely $16.25 billion. The same state of affairs was evidenced with Time Warner, which AT&T acquired in 2018 however spun off final yr. In each conditions, AT&T purchased excessive and bought low, thus decreasing shareholder worth.

Attributable to its poor efficiency file, AT&T is now buying and selling at a virtually 10-year low P/E ratio of seven.6. A budget valuation has resulted in an above common dividend yield of 6.0%. We imagine that AT&T has change into exceptionally engaging from a long-term viewpoint.

After a collection of failed investments, AT&T is now specializing in its core enterprise. Because of this, the corporate has already begun to enhance its efficiency.

Supply: Investor Presentation

At any time when the market appreciates the virtues of the lean enterprise mannequin of AT&T, it’s more likely to reward the inventory with a better P/E ratio.

Click on right here to obtain our most up-to-date Certain Evaluation report on AT&T (T) (preview of web page 1 of three proven under):

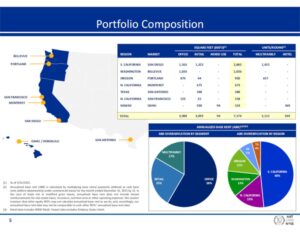

#10: American Property Belief (AAT) – P/E ratio of seven.6

American Property Belief is a REIT that was shaped in 2011 as a successor of American Property, a privately held firm based in 1967. American Property Belief is headquartered in San Diego, California, and has nice expertise in buying, enhancing and growing workplace, retail and residential properties all through the U.S., primarily in Southern California, Northern California, Oregon, Washington and Hawaii.

Its workplace portfolio and its retail portfolio comprise of roughly 4.0 million and three.1 million sq. ft, respectively.

Supply: Investor Presentation

American Property Belief additionally owns greater than 2,000 multifamily models.

The expansion technique of American Property Belief includes the acquisition of properties in submarkets with favorable provide and demand traits, together with excessive limitations to entry. As well as, the REIT redevelops lots of its newly-acquired properties to be able to improve their worth. It additionally has a capital recycling technique, which includes promoting properties whose returns appear to have been maximized and shopping for high-return properties.

Thanks to those development drivers, American Property Belief has grown its FFO per unit each single yr over the past decade, apart from 2020 because of the pandemic. The REIT has grown its FFO per unit at a 4.4% common annual charge throughout this era. Furthermore, it proved pretty resilient to the pandemic and has already recovered from that disaster.

American Property Belief seems resilient to excessive inflation due to its means to boost rental charges considerably yearly. However, it has decelerated recently, because it has begun to face robust comparisons over exceptionally sturdy ends in the prior yr’s interval. Because of this, the inventory has been punished by the market.

American Property Belief is at the moment buying and selling at a 10-year low price-to-FFO ratio of seven.6, which is lower than half of the 5-year common price-to-FFO ratio of 17.1 of the inventory. As well as, the inventory is providing a 10-year excessive dividend yield of seven.7%. Given the wholesome payout ratio of 59% and the dependable development trajectory of the REIT, the dividend is protected. The one concern is the fabric debt load of the REIT, which has an curiosity protection ratio of solely 2.0.

On the brilliant aspect, American Property Belief has acquired funding grade scores from the main score businesses. Given the promising development potential of the REIT, we don’t anticipate it to face any issues servicing its debt. Subsequently, we anticipate American Property Belief to supply extreme returns to buyers every time the financial system recovers from its newest slowdown.

Click on right here to obtain our most up-to-date Certain Evaluation report on American Property Belief (AAT) (preview of web page 1 of three proven under):

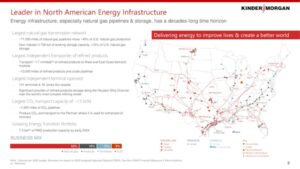

#11: Kinder Morgan (KMI) – P/E ratio of seven.9

Kinder Morgan is among the many largest power firms within the U.S. It’s engaged in storage and transportation of oil and gasoline and different merchandise. It owns an curiosity in or operates roughly 83,000 miles of pipelines and 140 terminals.

Supply: Investor Presentation

Kinder Morgan has a strong enterprise mannequin, because it generates almost all its money flows from fee-based contracts and minimum-volume contracts. The corporate generates almost 70% of its working earnings from minimum-volume contracts. In different phrases, its clients pay a minimal quantity to Kinder Morgan yearly even when they transport a lot decrease volumes than regular.

Furthermore, Kinder Morgan is resilient to the secular shift from fossil fuels to scrub power sources. Whereas oil firms are susceptible to this shift, which has enormously accelerated within the final three years, Kinder Morgan is concentrated totally on pure gasoline, which is a a lot cleaner gas than oil merchandise. Because of this, all of the environmental insurance policies that intention to scale back oil consumption don’t intention to scale back pure gasoline consumption and therefore Kinder Morgan is hardly affected by environmental insurance policies.

The resilience of Kinder Morgan was additionally proved all through the coronavirus disaster. Most oil firms incurred extreme losses in 2020 because of the collapse of the costs of oil and gasoline in that yr. Quite the opposite, Kinder Morgan incurred simply an 8% lower in its distributable money circulation (DCF) per unit in that yr. An 8% lower in one of many fiercest downturns of the power sector is actually admirable. Furthermore, the corporate recovered strongly in 2021, with a file distributable money circulation per unit in that yr.

Kinder Morgan is at the moment buying and selling at a beautiful price-to-DCF ratio of seven.9. The corporate has raised its dividend for five consecutive years and it’s providing an above common dividend yield of 6.6%. Because of its strong payout ratio of 52% and its defensive enterprise mannequin, Kinder Morgan is more likely to maintain elevating its dividend for a lot of extra years. Subsequently, buyers ought to benefit from its exceptionally excessive yield and low-cost valuation.

Click on right here to obtain our most up-to-date Certain Evaluation report on Kinder Morgan (KMI) (preview of web page 1 of three proven under):

#12: Verizon (VZ) – P/E ratio of 8.0

Verizon, which was created by the merger of Bell Atlantic with GTE in 2000, is likely one of the largest wi-fi carriers within the nation. Wi-fi generates three-quarters of the full revenues of the corporate whereas broadband and cable providers account for a few quarter of gross sales. The community of Verizon covers roughly 300 million individuals and 98% of the U.S.

Verizon enjoys a key aggressive benefit, particularly its popularity as the perfect wi-fi service within the U.S. That is clearly mirrored within the wi-fi web additions of the corporate and its exceptionally low churn charge. This dependable service permits Verizon to take care of its buyer base and transfer some clients to higher-priced plans.

Verizon reveals lackluster enterprise momentum proper now. Final yr, the corporate posted basically flat gross sales and noticed its earnings per share dip 6% on account of excessive working bills in addition to excessive curiosity expense. Verizon has supplied steering for earnings per share of $4.55-$4.85 in 2023, implying an additional 7% lower.

Supply: Investor Presentation

However, it is very important be aware that the inventory has change into exceptionally low-cost. To make sure, Verizon is at the moment buying and selling at a virtually 10-year low P/E ratio of 8.0 and is providing a 10-year excessive dividend yield of 6.9%. Because of the strong payout ratio of 56%, the sturdy enterprise place of the corporate and its resilience to recessions, its dividend needs to be thought-about protected. It is usually price noting that Verizon has grown its dividend for 18 consecutive years. Total, every time Verizon returns to development mode, it’s more likely to supply extreme returns to those that buy the inventory round its present inventory worth.

Click on right here to obtain our most up-to-date Certain Evaluation report on Verizon (VZ) (preview of web page 1 of three proven under):

#13: Altria (MO) – P/E ratio of 8.8

Altria is a client staples large, with a historical past of 175 years. The corporate is the producer of the top-selling cigarette model on the earth, particularly Marlboro, in addition to some non-smokeable merchandise. The tobacco large has maintained a market share of about 40%-43% for a number of years in a row.

Supply: Investor Presentation

Altria additionally has giant stakes in world beer large Anheuser Busch InBev (BUD) and Cronos Group (CRON), a hashish firm.

Altria has a rock-solid enterprise mannequin in place. Because of the inelastic demand for its merchandise, the corporate has been elevating its costs yr after yr. Because of this, it has greater than offset the impact of the steadily declining consumption per capita of cigarettes on its earnings. Because of its sturdy pricing energy, Altria has grown its earnings per share each single yr over the past decade, at an 8.8% common annual charge. The constant development file of Altria is a testomony to the energy of its enterprise mannequin.

However, Altria has been caught off-guard within the ongoing transition of customers in the direction of different tobacco merchandise, reminiscent of vaping merchandise. About 5 years in the past, Altria acquired a 35% stake in Juul, a frontrunner in vaping merchandise, for $12.8 billion however that funding proved disastrous. After the acquisition, Juul incurred a number of hits on account of restrictions from regulatory authorities. The corporate can be going through extreme potential fines from regulators sooner or later. Consequently, Altria just lately divested its stake in Juul and thus its entire funding within the firm evaporated.

Attributable to its failed funding and its weak place in different tobacco merchandise, Altria is at the moment buying and selling at a virtually 10-year low price-to-earnings ratio of 8.8 and is providing a virtually 10-year excessive dividend yield of 8.6%, with a 10-year low payout ratio of 75%. The inventory has change into extraordinarily low-cost. It is usually exceptional that Altria continues rising its earnings per share to new all-time highs yr after yr. The corporate is on monitor to develop its backside line by about 4% this yr. At any time when the market shift its concentrate on the rock-solid enterprise mannequin of Altria, the inventory is more likely to supply extreme returns to its shareholders off its present depressed worth.

Click on right here to obtain our most up-to-date Certain Evaluation report on Altria (MO) (preview of web page 1 of three proven under):

#14: V.F. Company (VFC) – P/E ratio of 9.7

V.F. Company has a historical past of greater than a century and is likely one of the largest attire, footwear and equipment firms on the earth. Its manufacturers embody The North Face, Vans, Timberland and Dickies.

V.F. Company is at the moment going through a extreme downturn because of the a number of influence of almost 40-year excessive inflation on the inventory. Extreme inflation has pronouncedly elevated the price of uncooked supplies, the freight prices and the labor prices of V.F. Company. Consequently, it exerts nice stress on the working margins of the retailer.

As well as, because of the influence of inflation on the true buying energy of customers, the latter have change into conservative of their spending. Because of this, the inventories of V.F. Company have almost doubled over the prior yr. This has led the corporate to supply deep reductions in an effort to scale back its stock to more healthy ranges and thus the working margins of V.F. Company are below nice stress.

Supply: Investor Presentation

As a result of influence of sky-high inflation on its enterprise, V.F. Company just lately reduce its dividend by 41%, after 50 consecutive years of dividend development. However, the inventory continues to be providing a virtually 10-year excessive dividend yield of 5.9%. It additionally has a strong payout ratio of 57% and a rock-solid steadiness sheet and therefore its new dividend needs to be thought-about protected.

Furthermore, V.F. Company is buying and selling at a recent 10-year low, at a virtually 10-year low P/E ratio of 9.7. Moreover, the Fed is set to revive inflation to its goal stage of two%. Because of the aggressive stance of the Fed, inflation has subsided each month because it peaked final summer time. When inflation reverts to regular ranges, V.F. Company is more likely to get pleasure from a powerful rebound in its enterprise and thus it’s going to most likely extremely reward affected person buyers.

Click on right here to obtain our most up-to-date Certain Evaluation report on V.F. Company (VFC) (preview of web page 1 of three proven under):

#15: Lazard (LAZ) – P/E ratio of 10.0

Lazard is a monetary advisory firm, with a historical past of 175 years and operations in 43 cities worldwide.

Supply: Investor Presentation

The corporate has two enterprise divisions, particularly Monetary Advisory and Asset Administration. The previous contains investor analytics, debt issuance, mergers and acquisitions, debt restructuring, chapter 11 and capital raises whereas the latter is concentrated totally on institutional shoppers.

Lazard has an awesome popularity in its enterprise, as it’s thought-about probably the most dependable firms within the monetary world. When an organization or a rustic faces monetary issues, it typically consults Lazard to be able to consider its choices and restructure its debt in essentially the most environment friendly means. The shoppers of Lazard pay considerable quantities to the corporate for its consulting providers however they earn much more due to the experience of Lazard.

Lazard is more likely to incur a decline in its earnings this yr because of the world financial slowdown brought on by the rate of interest hikes carried out by most central banks, the resultant lower in belongings below administration and the lowered transaction exercise of the shoppers of the corporate.

With that mentioned, the inventory has change into exceptionally low-cost. Lazard is at the moment buying and selling at a virtually 10-year low P/E ratio of 10.0 and is providing a 10-year excessive dividend yield of 6.1%. Lazard has an honest payout ratio of 61% and a powerful steadiness sheet, with a BBB+ credit standing from S&P and Fitch. Furthermore, the corporate doesn’t have any debt maturities till 2025 whereas administration has repeatedly affirmed its dedication for a rising dividend. Given additionally its dependable enterprise mannequin, Lazard is just not more likely to reduce its 6.1% dividend. Total, the inventory is more likely to supply extreme returns to buyers every time the worldwide financial system exhibits indicators of restoration from its newest slowdown.

Click on right here to obtain our most up-to-date Certain Evaluation report on Lazard (LAZ) (preview of web page 1 of three proven under):

#16: Easterly Authorities Properties (DEA) – P/E ratio of 11.1

Easterly Authorities Properties is an internally managed REIT with a concentrate on acquisition, growth and administration of properties that are leased to U.S. Authorities businesses. Many of the properties of the REIT are leased to U.S. authorities businesses, such because the FBI, IRS, and DEA.

Easterly Authorities Properties has discovered a profitable area of interest in the true property enterprise and has been working to change into a model title in its discipline of U.S. Authorities leasing. Its operations are considered as protected investments, because the U.S. authorities is essentially the most dependable tenant a landlord can discover. Throughout the U.S. Authorities, Easterly Authorities Properties leases to predominantly businesses that are thought-about as important providers. This helps clarify how the belief has been in a position to obtain an impressive 100% occupancy charge. Furthermore, the REIT has well-laddered lease maturities.

Supply: Investor Presentation

Sadly, Easterly Authorities Properties has a considerably lackluster efficiency file, because it has did not develop its FFO per unit meaningfully over the past 5 years. However, the inventory is markedly cheaply valued. It’s buying and selling at an 8-year low price-to-FFO ratio of 11.1 and is providing an 8-year excessive dividend yield of 8.3%. The payout ratio is excessive, at 93%, however the dividend could also be sustained due to the defensive enterprise mannequin of the REIT. We anticipate the inventory to rebound strongly every time inflation reverts to its long-term vary.

Click on right here to obtain our most up-to-date Certain Evaluation report on Easterly Authorities Properties (DEA) (preview of web page 1 of three proven under):

#17: 3M Firm (MMM) – P/E ratio of 11.5

3M Firm sells greater than 60,000 merchandise, that are used day-after-day in properties, hospitals, workplace buildings and faculties all over the world. The economic producer has presence in additional than 200 international locations.

3M has a key aggressive benefit, particularly its exemplary division of Analysis & Growth (R&D). The corporate has persistently spent 5%-6% of its whole revenues (almost $2 billion per yr) on R&D to be able to create new merchandise and thus meet altering client wants. This technique has actually born fruit, because it has resulted in a portfolio of greater than 100,000 patents. Because of its concentrate on innovation, 3M generates almost one-third of its revenues from merchandise that didn’t exist 5 years in the past.

3M is at the moment going through a headwind on account of excessive price inflation. Nonetheless, due to its dominant enterprise place, the corporate has sturdy pricing energy. Because of this, it has been in a position to cross its elevated prices to its clients by way of materials worth hikes. That is clearly mirrored within the enterprise efficiency of 3M, as the corporate posted almost all-time excessive earnings per share in 2022.

3M is a Dividend King, with one of many longest dividend development streaks within the investing universe. The corporate has raised its dividend for 64 consecutive years and is at the moment providing a 10-year excessive dividend yield of 5.9%. The inventory can be buying and selling at a 10-year low P/E ratio of 11.5.

The exceptionally low-cost valuation of 3M has resulted from a powerful headwind, particularly quite a few pending lawsuits. There are almost 300,000 claims that its earplugs, which have been utilized by U.S. fight troops and have been manufactured by Aearo Applied sciences, a subsidiary of 3M, have been faulty. The subsidiary of 3M filed for chapter however a U.S. choose dominated that this chapter wouldn’t stop lawsuits from burdening 3M. Because of this, no-one can predict the ultimate quantity of liabilities that 3M must pay to its plaintiffs.

However, due to its rock-solid steadiness sheet, 3M is more likely to show able to enduring this headwind and rising stronger after this disaster is over. 3M has an curiosity protection ratio of 12.1 and web debt to market cap of solely 32%.

Supply: Investor Presentation

Given additionally its wholesome payout ratio of 58% and its dependable enterprise efficiency, 3M is more likely to proceed elevating its dividend for a lot of extra years.

Click on right here to obtain our most up-to-date Certain Evaluation report on 3M Firm (MMM) (preview of web page 1 of three proven under):

#18: LTC Properties (LTC) – P/E ratio of 12.2

LTC Properties is a REIT that invests in senior housing and expert nursing properties. Its portfolio consists of roughly 50% senior housing and 50% expert nursing properties. The REIT owns 216 investments in 29 states with 32 working companions.

Supply: Investor Presentation

LTC Properties has been harm by the chapter of Senior Care Facilities, which is the biggest expert nursing operator in Texas. Senior Care filed for Chapter 11 chapter in December-2018. Till 2018, it was producing 9.7% of the annual revenues of LTC Properties and was the fifth largest buyer of the belief.

On the brilliant aspect, LTC Properties has most of its belongings in states with the very best projected will increase within the 80+ inhabitants cohort over the subsequent decade. Furthermore, LTC Properties is at the moment recovering from the coronavirus disaster.

LTC Properties is at the moment providing a 10-year excessive dividend yield of 6.9%. The REIT has raised its dividend at a 2.3% common annual charge over the past decade. Nonetheless, it has frozen its dividend within the final six years because of the absence of underlying development. Consequently, it’s prudent to not anticipate dividend development anytime quickly. The payout ratio is 84% and the steadiness sheet is leveraged, with a debt to adjusted EBITDA ratio of 5.0 and an curiosity protection ratio of three.5. Because of this, the dividend might come below stress if LTC Properties faces a powerful headwind, reminiscent of a recession. Thankfully, the REIT doesn’t have materials debt maturities for the subsequent 5 years.

Furthermore, LTC Properties is buying and selling at a 10-year low price-to-FFO ratio of 12.2, which is way decrease than the 10-year common price-to-FFO ratio of 15.1 of the inventory. The exceptionally low-cost valuation has resulted primarily from the impact of excessive rates of interest on the curiosity expense of the REIT. At any time when rates of interest normalize, the inventory is more likely to get pleasure from a powerful rally off its depressed worth.

Click on right here to obtain our most up-to-date Certain Evaluation report on LTC Properties (LTC)(preview of web page 1 of three proven under):

#19: Philip Morris (PM) – P/E ratio of 14.8

Philip Morris was shaped when its father or mother firm Altria spun off its worldwide operations. Philip Morris sells cigarettes below the Marlboro model and others manufacturers in worldwide markets.

Philip Morris has probably the most helpful cigarette manufacturers on the earth, Marlboro, and is a frontrunner within the reduced-risk product class with iQOS.

Supply: Investor Presentation

Because of its sturdy enterprise place, it’s a low-risk enterprise. The one materials danger comes from potential restrictions from regulatory authorities however Philip Morris is safer than many different tobacco firms on this regard due to its broad geographic diversification.

Philip Morris has grown its dividend for 15 consecutive years and is at the moment providing a virtually 10-year excessive dividend yield of 5.6%. Its payout ratio is just too excessive, at 83%, however the firm is probably going to have the ability to defend its dividend now that its previous investments have begun to bear fruit and capital necessities have decreased sharply. However, it’s prudent for buyers to be ready for modest dividend development going ahead.

However, due to the sturdy enterprise momentum of its different tobacco merchandise, Philip Morris expects to develop its currency-neutral earnings per share by about 6% this yr, from $5.81 to an all-time excessive of $6.09-$6.21. Furthermore, the inventory is buying and selling at a virtually 10-year low P/E ratio of 14.8. This earnings a number of is exceptionally low for this inventory, which has at all times loved a premium valuation due to its sturdy enterprise mannequin and its beneficiant dividends. The earnings of the corporate have been harm by a powerful greenback however we anticipate the market to reward the inventory with a better P/E ratio every time the greenback depreciates vs. the opposite main currencies.

Click on right here to obtain our most up-to-date Certain Evaluation report on Philip Morris (PM) (preview of web page 1 of three proven under):

#20: Realty Earnings (O) – P/E ratio of 15.0

Realty Earnings is a retail REIT that’s well-known for its excellent dividend development historical past. The belief owns greater than 4,000 retail properties.

Many buyers keep away from retail REITs because of the secular shift of customers from brick-and-mortar procuring to on-line purchases. Nonetheless, Realty Earnings continues to thrive within the present enterprise panorama. The REIT owns retail properties that aren’t a part of a wider retail growth, reminiscent of a mall, however are standalone properties. Because of this, the properties of Realty Earnings can appeal to a number of varieties of tenants and therefore the corporate is basically proof against the secular decline of brick-and-mortar retailers.

The important thing aggressive benefit of Realty Earnings is its exemplary administration, which has nice experience in figuring out high-return properties. Because of its strong development technique, Realty Earnings has grown its FFO per unit each single yr over the past decade, at a 5.5% common annual charge. It has achieved such a constant development file due to the acquisition of high-return properties and predictable hire hikes yr after yr.

Furthermore, Realty Earnings has proved extraordinarily resilient to recessions. Within the Nice Recession, whereas different REITs reduce their dividends, Realty Earnings continued rising its dividend. The REIT has raised its dividend for 100 consecutive quarters.

Realty Earnings has grown its dividend at a 4.4% common annual charge since 1994, with 119 dividend hikes since then.

Supply: Investor Presentation

The REIT is at the moment providing a virtually 10-year excessive dividend yield of 5.0% and is buying and selling at a virtually 10-year low price-to-earnings ratio of 15.0. The exceptionally low-cost valuation of the inventory has resulted primarily from the influence of inflation on the current worth of future money flows and the impact of excessive rates of interest on curiosity expense. At any time when inflation and rates of interest revert to regular ranges, Realty Earnings will nearly actually supply extreme returns.

Click on right here to obtain our most up-to-date Certain Evaluation report on Realty Earnings (O) (preview of web page 1 of three proven under):

Last Ideas

All of the above shares are buying and selling at remarkably low-cost valuation ranges on account of some enterprise headwinds. A few of them have been harm by excessive inflation or the most recent financial slowdown whereas others are going through their very own particular points. Many of the above shares are more likely to extremely reward buyers off their present depressed ranges. Furthermore, all of the above shares are providing dividend yields above 5%. Thus, they make it a lot simpler for buyers to attend patiently for the enterprise headwinds to subside.

If you’re excited by discovering extra high-quality dividend development shares appropriate for long-term funding, the next Certain Dividend databases shall be helpful:

The foremost home inventory market indices are one other strong useful resource for locating funding concepts. Certain Dividend compiles the next inventory market databases and updates them month-to-month:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].

")