filadendron/E+ through Getty Photos

F-star Therapeutics (NASDAQ:FSTX) is a microcap firm with macrocap goals and a takeover bid at $7.12 per share. The corporate at present trades at $5.86. The hole stays on concern that though the UK govt has authorized the deal, the US CFIUS (the Committee on Overseas Funding in the USA) hasn’t authorized it but. This presents a possibility if the deal closes; for my part, it additionally presents a possibility if the deal doesn’t shut, as a result of the corporate seems to be undervalued. The one threat is money.

With a view to enhance their valuation within the occasion the deal doesn’t shut, this firm must impress upon the market that their pipeline can’t be valued at a mere $100mn. To ensure that them to so impress the market, they should produce convincing information from their belongings. That is my first impression; now let’s dig in.

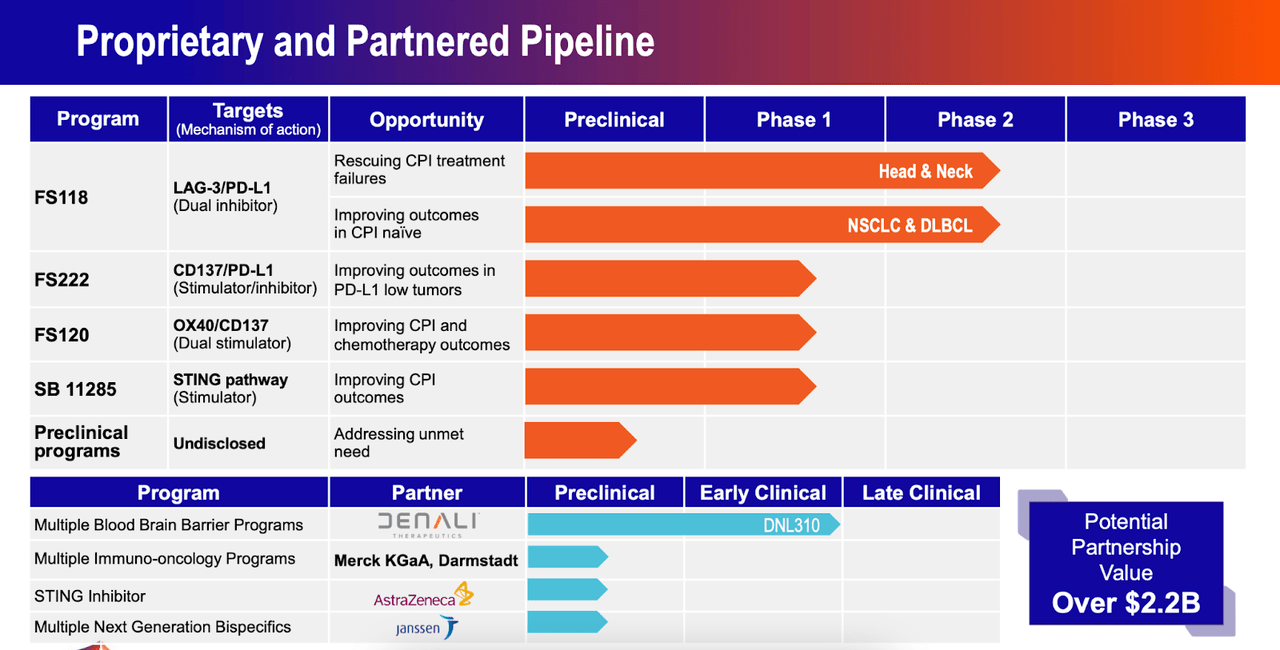

This is a take a look at their pipeline:

FSTX pipeline (FSTX web site)

At first look, that is a powerful pipeline. They’ve 4 scientific stage, self-owned belongings, and what seems to be like 4 separate partnered packages, with large names like Merck KGaA, AstraZeneca, Janssen and Denali. Additionally they state, in large, daring letters, that potential partnership worth is over $2.2bn.

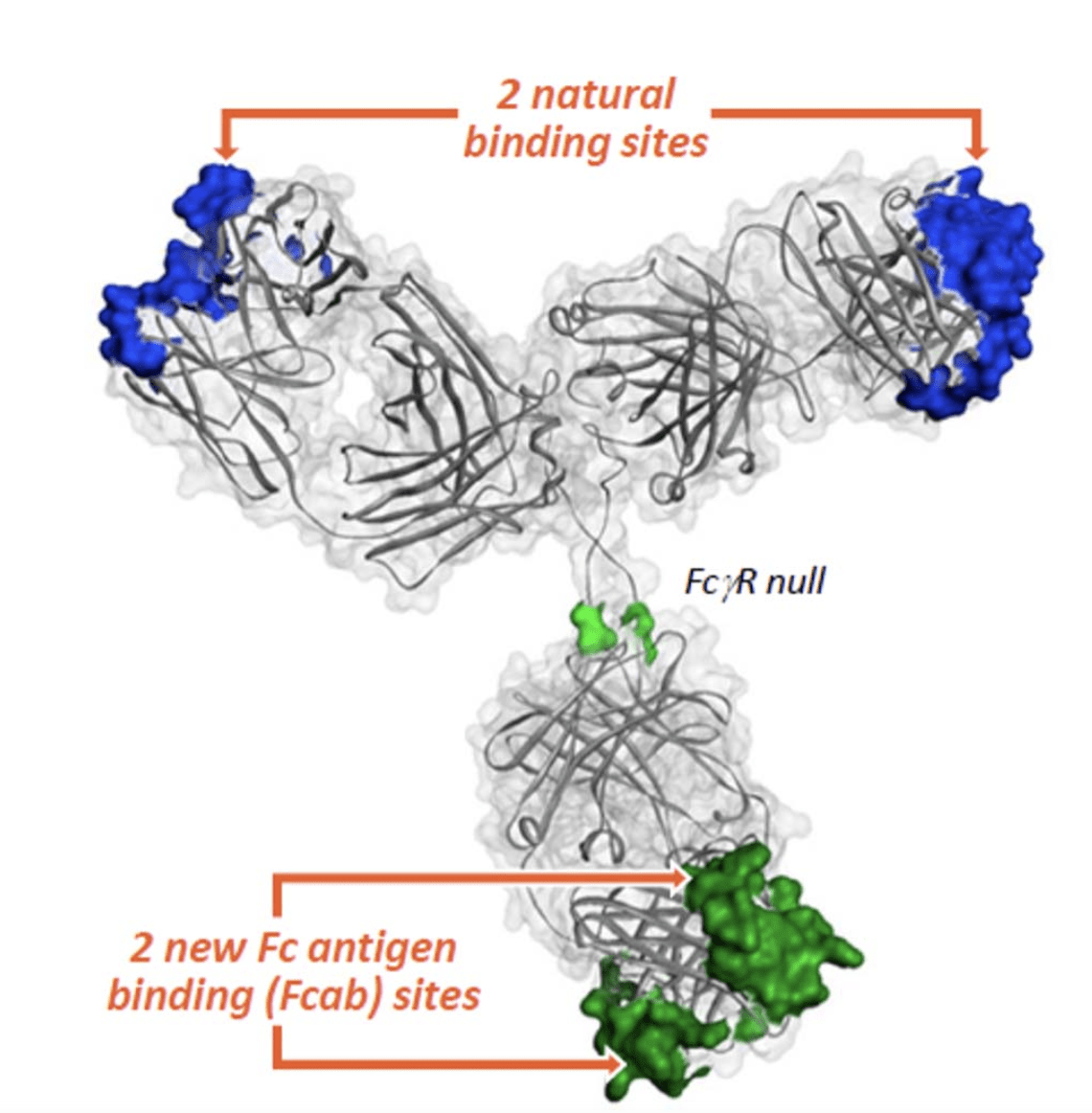

The corporate’s expertise is immunotherapy-focused, utilizing a bispecific antibody platform. These molecules are tetravalent, which the corporate claims will “drive robust twin immune activation capabilities.”

FSTX expertise (FSTX web site)

These monoclonal antibodies now bind to 2 separate and particular goal antigens. As Fierce explains:

F-star’s Modular Antibody Expertise makes bispecific antibodies by introducing a brand new antigen binding web site to the fixed (FC) area of an antibody. This binding web site, dubbed an Fcab (Fc area with antigen binding potential), along with the antibody’s personal binding area, permits it to bind to 2 totally different antigens.

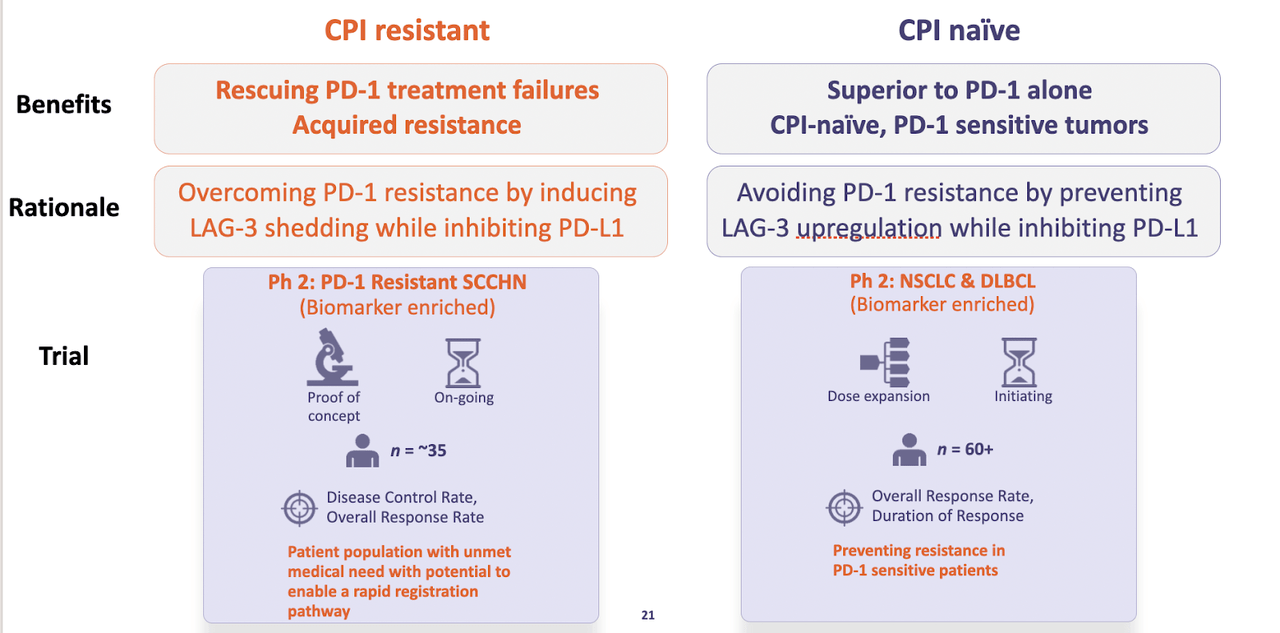

Lead asset FS118 is a twin checkpoint inhibitor concentrating on PD-L1 and LAG-3. Its goal indications are Head & Neck cancers, NSCLC and DLBCL. The second asset, FS120, is a first-in-class OX40/CD137 mAb² twin agonist bispecific antibody. FS122 is a CD137/PD-L1 mAb² bispecific antibody. SB 1125 is a second era STING (Stimulator of Interferon Genes) agonist.

FS118 has gone by way of a part 1 trial in closely pretreated PD-1 resistant sufferers, the place it “was nicely tolerated with no treatment-related critical hostile occasions and no dose-limiting toxicity, as much as 20mg/kg.” In keeping with the info right here (see the January 2022 Presentation), illness management was noticed in sufferers expressing PD-L1 and LAG-3 within the tumor microenvironment. In a affected person with Anaplastic thyroid most cancers, or ATC, with perithyroid metastasis, a number of strains of therapies had been beforehand given. Concurrent chemo and radiation had progressive illness after 5 months. Anti-PD-L1 nivolumab was given, leading to a ten month length of response. A Braf/Mek inhibitor was additionally given together with nivo, which resulted in extreme toxicity with progressive illness after 4 months. Since February 2019, this affected person has been on FS118 dosing (33 months), and “inside a month the affected person had fast enchancment in tumor measurement and was in a position to swallow.” This results in the next improvement plan for FS118:

FS118 Improvement plan (FSTX web site)

It now has a part 2 proof of idea trial ongoing in HNC. The three different belongings have part 1 trials ongoing. Thus, as rising biopharmas go, there’s some semblance of purpose in claiming that the info at hand might not justify the valuation out there. We’ve got seen worse, a lot worse.

One other angle to F-star’s funding case is their in depth patent property. As the corporate says:

Our patent property consists of over 500 granted patents and pending patent functions typically directed to, for instance, compositions and strategies associated to our Fcabs, our modular antibody expertise platform, our lead mAb 2 product improvement candidates, our STING agonist SB 11285 and different STING agonist compounds, and different merchandise, proprietary applied sciences and processes.

For lead asset FS118, they personal or have licensed eight patent households, out of which they personal ” two FS118-focused patent households which relate to the FS118 mAb 2 bispecific antibody composition of matter and the LAG-3 Fcab included in FS118.” Patent time period goes to 2038. FS222 is roofed by 7 patent households, and so they ” personal three patent households which relate to the composition of matter of the CD137 Fcab included in FS222, the PD-L1 antibody included in FS222 (acquired below settlement from Iontas), and the FS222 mAb 2 bispecific antibody.” The patent scenario is comparable for FS220, the place additionally they personal composition of matter patents. This implies, these molecules had been found by them, or they’ve important IP protection as a minimum. Additionally they personal patents overlaying their platform applied sciences, and extra composition of matter patents overlaying their STING compound. I can see what might need attracted large pharma to this firm. If their proof of idea trial works out, we might be seeing much more from these partnerships.

Now let’s discover these partnerships to see what, if something, large pharma sees in FSTX, or are they proforma offers.

Denali (DNLI) first partnered with F-star for his or her F-star Gamma unit in 2016, with an choice to amass this unit, which was exercised in 2016, in a deal “probably value $471 million, choosing up the rights to antibodies developed below their collaboration.” About this collaboration, Denali CEO Ryan Watts, Ph.D., stated:

Our resolution to train the choice to purchase F-star Gamma displays the progress in our collaboration with F-star and the era of preclinical information displaying that our proprietary TV platform expertise might allow us to ship biologics throughout the BBB and into the mind. Particularly, current information demonstrated strong and sustained peripheral and mind exercise for our ETV:IDS program for Hunter Syndrome and therefore preclinical proof of idea. Moreover, the expanded collaboration permits us to deepen and broaden our analysis efforts supporting our TV platform expertise

Denali really had extra time to shut the choice, however they “ramped up” the timeline after seeing one thing they preferred. This was no proforma deal.

The corporate has a small, ~$13mn+royalties cope with Kymab in 2016 for sure of their patents. Kymab was acquired by Sanofi in 2021.

In 2019, the corporate entered right into a licensing settlement “to develop, manufacture and commercialize two separate mAb 2 antibody merchandise that every comprise a particular Fcab and a Fab goal pair (every a licensed product)” with Ares, a subsidiary of Merck KGaA (OTCPK:MKGAF) of Dermstadt, Germany. The deal is probably value some $750mn. Final yr, Merck exercised its fourth program choice as a part of the deal, and produced information from a partnered compound at SITC.

F-star had an settlement with AstraZeneca (AZN) in 2021 whereby they granted international rights to their STING compound to AZN. The deal was value a small $12mn upfront cost, $300mn in milestone funds, and single digit royalties.

In the identical yr, the corporate acquired into one other settlement with Janssen (JNJ) and gave them a “worldwide unique license to analysis, develop and the choice to commercialize as much as 5 novel bispecific antibodies directed to Janssen therapeutic targets utilizing our proprietary Fcab and mAb2 platforms.” The deal concerned $17.5mn in upfront funds, $1.35bn in milestones, and mid single digit royalties.

Thus, these are usually not proforma offers in any respect. These are critical offers, and as is common with early stage however promising corporations with out POC, the upfront funds are small, however the milestone funds are massive. A few of these corporations have even paid improvement prices for the compounds they acquired rights to, on a retrospective foundation. This isn’t one thing I’ve come throughout usually. This, once more, goes to indicate that the POC trial of FS118 carries lots of weight, and given the early information we’ve seen, the corporate seems to be undervalued.

Right here, I’m going to desert normal apply and never talk about market potential of the focused indications as a result of at this stage of improvement, there’s not sufficient choice for many goal indications. Three issues appear necessary right here – early information, which they’ve; patents, which additionally they have; and these probably main offers with large pharma. This firm should be valued on these bases, and I do not assume their present valuation justifies their potential.

The takeover bid

F-star was supplied a takeover bid by invoX Pharma – wholly owned by Sino Biopharmaceutical (OTCPK:SBMFF) (OTCPK:SBHMY), in June 2022, for $7.12 per share in an all-cash transaction. A November article on Looking for Alpha discusses the small print right here. Since November, although, CFIUS has nonetheless delayed the method. Sino Biopharma is a $11.4bn market cap , OTC traded main Chinese language agency. The writer I cited says that the explanation for the delay might be “overseas entry to delicate U.S. affected person information, continued U.S. entry to the corporate’s R&D output, or one thing else.” The writer speculates that presence of Chinese language authorities components on Sino’s board could also be a deterrent for CFIUS, whereas the origin and management of the corporate in Thailand could also be a mitigant.

In late December, the CFIUS issued an interim order blocking the deliberate sale. Additionally they threatened “to take motion if the businesses shut the deal with out resolving excellent nationwide safety dangers.” FSTX dropped 40%, after which went again up 40% the subsequent day after the 2 corporations introduced that they determined to increase their settlement deadline to January 31, 2023 from Jan 17.

One other necessary assertion from the Dec 30 8-Okay:

CFIUS has confirmed to the Events that it has decided that mitigation measures could be out there and in discussions with the Events indicated a draft Nationwide Safety Settlement setting forth such mitigation measure could be despatched to the Events.

With regard to additional extensions and F-star’s want for money, here is what Sino Bio stated:

“We’re in search of to maneuver swiftly to make sure F-star has the financing it wants to take care of probably lifesaving work on most cancers scientific trials, whereas avoiding in depth layoffs,” invoX stated in a press release. “By means of our engagement with CFIUS workers, we perceive that the Committee has decided that any nationwide safety considerations could be mitigated and can work expeditiously to succeed in a decision.”

This will likely really imply that if there are additional extensions however with a constructive tone from CFIUS, Sino Bio might lengthen that $12mn FSTX was purported to obtain if the acquirer walked away as a result of CFIUS delays.

Financials

FSTX has a market cap of $128mn and a money steadiness of $35mn. Final quarter, they spent round $10mn in R&D and $5mn in G&A, and final yr they spent some $40mn. So the money runway is brief, which is one purpose why the acquisition bid seems to be like a godsend, and its denial seems to be like a despairing occasion. Nevertheless, as I’ve tried to argue, the deal might look good within the quick time period, however in the long run, it could really be devaluing FSTX.

Backside line

In lower than every week, we are going to most likely know whether or not the 2 corporations will lengthen the settlement additional. It appears seemingly that they may, given the CFIUS lifeline of mitigation measures and a draft Nationwide Safety Settlement setting forth such mitigation measure. That the UK has agreed to the merger – the UK broadly follows US authorities traits, politically talking – can also be indicative of a course of which may be drawn out, however may finish positively. If it does, the inventory will go up some 30%.

If it does not, the inventory will fall drastically. Nevertheless, there is a backup plan at work right here within the in depth patent property and the probability of constructive FS118 information if the corporate survives. This presents a dangerous alternative.

Editor’s Notice: This text discusses a number of securities that don’t commerce on a significant U.S. change. Please pay attention to the dangers related to these shares.

")