V-Guard Industries Restricted’s acquisition of main kitchen home equipment model Sunflame Enterprises Non-public Ltd (SEPL) augurs properly for the corporate. Brokerage agency Sharekhan sees a 23 per cent upside or Rs 60 per share acquire. The inventory was advisable at a worth of Rs 261.

V-Guard shares right now ended at Rs 271 on the NSE and had been down 0.55 per cent from the earlier closing worth.

V-Guard acquired 100 per cent stake in Haryana based mostly SEPL for a consideration of Rs 660 crore on a cash-free and debt-free foundation. The transaction is predicted to shut by mid-January 2023.

Sunflame’s acquisition is according to firm’s technique to turn into a major participant within the home kitchen home equipment business which at the moment types simply 4-5 per cent of its whole income, Sharekhan mentioned in a report.

V-Guard will seemingly profit from Sunflame’s model which has a pan-India presence with a robust model recall, it mentioned. It may assist in unlocking synergy advantages in areas like geography, product portfolio and channels since Sunflame has sturdy presence in north and west, whereas V-Guard is predominantly current within the south market, the brokerage agency mentioned additional.

“Its vast portfolio, product improvement capabilities and the just lately established state of-the-art built-in manufacturing facility would assist V-Guard scale up its kitchen home equipment enterprise,” Sharekhan mentioned in a report.

In the long term, a significant contribution from this acquisition would assist develop the bottom-line, it mentioned.

“We count on Income/PAT CAGR of 19/23 per cent over FY2022-FY2025E EPS (not factoring in Sunflame acquisition). We retain a Purchase on V-Guard with a revised worth goal (PT) of Rs. 320, rolling ahead our estimates to September FY2024E EPS,” the brokerage added.

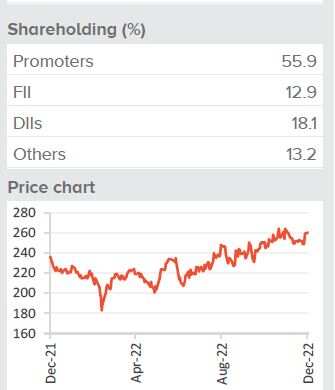

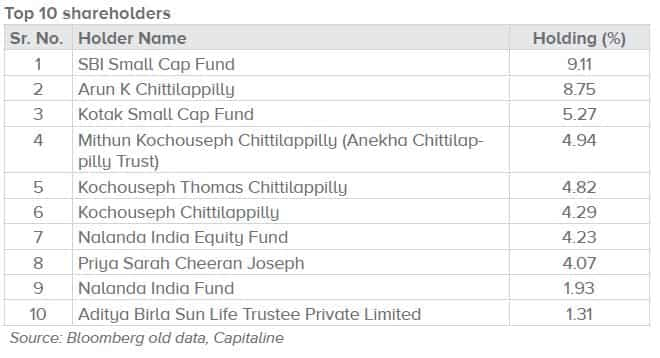

V-Guard Fundamentals

The corporate had carried out persistently properly with regular money flows and robust working margin of 12-13 per cent, this brokerage mentioned.

The acquisition in all fairness priced at Enterprise Worth/gross sales of 1.9X.

Caveats

Though income progress will seemingly be incremental, the acquisition possibly earnings impartial, and even marginally dilutive for FY24E as a consequence of rise in curiosity value and decline in different earnings as a consequence of decrease money.

Comparatively weak demand atmosphere in a few of the product classes coupled with intense competitors in a few of its enterprise segments is a key concern, the brokerage agency mentioned.

Technical View

The inventory has outperformed Nifty50 by over 12 per cent, giving returns of 21 per cent towards 9.5 per cent returned by the latter over a 1-year interval, in accordance to an information sourced from Trendlyne. Momentum indicators RSI and MFI are at 65.4 and 63.3. A quantity under 30 signifies that the inventory is in oversold territory whereas quantity above 70 means that the inventory is in oversold scenario.

All 16 shifting averages mirror a bullish development.

Technical Analyst Nilesh Jain recommends a purchase on decline on this inventory. The inventory is buying and selling close to an necessary breakout zone and if a degree of Rs 280 is breached, an additional upside of Rs 320 will open, Jain mentioned.

The chart construction is optimistic, and regardless of Wednesday’s market crash, the declines on this inventory had been restricted, he additional added.

Jain, who’s Assistant Vice President – Lead By-product and Technical Analysis at Centrum Broking, recommends a cease lack of Rs 320.

Additionally Learn: Cementing your portfolio: Sharekhan sees Rs 1300 per share good points in UltraTech Cement; lists 4 triggers with this CAVEAT

(Disclaimer: The views/options/advises expressed right here on this article is solely by funding specialists. Zee Enterprise suggests its readers to seek the advice of with their funding advisers earlier than making any monetary determination.)

Q3 2024 Earnings Name Transcript")

.png#keepProtocol "Permitting Consumers to Self-Educate within the Ecommerce Period")

bullish market over?")