Darren415

This text was first launched to Systematic Earnings subscribers and free trials on Oct. 31.

Welcome to a different installment of our Preferreds Market Weekly Evaluation, the place we focus on most popular inventory and child bond market exercise from each the bottom-up, highlighting particular person information and occasions, in addition to top-down, offering an outline of the broader market. We additionally attempt to add some historic context in addition to related themes that look to be driving markets or that buyers should be aware of. This replace covers the interval via the final week of October.

Be sure you take a look at our different weekly updates masking the enterprise improvement firm (“BDC”) in addition to the closed-end fund (“CEF”) markets for views throughout the broader earnings house.

Market Motion

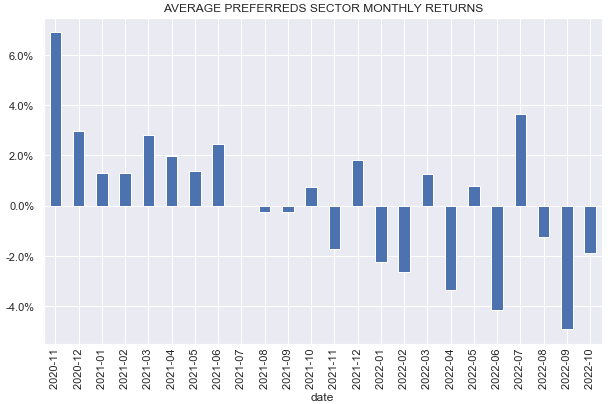

Preferreds had a great week with all sub-sectors seeing constructive returns. Over October, nonetheless, most sectors completed decrease.

Systematic Earnings

In contrast to CEFs and BDCs, preferreds delivered a damaging return in October – the third damaging month-to-month return in a row.

Systematic Earnings

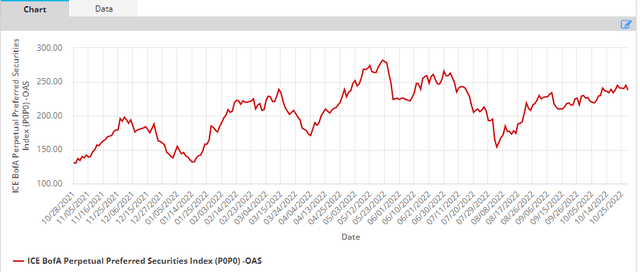

In distinction to BB-rated company bonds, as an example, whose credit score spreads have rallied by 0.7% from 3.76% in October, preferreds credit score spreads have truly widened in October as the next chart reveals. Total, preferreds supply good worth in the intervening time, notably within the institutional sector which boasts a decrease period.

ICE

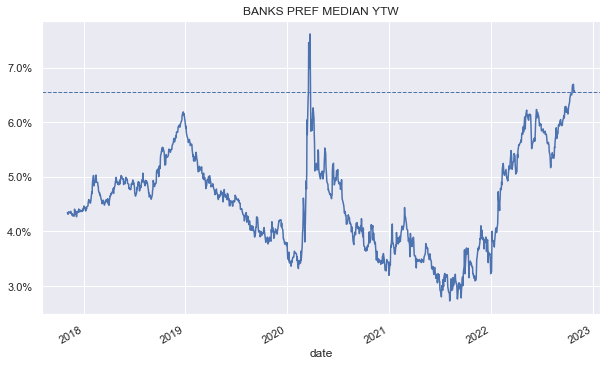

Financial institution preferreds, as an example, lots of that are or are near investment-grade, boast yields near 7%.

Systematic Earnings

Market Commentary

Company mREITs have kicked off Q3 earnings within the sector.

AGNC (AGNC) e book worth fell round 20% – the very best tempo within the post-COVID interval and nearly as massive because the 23% drop in Q1-2020. AGNC issued $289m value of widespread through the quarter in addition to $150m of the brand new AGNCL. Internet-net, this, along with the e book worth drop, has prompted fairness protection to fall from 5.2x to 4.3x – a far cry from a double-digit stage in 2019.

AGNC Sequence C (AGNCN) is at the moment callable and it does make sense for AGNC to redeem it for two causes. One, the newly issued AGNC Sequence L has a a lot decrease coupon proper now than AGNCN and the drop within the firm’s stockholders’ fairness has elevated the load of preferreds within the capital construction, rising the entire financing value of the corporate (since preferreds curiosity expense is above the price of repo).

It’s completely attainable that the corporate is preserving AGNCN alive to maximise their publicity to Companies which, at present valuations, makes numerous sense. It additionally jibes with the truth that leverage has truly elevated (to eight.7x) and the MBS foundation sensitivity of e book worth rose to a 3-year excessive determine of 19% (i.e. 19% drop in e book worth for a 25bp rise in Company spreads). When/if the Company foundation begins to revert, AGNCN may truly be redeemed and the corporate will then additionally decrease its leverage.

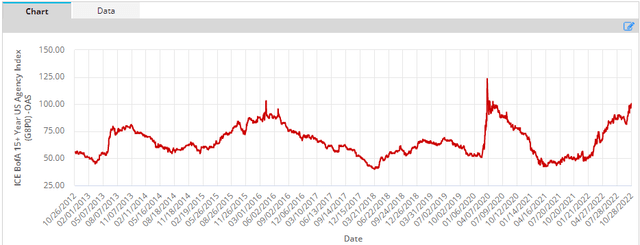

Extra broadly, what’s fascinating is that Company valuations are rather more excessive than the valuations of different fixed-income sectors – they’re buying and selling at their peak this yr and never far off their COVID peaks.

ICE

If valuations transfer to their peak GFC ranges, we’d count on a 40-50% e book worth drop for AGNC (leading to fairness protection of round 2x), though it is onerous to think about it getting there (and the Fed not doing something). Based mostly on this, it could possibly make sense to chubby Company mREIT preferreds relative to different credit score belongings. As an illustration, high-yield company credit score spreads are greater than 1% beneath their 2022 peak, about half their COVID peak ranges and 1 / 4 of their peak GFC ranges.

Dynex Capital (DX) noticed fairly comparable outcomes. It tends to run a lower-leverage portfolio so its e book worth fell a extra modest 16%. Leverage elevated sharply nonetheless to eight.5x from 6.6x. DX tends to be rather more nimble with leverage than different mREITs so this leap means they’re seeing good worth in Companies. Like AGNC and Annaly Capital (NLY), DX additionally issued widespread shares. Fairness/preferreds protection fell to five.9x.

Annaly additionally declared outcomes. Ebook worth fell round 15% whereas leverage fell as properly. A really compelling side of NLY is the convexity in its conduct. Particularly, this has to do with the way it responds to massive e book worth drops. In Q3, the corporate issued 16% extra widespread shares. The web result’s that whereas e book worth fell 15%, fairness, which is the factor that really issues to preferreds, fell only one.2%. Because the e book worth has been falling this yr, the corporate grew its widespread shares by an enormous 29%.

AGNC and DX have additionally issued new widespread shares however not almost in as massive quantities. In different phrases, a big e book worth drop causes NLY to situation widespread shares, softening the affect on preferreds. And if we see an enormous rise in e book worth, NLY will doubtless do nothing (i.e. they will not purchase again 29% of their shares), leaving preferreds a lot better off from an natural rise in fairness.

This convexity of little fairness protection loss to the draw back and an enormous potential fairness protection acquire to the upside is a pleasant profile for preferreds to have. On this sense, NLY preferreds supply a lot greater convexity than its counterparts within the sector. There isn’t a assure NLY will hold being so daring with widespread fairness issuance to the draw back however the truth is that they have been to this point, leaving their preferreds a lot better off than others within the sector.

The opposite factor value highlighting is that NLY tends to be considerably extra conservative. For instance, whereas DX and AGNC elevated their leverage ranges in Q3 (to eight.5x and eight.7x), NLY truly moved it decrease considerably from 6.6x to five.8x.

The next stage of leverage is extra enticing for buyers in widespread shares who’re bullish Companies. Nevertheless, preferreds holders are rather more occupied with draw back threat than upside features so, all else equal, they like decrease leverage ranges.

Let’s take a look at what yields are on supply inside the sector.

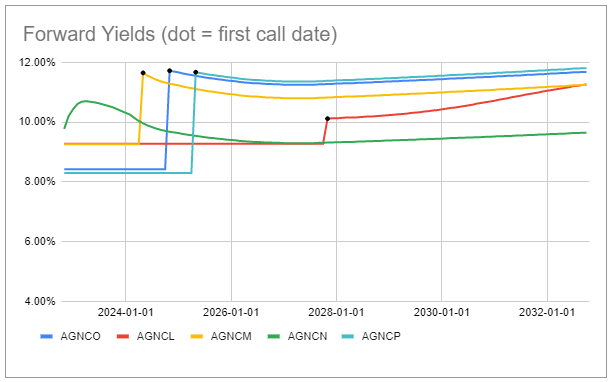

The chart beneath reveals ahead yields of the AGNC suite. There isn’t a slam dunk “greatest” inventory right here. Shares with greater yields within the close to time period like AGNCN and AGNCM are anticipated to have decrease yields in the long term and vice-versa. On this sense, the pricing is fairly environment friendly. Total, we see worth in AGNCN within the close to time period and AGNCL within the longer-term.

Systematic Earnings Preferreds Software

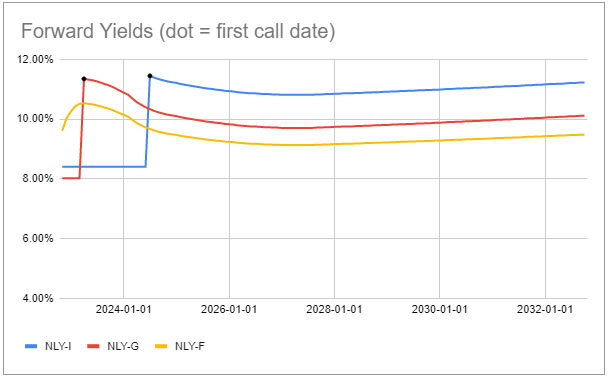

Within the NLY suite we like NLY.PF and NLY.PG.

Systematic Earnings Preferreds Software

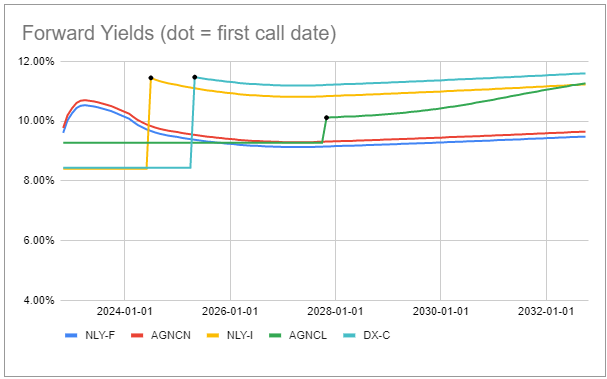

If we mix the shortest name and longest name AGNC and NLY preferreds with DX.PC, we get the next image. Over the longer-term, DX.PC gives numerous worth in our view, nonetheless, Apr-2025 is a long-time to attend for a bump within the coupon and by then Libor may simply be considerably decrease than it’s in the present day or what’s priced into Libor forwards.

Systematic Earnings Preferreds Software

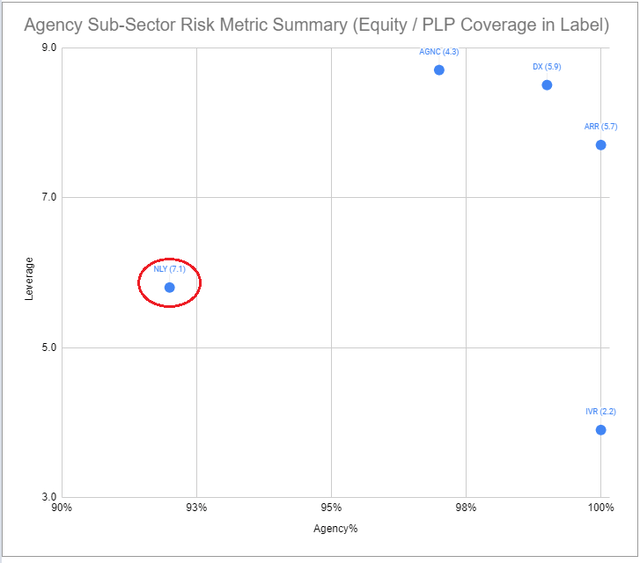

In elementary phrases, we proceed to favor NLY within the sector – it has the very best fairness/most popular protection within the Company mREIT preferreds sub-sector and the bottom leverage. As talked about above, it has additionally been most aggressive in issuing widespread shares, boosting fairness most popular protection.

Systematic Earnings Preferreds Software

")

Q3 2024 Earnings Name Transcript")