Up to date on September twelfth, 2022 by Bob Ciura

Buyers seeking to generate larger ranges of revenue from their funding portfolios ought to check out Actual Property Funding Trusts, or REITs. These are corporations that personal actual property properties and lease them to tenants or spend money on actual property backed loans, each of which generate a gradual stream of revenue.

The majority of their revenue is then handed on to shareholders, via dividends. You possibly can see all 208 REITs right here.

You possibly can obtain our full record of REITs, together with vital metrics resembling dividend yields and market capitalizations, by clicking on the hyperlink under:

The great thing about REITs, for revenue traders, is that they’re required to distribute 90% of their taxable revenue to shareholders yearly, within the type of dividends. In return, REITs sometimes don’t pay company taxes.

Consequently, most of the 200+ REITs we observe provide excessive dividend yields of 5%+.

However not all high-yielding shares are computerized buys. Buyers ought to fastidiously assess the basics to make sure the excessive yields are sustainable.

Notice that whereas the securities on this article have very excessive yields, a excessive yield alone doesn’t make for a stable funding. Dividend security, valuation, administration, steadiness sheet well being, and progress are all crucial elements as effectively.

We urge traders to make use of the under evaluation as informative, however to do vital due diligence earlier than shopping for into any safety – and particularly excessive yield securities. Many (however not all) excessive yield securities have vital threat of a dividend discount and/or deteriorating enterprise outcomes.

Desk of Contents

You possibly can immediately soar to any particular part of the article by utilizing the hyperlinks under:

Excessive-Yield REIT No. 10: Ellington Residential Mortgage REIT (EARN)

Ellington Residential Mortgage REIT acquires, invests in, and manages residential mortgage and actual property associated belongings. Ellington focuses totally on residential mortgage-backed securities, particularly these backed by a U.S. Authorities company or U.S. authorities–sponsored enterprise. Company MBS are created and backed by authorities companies or enterprises, whereas non-agency MBS are not assured by the federal government.

Supply: Investor Presentation

On August 4th, 2022, Ellington introduced a month-to-month dividend of $0.08 per share to be paid on September twenty sixth, 2022. This $0.08 month-to-month dividend is a 20% lower in comparison with the $0.10 paid month-to-month from October 2021 to Could 2022.

On August tenth, 2022, Ellington Residential reported its Q2 outcomes for the interval ending June thirtieth, 2022. The corporate booked an $(0.82) internet loss per share for Q2. The corporate renamed what was beforehand known as core earnings to adjusted distributable earnings beginning on this quarter.

Ellington achieved adjusted distributable earnings of $3.7 million this quarter, resulting in core EPS of $0.28 per share, which simply covers the dividend paid within the interval. EARN achieved a internet curiosity margin of 1.66% in Q2.

At quarter finish, Ellington had $37.5 of money and money equivalents, and $3.4 million of different unencumbered belongings. The debt-to-equity ratio was 8.0.

Click on right here to obtain our most up-to-date Positive Evaluation report on EARN (preview of web page 1 of three proven under):

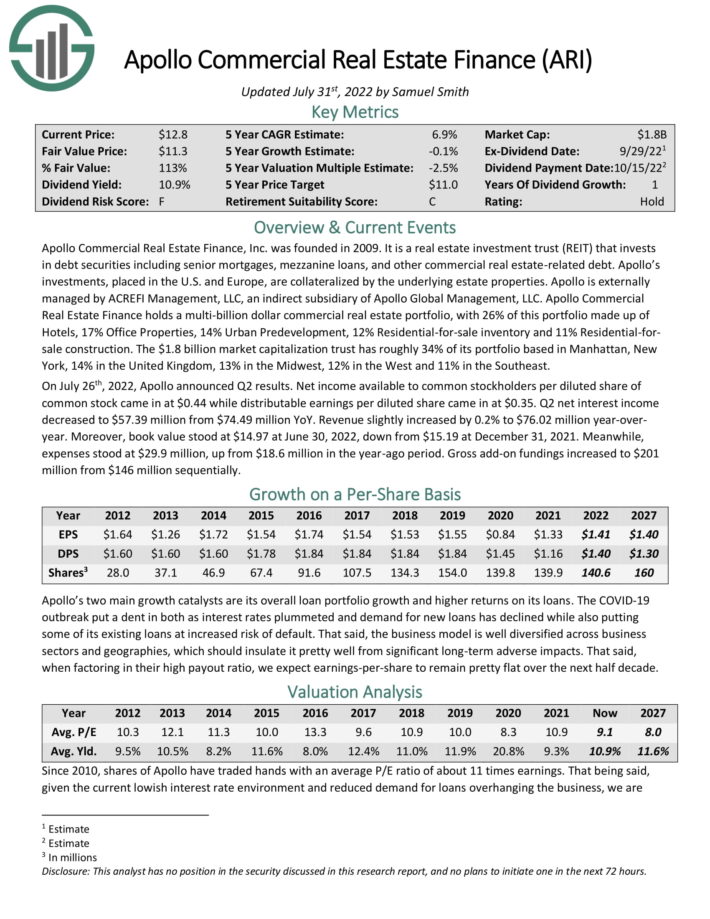

Excessive-Yield REIT No. 9: Apollo Business Actual Property Finance (ARI)

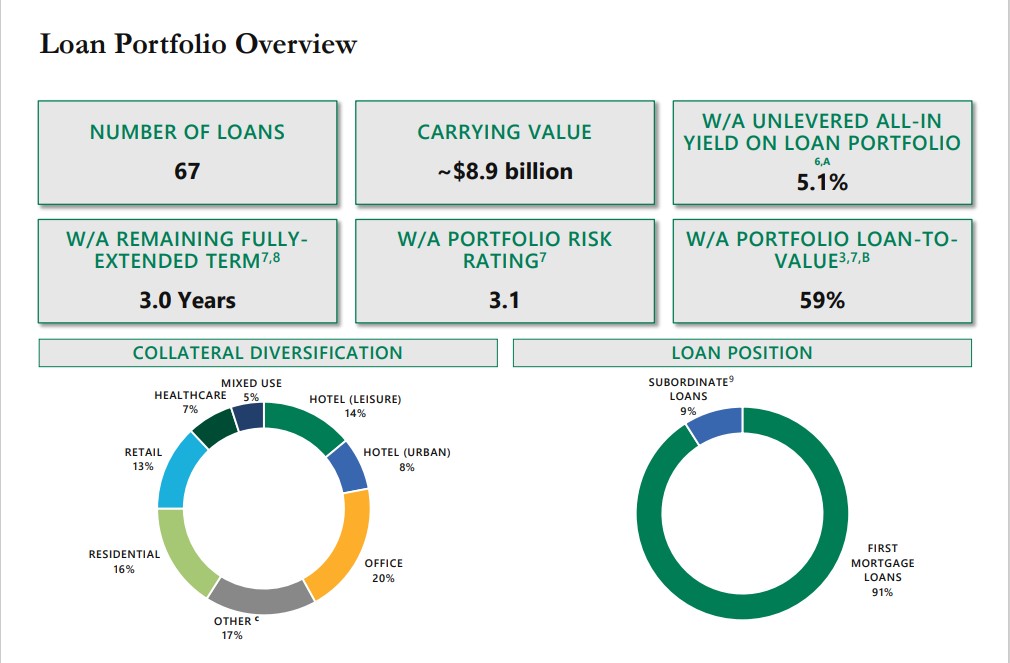

Apollo Business Actual Property Finance invests in debt securities together with senior mortgages, mezzanine loans, and different industrial actual estate-related debt. Apollo’s investments, positioned within the U.S. and Europe, are collateralized by the underlying property properties. Apollo is externally managed by ACREFI Administration, LLC, an oblique subsidiary of Apollo World Administration, LLC.

The belief has roughly 34% of its portfolio primarily based in Manhattan, New York, 14% in the UK, 13% within the Midwest, 12% within the West and 11% within the Southeast.

Supply: Investor Presentation

On July twenty sixth, 2022, Apollo introduced Q2 outcomes. Internet revenue accessible to widespread stockholders per diluted share ofcommon inventory got here in at $0.44 whereas distributable earnings per diluted share got here in at $0.35. Q2 internet curiosity revenue decreased to $57.39 million from $74.49 million YoY.

Income barely elevated by 0.2% to $76.02 million year-overyear. Furthermore, guide worth stood at $14.97 at June 30, 2022, down from $15.19 at December 31, 2021. In the meantime, bills stood at $29.9 million, up from $18.6 million within the year-ago interval. Gross add-on fundings elevated to $201 million from $146 million sequentially.

Click on right here to obtain our most up-to-date Positive Evaluation report on ARI (preview of web page 1 of three proven under):

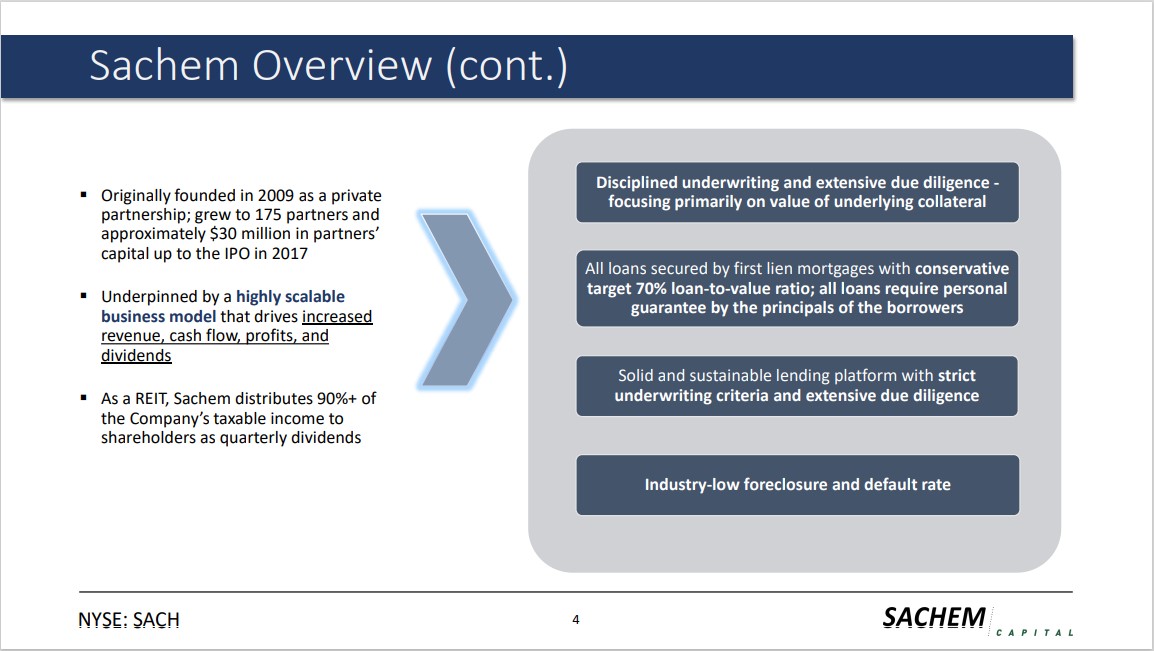

Excessive-Yield REIT No. 8: Sachem Capital Corp. (SACH)

Sachem Capital makes a speciality of originating, underwriting, funding, servicing, and managing a portfolio of short-term (i.e., three years or much less) loans secured by first mortgage liens on actual property positioned primarily in Connecticut. Every of Sachem’s loans is personally assured by the principal(s) of the borrower, which is often collaterally secured by a pledge of the guarantor’s curiosity within the borrower. The corporate generates round $30 million in complete revenues.

Supply: Investor Presentation

On July eleventh, 2022, Sachem Capital raised its dividend by 16.7% to a quarterly charge of $0.14.

On August 4th, 2022, Sachem Capital Corp. introduced its Q2-2022 outcomes for the interval ending June thirtieth, 2022. Whole revenues throughout the quarter got here in at $12.5 million, up 86.9% in comparison with Q2-2021. The rise in income was primarily pushed by a rise in lending operations, together with larger curiosity revenue and origination charges as a result of firm increasing its funding portfolio over the previous 4 quarters.

Internet revenue was roughly $4.3 million, 72% larger in comparison with final yr. Nevertheless, EPS grew by two cents throughout the identical interval to $0.12 because of a better share depend to ensure that Sachem to fund its new originations. We now forecast FY2022 NII/share2 of $0.56.

Click on right here to obtain our most up-to-date Positive Evaluation report on SACH (preview of web page 1 of three proven under):

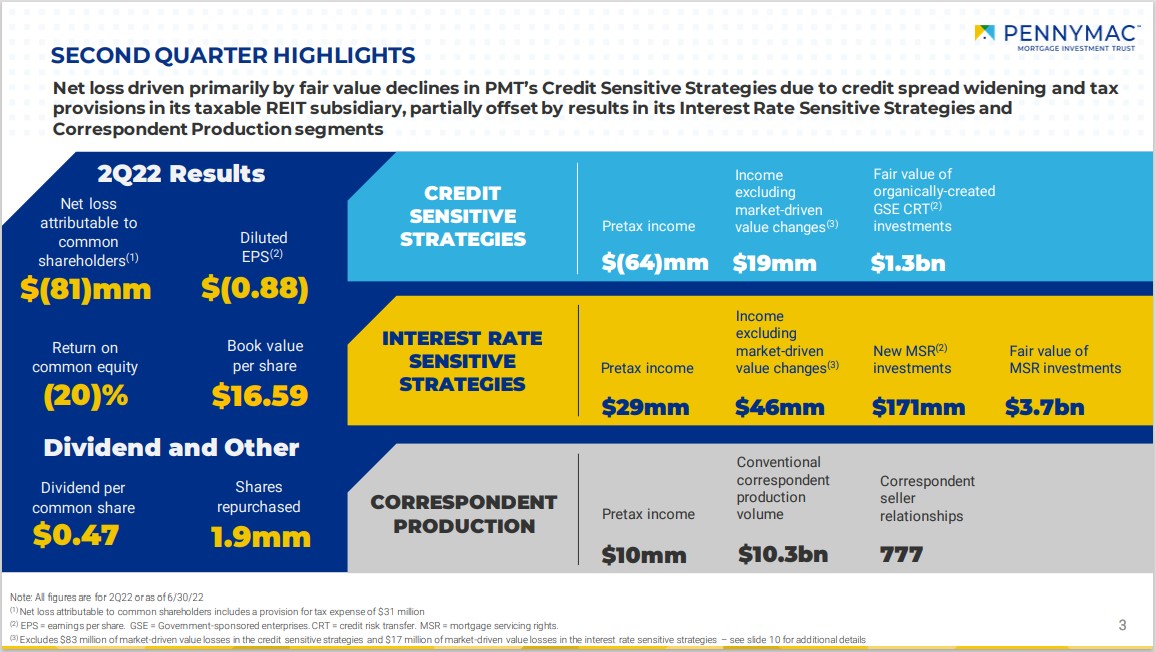

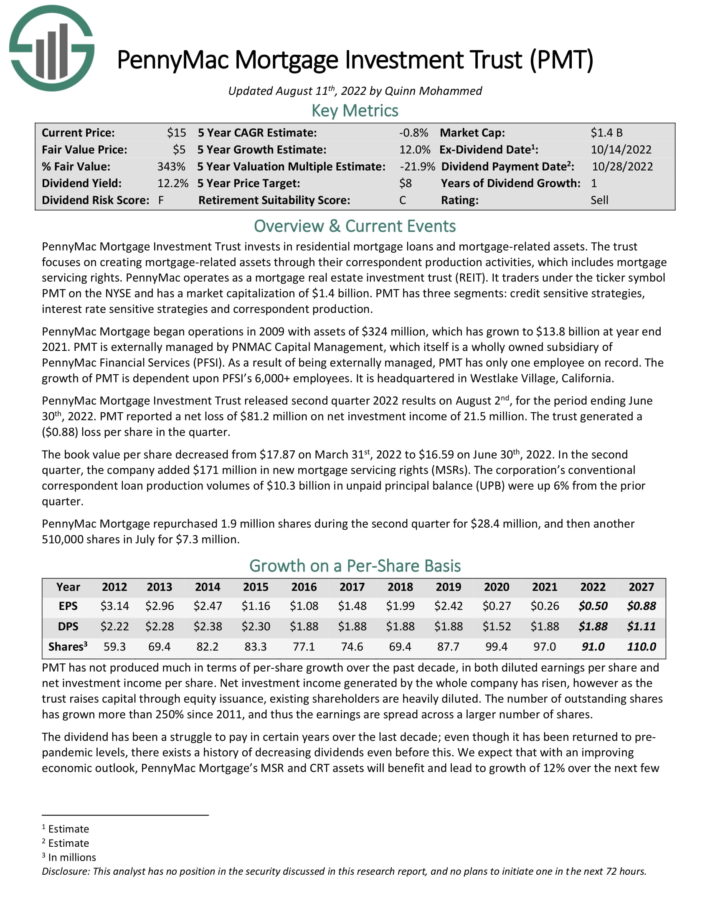

Excessive-Yield REIT No. 7: PennyMac Mortgage Funding Belief (PMT)

PennyMac Mortgage Funding Belief is a specialty REIT that invests in residential mortgage loans and mortgage-related belongings. PMT is managed by PNMAC Capital Administration, LLC, a subsidiary of PennyMac Monetary Providers, Inc. (PFSI).

Supply: Investor Presentation

PMT believes it would generate long-term progress alongside a big (and rising) addressable market in its core business.

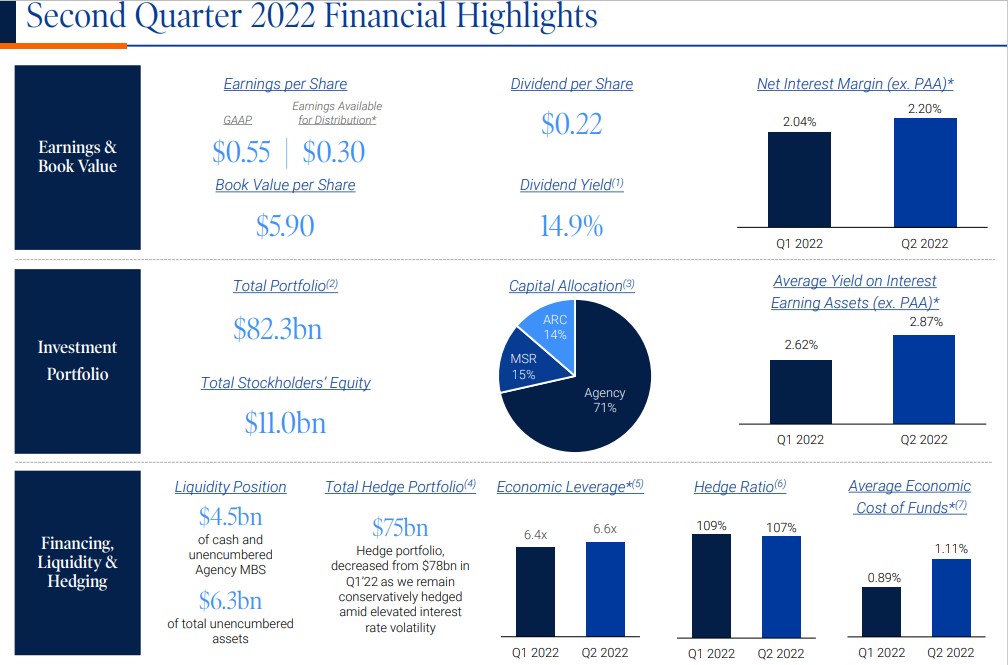

PennyMac Mortgage Funding Belief launched second quarter 2022 outcomes on August 2nd, for the interval ending June thirtieth, 2022. PMT reported a internet lack of $81.2 million on internet funding revenue of 21.5 million. The belief generated a ($0.88) loss per share within the quarter.

The guide worth per share decreased from $17.87 on March thirty first, 2022 to $16.59 on June thirtieth, 2022. Within the second quarter, the corporate added $171 million in new mortgage servicing rights (MSRs). The company’s typical correspondent mortgage manufacturing volumes of $10.3 billion in unpaid principal steadiness (UPB) have been up 6% from the prior quarter.

PennyMac Mortgage repurchased 1.9 million shares throughout the second quarter for $28.4 million, after which one other 510,000 shares in July for $7.3 million.

Click on right here to obtain our most up-to-date Positive Evaluation report on PMT (preview of web page 1 of three proven under):

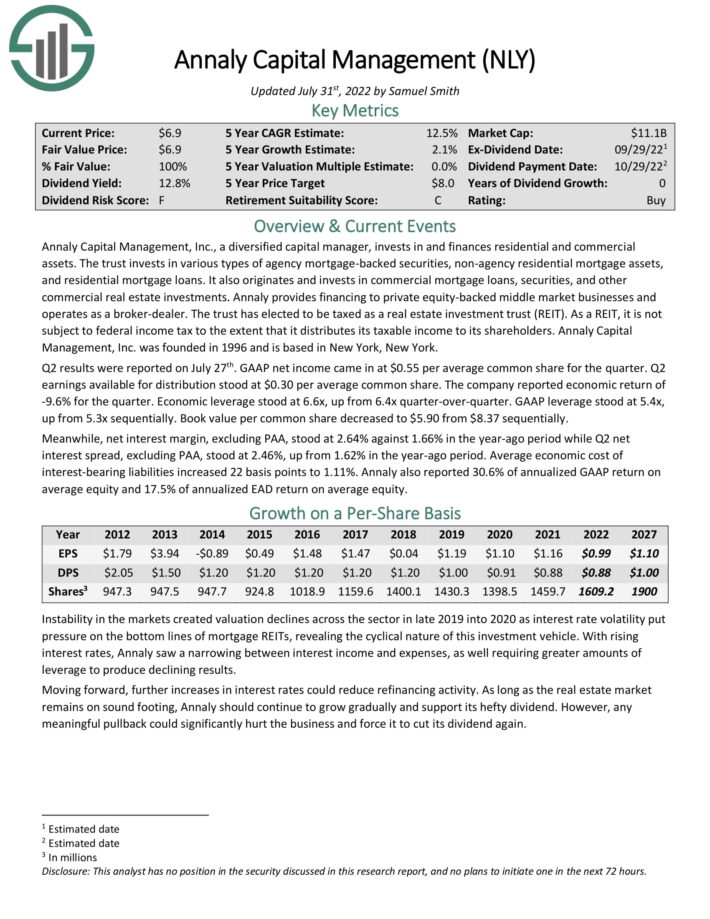

Excessive-Yield REIT No. 6: Annally Capital Administration (NLY)

Annaly Capital Administration, Inc., a diversified capital supervisor, invests in and funds residential and industrial belongings. The belief invests in varied kinds of company mortgage–backed securities, non–company residential mortgage belongings, and residential mortgage loans.

It additionally originates and invests in industrial mortgage loans, securities, and different industrial actual property investments. Annaly provides financing to non-public fairness–backed center market businesses and operates as a dealer–vendor.

Supply: Investor Presentation

Q2 outcomes have been reported on July twenty seventh. GAAP internet revenue got here in at $0.55 per common widespread share for the quarter. Q2 earnings accessible for distribution stood at $0.30 per common widespread share. The corporate reported financial return of -9.6% for the quarter. Financial leverage stood at 6.6x, up from 6.4x quarter-over-quarter. GAAP leverage stood at 5.4x, up from 5.3x sequentially. E book worth per widespread share decreased to $5.90 from $8.37 sequentially.

In the meantime, internet curiosity margin, excluding PAA, stood at 2.64% towards 1.66% within the year-ago interval whereas Q2 internet curiosity unfold, excluding PAA, stood at 2.46%, up from 1.62% within the year-ago interval. Common financial price of interest-bearing liabilities elevated 22 foundation factors to 1.11%. Annaly additionally reported 30.6% of annualized GAAP return on common fairness and 17.5% of annualized EAD return on common fairness.

Click on right here to obtain our most up-to-date Positive Evaluation report on NLY (preview of web page 1 of three proven under):

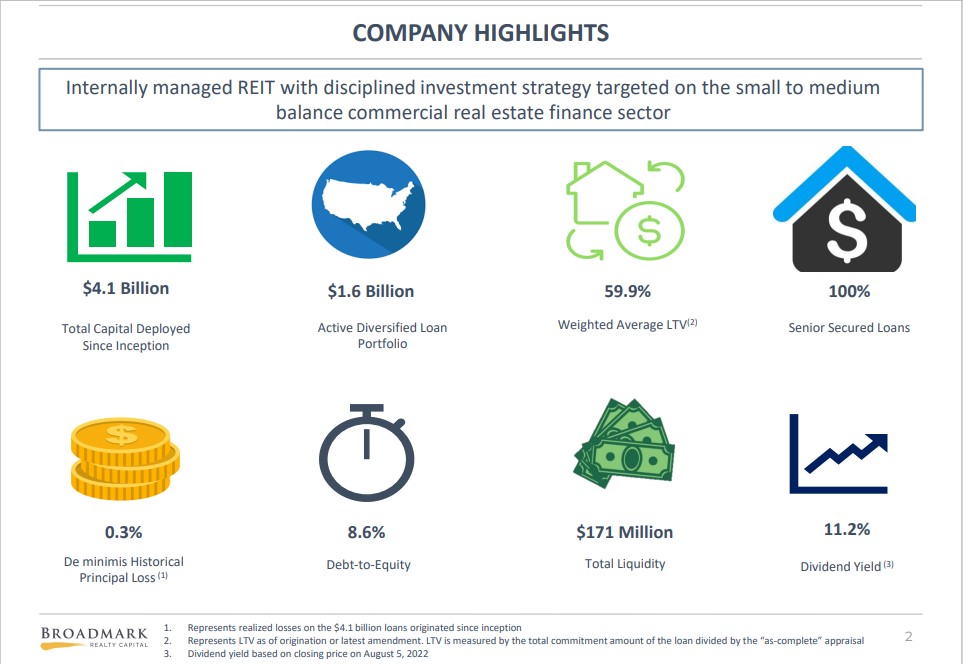

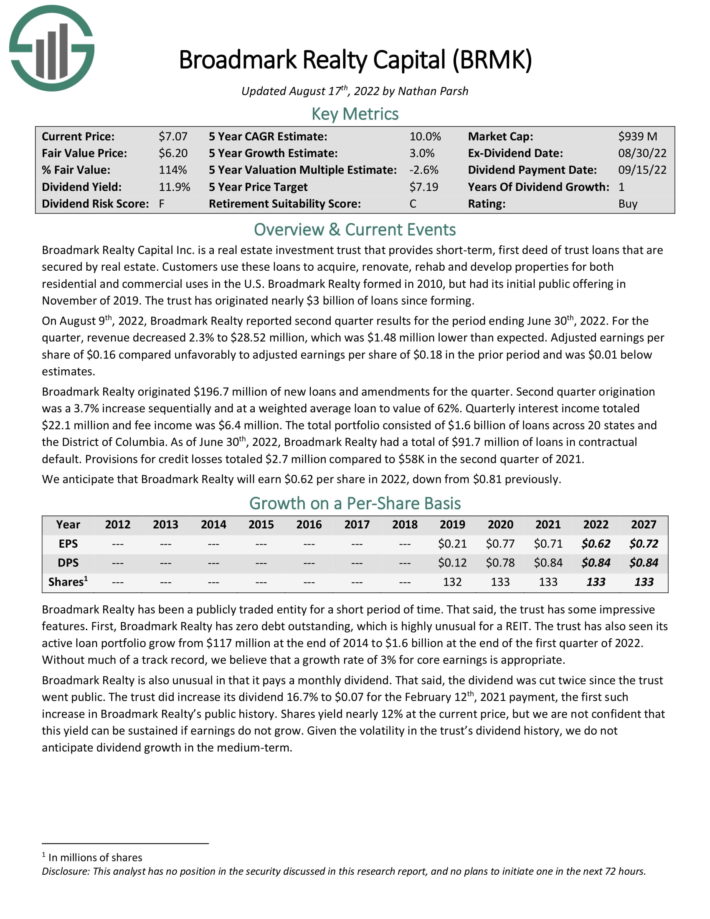

Excessive-Yield REIT No. 5: Broadmark Realty Capital (BRMK)

Broadmark Realty Capital Inc. is an actual property funding belief that gives short-term, first deed of belief loans which can be secured by actual property. Clients use these loans to amass, renovate, rehab and develop properties for each residential and industrial makes use of within the U.S. Broadmark Realty fashioned in 2010, however had its preliminary public providing in November 2019.

Supply: Investor Presentation

On August ninth, 2022, Broadmark Realty reported second quarter outcomes for the interval ending June thirtieth, 2022. For the quarter, income decreased 2.3% to $28.52 million, which was $1.48 million decrease than anticipated. Adjusted earnings per share of $0.16 in contrast unfavorably to adjusted earnings per share of $0.18 within the prior interval and was $0.01 under estimates.

Broadmark Realty originated $196.7 million of recent loans and amendments for the quarter. Second quarter origination was a 3.7% improve sequentially and at a weighted common mortgage to worth of 62%. Quarterly curiosity revenue totaled $22.1 million and price revenue was $6.4 million. The whole portfolio consisted of $1.6 billion of loans throughout 20 states and the District of Columbia.

As of June thirtieth, 2022, Broadmark Realty had a complete of $91.7 million of loans in contractual default. Provisions for credit score losses totaled $2.7 million in comparison with $58K within the second quarter of 2021.

Click on right here to obtain our most up-to-date Positive Evaluation report on BRMK (preview of web page 1 of three proven under):

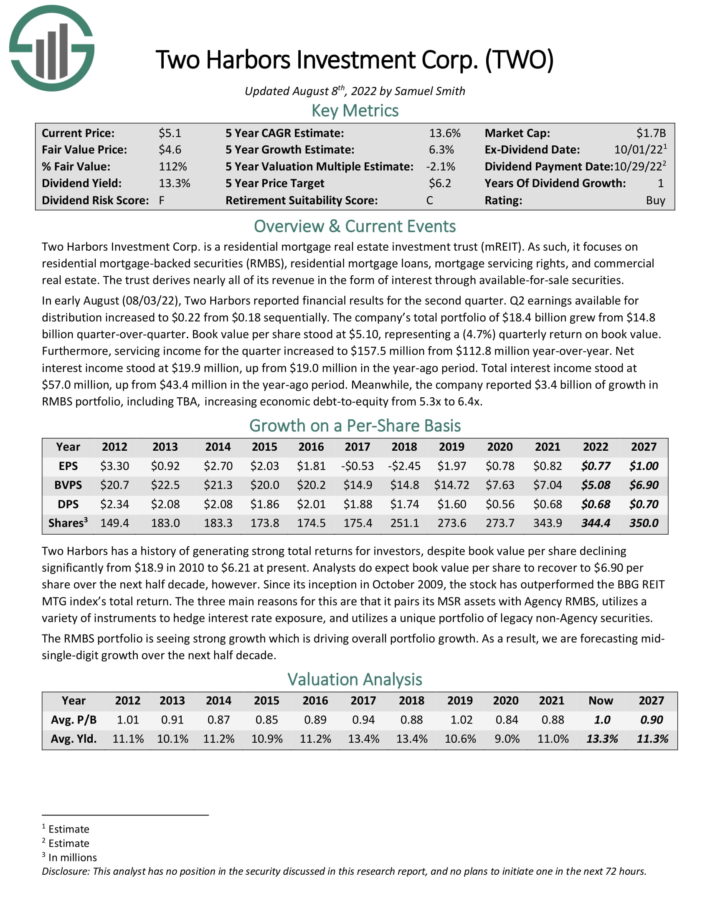

Excessive-Yield REIT No. 4: Two Harbors Funding Corp. (TWO)

Two Harbors Funding Corp. is a residential mortgage actual property funding belief (mREIT). As such, it focuses on residential mortgage–backed securities (RMBS), residential mortgage loans, mortgage servicing rights, and industrial actual property.

The belief derives practically all of its income within the type of curiosity via accessible–for–sale securities.

Supply: Investor Presentation

In early August (08/03/22), Two Harbors reported monetary outcomes for the second quarter. Q2 earnings accessible for distribution elevated to $0.22 from $0.18 sequentially. The corporate’s complete portfolio of $18.4 billion grew from $14.8 billion quarter-over-quarter. E book worth per share stood at $5.10, representing a (4.7%) quarterly return on guide worth.

Moreover, servicing revenue for the quarter elevated to $157.5 million from $112.8 million year-over-year. Internet curiosity revenue stood at $19.9 million, up from $19.0 million within the year-ago interval. Whole curiosity revenue stood at $57.0 million, up from $43.4 million within the year-ago interval. In the meantime, the corporate reported $3.4 billion of progress in RMBS portfolio, together with TBA, growing financial debt-to-equity from 5.3x to six.4x.

Click on right here to obtain our most up-to-date Positive Evaluation report on Two Harbors (TWO) (preview of web page 1 of three proven under).

Excessive-Yield REIT No. 3: New York Mortgage Belief (NYMT)

New York Mortgage Belief is an actual property funding belief, or REIT, that acquires, invests in, funds, and manages mortgage-related belongings and different monetary belongings. The belief doesn’t personal bodily actual property, however fairly seeks to handle a portfolio of investments which can be actual property associated. New York Mortgage Belief derives income from internet curiosity revenue and internet realized capital beneficial properties from its funding portfolio.

Supply: Investor Presentation

The belief primarily seeks to generate curiosity revenue from mortgage-related belongings, but it surely additionally owns some distressed monetary belongings the place it seeks to seize capital beneficial properties. The belief invests in residential mortgage loans, multi-family CMBS, most well-liked fairness, and three way partnership fairness.

Click on right here to obtain our most up-to-date Positive Evaluation report on NYMT (preview of web page 1 of three proven under):

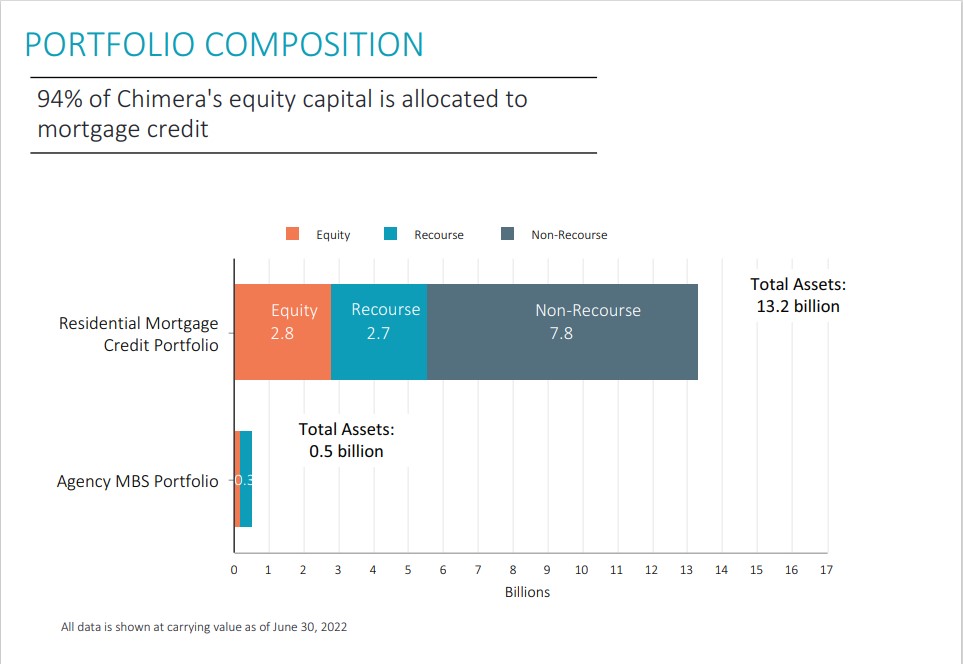

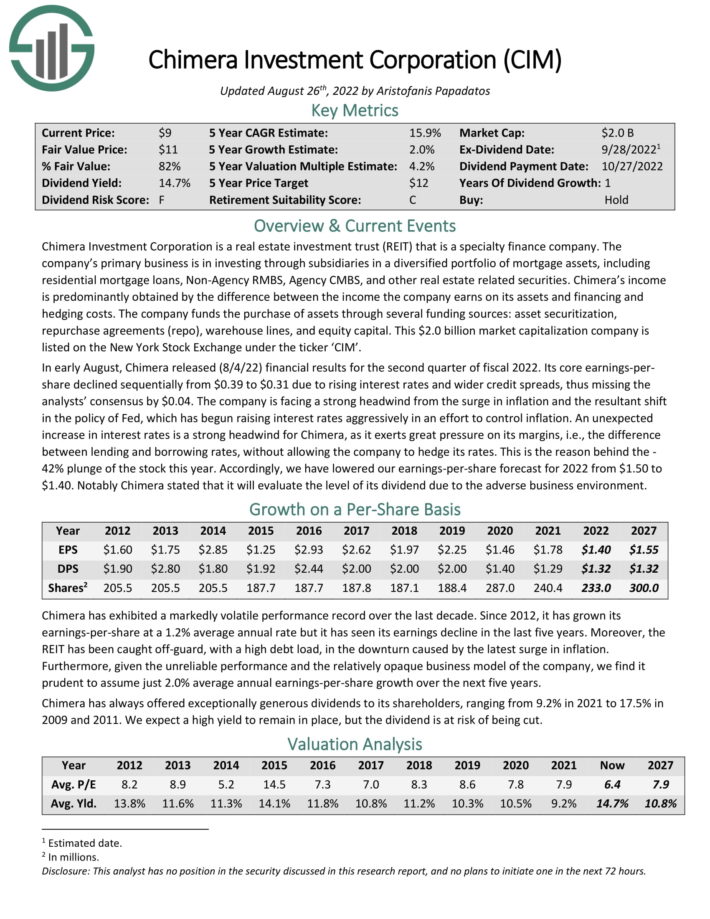

Excessive-Yield REIT No. 2: Chimera Funding Company (CIM)

Chimera Funding Company is an actual property funding belief (REIT) that may be a specialty finance firm. The corporate’s major enterprise is in investing via subsidiaries in a diversified portfolio of mortgage belongings, together with residential mortgage loans, Non-Company RMBS, Company CMBS, and different actual property associated securities.

Supply: Investor Presentation

Chimera’s revenue is predominantly obtained by the distinction between the revenue the corporate earns on its belongings and financing and hedging prices. The corporate funds the acquisition of belongings via a number of funding sources: asset securitization, repurchase agreements (repo), warehouse traces, and fairness capital.

Click on right here to obtain our most up-to-date Positive Evaluation report on CIM (preview of web page 1 of three proven under):

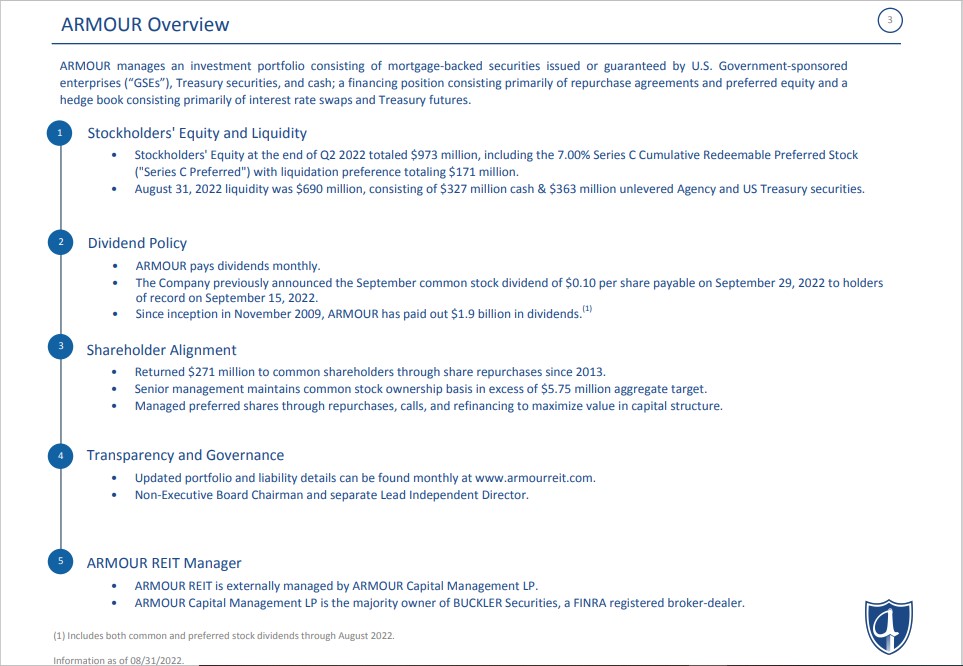

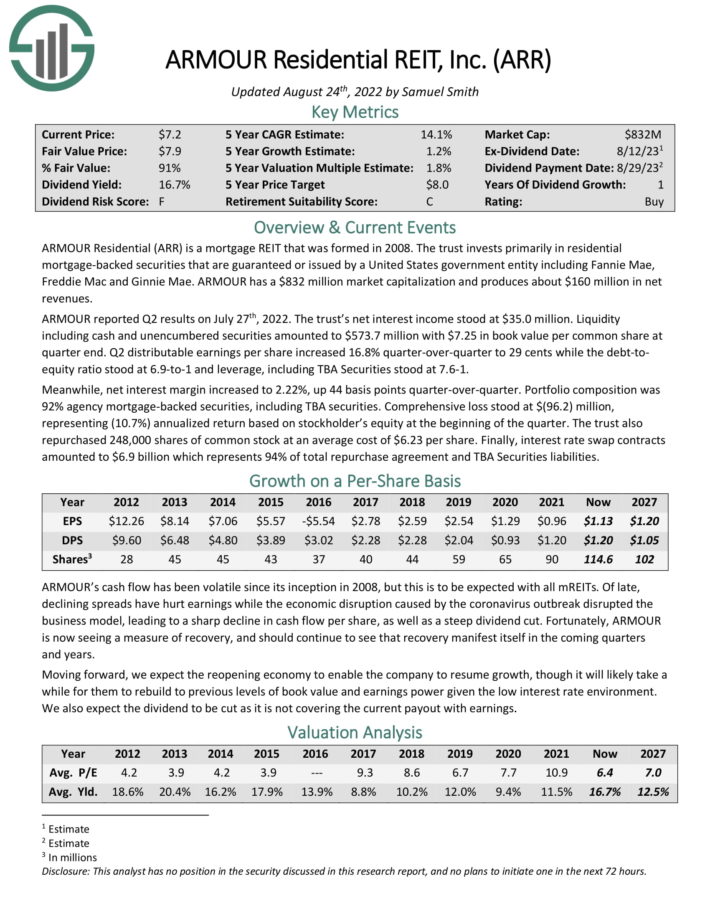

Excessive-Yield REIT No. 1: ARMOUR Residential REIT (ARR)

ARMOUR is a mortgage REIT that invests primarily in residential mortgage–backed securities that are assured or issued by a United States authorities entity together with Fannie Mae, Freddie Mac and Ginnie Mae. ARMOUR reported Q2 outcomes on July twenty seventh, 2022. The belief’s internet curiosity revenue stood at $35.0 million.

Supply: Investor Presentation

Liquidity together with money and unencumbered securities amounted to $573.7 million with $7.25 in guide worth per widespread share at quarter finish. Q2 distributable earnings per share elevated 16.8% quarter-over-quarter to 29 cents whereas the debt-to-equity ratio stood at 6.9-to-1 and leverage, together with TBA Securities stood at 7.6-1.

In the meantime, internet curiosity margin elevated to 2.22%, up 44 foundation factors quarter-over-quarter. Portfolio composition was 92% company mortgage-backed securities, together with TBA securities. Complete loss stood at $(96.2) million, representing (10.7%) annualized return primarily based on stockholder’s fairness originally of the quarter.

The belief additionally repurchased 248,000 shares of widespread inventory at a median price of $6.23 per share. Lastly, rate of interest swap contracts amounted to $6.9 billion which represents 94% of complete repurchase settlement and TBA Securities liabilities.

Click on right here to obtain our most up-to-date Positive Evaluation report on ARR (preview of web page 1 of three proven under):

Ultimate Ideas

REITs have vital attraction for revenue traders, because of their excessive yields. These 10 excessive high-yielding REITs are particularly enticing on the floor, though traders needs to be conscious that abnormally excessive yields are sometimes accompanied by elevated dangers.

At Positive Dividend, we frequently advocate for investing in corporations with a excessive chance of accelerating their dividends each yr.

If that technique appeals to you, it could be helpful to flick thru the next databases of dividend progress shares:

Thanks for studying this text. Please ship any suggestions, corrections, or inquiries to [email protected].