Tom Werner

I reiterated my ‘Purchase’ ranking for Apple (NASDAQ:AAPL) in my earlier article revealed in Might 2024, highlighting its sturdy progress in service enterprise. Since my final report, the inventory worth has surged by greater than 19%, considerably outperforming the S&P 500 index (SP500). Apple is about to report its Q3 consequence on August 1st. I anticipate sturdy progress in its service enterprise however weak iPhone income progress for FY24. Because the inventory worth is overvalued, as per my calculation, I downgrade to a ‘Promote’ ranking with honest worth of $180 per share.

Flat iPhone Development Anticipated

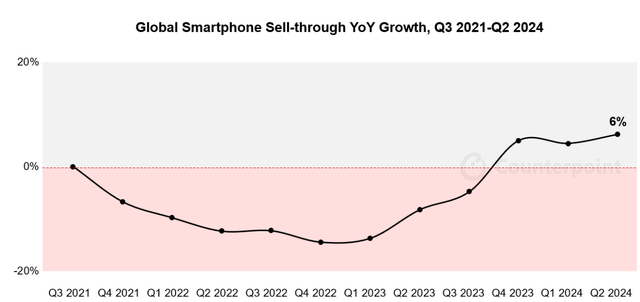

In accordance with the most recent Counterpoint report launched on July fifteenth, international smartphone sell-through grew 6% year-over-year for the third consecutive quarter, as illustrated within the chart under.

Counterpoint Report (As of July fifteenth 2024)

Nonetheless, Apple’s international iPhone gross sales are anticipated to stay flat within the Counterpoint report, with sturdy progress in Europe and LATAM, being offset by weak gross sales in China. As mentioned in my earlier article, Apple is going through sturdy competitors from Huawei in China. In April 2024, as reported by the media, Huawei launched its Pura 70 collection of smartphones, persevering with to create progress challenges for Apple in China. Better China accounted for greater than 18% of complete income in FY23; subsequently, China stays a vital marketplace for Apple.

I anticipate Apple’s smartphone enterprise in China will proceed to lose market share to native gamers, similar to Huawei and Xiaomi, and the important thing causes are as follows:

With the growing geopolitical tensions between the U.S. and China, the iPhone is unlikely to be favored within the home market in China as a result of patriotism amongst Chinese language native customers. The high-net-worth people in China favor the iPhone model; nevertheless, the penetration of wealth Chinese language is near the tip, for my part. Within the close to future, iPhone’s progress in China will primarily be pushed by substitute cycles. The rise of Huawei and its in-house developed chips might doubtlessly create vital progress challenges for Apple in China.

Sturdy Service Development Forward

Companies accounted for over 26% of complete income prior to now quarter, rising 14% year-over-year. As mentioned in my earlier coverages, I anticipate companies will turn out to be the brand new progress driver for Apple within the close to future. Apple possesses vital benefits within the service market, together with:

The huge variety of units in its put in base allows Apple to additional develop its subscription, App shops, fee and different companies. Solely Apple has the potential to leverage its units to increase its service enterprise. Apple has been integrating AI into its apps and ecosystem of {hardware} and repair. On June tenth, OpenAI and Apple introduced partnership to combine ChatGPT into Apple experiences, together with iOS, iPadOS and mac OS methods. I anticipate Apple will combine extra AI functionalities into its working methods and {hardware} sooner or later, driving extra subscriptions income progress.

General, I estimate Apple’s service enterprise will proceed to develop at mid-teens, contributing 4%-5% to the topline progress.

Outlook and Valuation

FY24 can be a transitional yr for Apple, because the iPhone 16 lineup is because of launch in September 2024. Based mostly on the efficiency of the primary two quarters, I estimate Apple will ship 3% income progress in FY24, with companies including 4% to topline progress and units dragging down complete progress by 1%.

From FY25 onwards, I forecast Apple’s normalized income progress to be 9%, assuming:

As mentioned, I anticipate Apple’s service enterprise will develop by 15% yearly, contributing 4%-5% to the general topline progress. The important thing progress drivers are the growing machine put in base, extra varieties of companies offered by iPhone ecosystems and ARPU progress. For different {hardware} enterprise, I assume Apple will ship 7% natural income progress, aligned with its historic progress common.

I anticipate 20bps working margin enlargement yearly, main pushed by:

10bps enlargement from gross income, pushed by growing service enterprise with higher margin profile. 10bps working leverage from SG&A

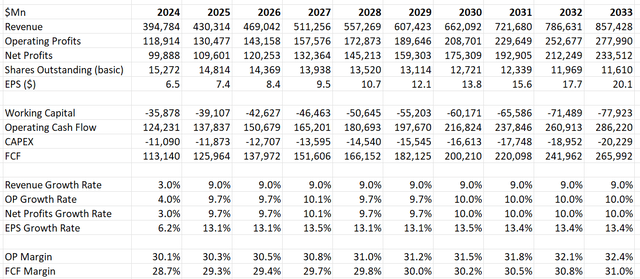

The DCF abstract may be discovered as follows:

Apple DCF – Writer’s Calculations

The WACC is calculated to be 12.5% assuming:

Danger free charge: 4.2% (US 10Y treasury yield) Beta: 1.19 (SA) Tax charge: 16% Fairness threat premium 7%; value of debt 7%. Fairness steadiness $3.34 trillion; debt steadiness $111 billion

The honest worth of Apple’s inventory is calculated to be $180 per share after discounting all the long run FCF.

Key Dangers

As reported by the media, the European Union fined Apple €1.84 billion for breaking its competitors legal guidelines for stopping Spotify (SPOT) from advising app customers cheaper methods to subscribe outdoors of Apple’s app retailer. It’s evident that Apple App Retailer is charging a 15-20% minimize from any fee throughout the retailer. I imagine the same complaints will come up sooner or later, as this price minimize proportion is kind of materials for app builders.

On July twenty fourth, Spain’s competitors authority, the CNMC, introduced the investigation into Apple’s App Retailer. It’s too early to foretell the result of the investigation; nevertheless, these investigations might pressure Apple to alter its insurance policies for its App retailer fee.

As I give Apple a ‘Promote’ ranking, I’m contemplating the next upside dangers:

Apple plans to allocate $110 billion in direction of shares repurchase, growing the quantity of capital returned to shareholder. The huge shares repurchase might doubtlessly increase Apple’s inventory worth within the near-term. Apple might probably ship higher-than-expected service income progress, which might please the market. I’ve to acknowledge that Apple is kind of sturdy in cloud, video, fee options, streaming and different companies.

Finish Notice

Whereas I anticipate iPhone income progress to be beneath stress within the close to time period attributable to weak China gross sales, Apple’s companies would proceed to develop at mid-teens, contributing progress for Apple. Nonetheless, the inventory worth is overvalued as per my calculations, I downgrade to a ‘Promote’ ranking with honest worth of $180 per share.