The know-how sector is presently experiencing one thing of a renaissance as breakthroughs in synthetic intelligence (AI) have ignited newfound curiosity from traders.

Among the many high AI alternatives are a small cohort of megacap tech firms collectively known as the “Magnificent Seven.” During the last yr and a half, semiconductor firm Nvidia (NASDAQ: NVDA) has returned 628% — greater than another member of the Magnificent Seven.

Nvidia is undoubtedly taking part in an enormous function within the AI revolution, and its near-term prospects look very sturdy. However what about the long run?

Amongst its Magnificent Seven friends, I see Amazon (NASDAQ: AMZN) because the superior funding alternative. Let’s discover why Nvidia is presently on a roll, and assess the long-term prospects of the chipmaker versus Amazon.

Nvidia is supercharged, however competitors lingers

Generative AI functions, corresponding to coaching massive language fashions, machine studying, and accelerated computing, depend on a few key elements. Specifically, subtle semiconductor chips often called graphics processing items (GPUs), in addition to knowledge heart community companies, are integral for AI use circumstances.

Proper now, Nvidia sits conveniently on the intersection of GPUs and knowledge heart operations. At present, the corporate is estimated to have 80% of the addressable marketplace for AI chips.

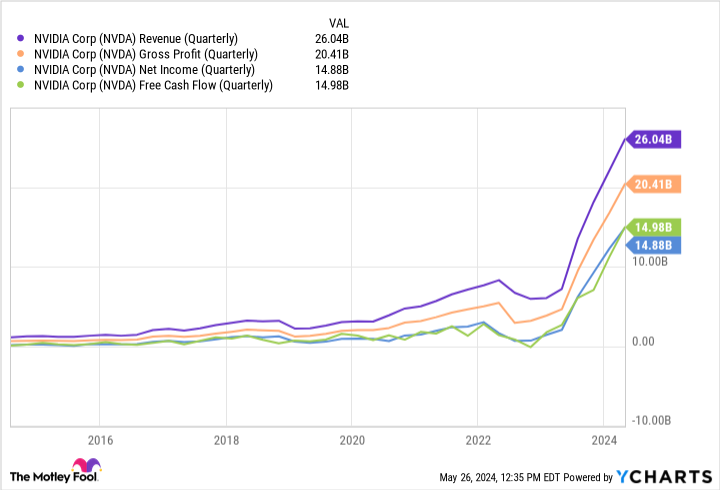

This commanding lead has translated into report income, margins, and money circulation.

The slope of the traces within the chart above underscores Nvidia’s dominance. Demand for the corporate’s chips and knowledge heart companies is strong, and has offered Nvidia with a profitable supply of pricing energy. Nonetheless, Superior Micro Units and Intel are creating a set of other GPUs.

Though neither firm has wherever close to the market share of Nvidia right now, the longer-term secular tailwinds fueling AI recommend that there might be a possibility to make up floor as Nvidia faces the problem of matching buyer demand traits with provide output.

Moreover, Nvidia is just not solely going through competitors from different chip companies. Meta Platforms and Amazon are each engaged on their very own internally developed chips in an effort to maneuver away from their reliance on Nvidia.

Though I do not see both firm migrating from Nvidia anytime quickly, the longer-term image means that a few of Nvidia’s main prospects might be a much less vital supply of development a number of years from now.

Why I see Amazon as the higher funding

In the present day, Amazon is finest identified for its e-commerce market and cloud computing infrastructure — Amazon Internet Providers (AWS). Nonetheless, Amazon has a lot of different alternatives in its ecosystem, together with streaming, grocery supply, and promoting.

Story continues

This diversified enterprise is what has me most bullish on Amazon’s long-term prospects, as a result of the corporate has a novel alternative to amplify its attain by integrating AI throughout its complete operation.

One of the vital profitable strikes Amazon has already made is its $4 billion funding into AI start-up Anthropic. Anthropic makes use of AWS as its major cloud supplier, and is coaching its generative AI fashions on Amazon’s homegrown chips.

Furthermore, Amazon additionally just lately dedicated $11 billion to construct out knowledge facilities — a transfer I see as a serious validation that the corporate is severe about transferring away from Nvidia in the long term.

Whereas the long-term features from these initiatives are possible years sooner or later, I am optimistic that Amazon is laying the groundwork for sustained development. Checked out a unique means, whereas Nvidia is presently having fun with triple-digit income and revenue development, I am skeptical that the corporate can sustain such momentum. Alternatively, I believe Amazon is simply scratching the service of a brand new wave fueled by aggressive ambitions that includes AI.

The underside line

Relating to selecting between Nvidia and Amazon, I do not assume you’ll be able to go unsuitable. Each firms are working from positions of power, and every represents compelling funding prospects.

With that mentioned, Nvidia’s inventory value has risen sharply over the past couple of years. Provided that competitors lingers throughout each knowledge heart companies and AI-powered chips, I do not see Nvidia sustaining its lead. Ultimately, I believe prospects will broaden their AI infrastructure and complement present Nvidia companies with these from different distributors.

In flip, this dynamic would lead to decelerating income and profitability for Nvidia within the coming years. Against this, Amazon already boasts over $50 billion in free money circulation and $84 billion of money and equivalents on its stability sheet.

Amazon is in a extremely great spot, financially talking, and has the flexibleness to proceed doubling down on its AI efforts. In consequence, I believe Amazon will ultimately surpass Nvidia by way of worth because it grows right into a extra subtle enterprise.

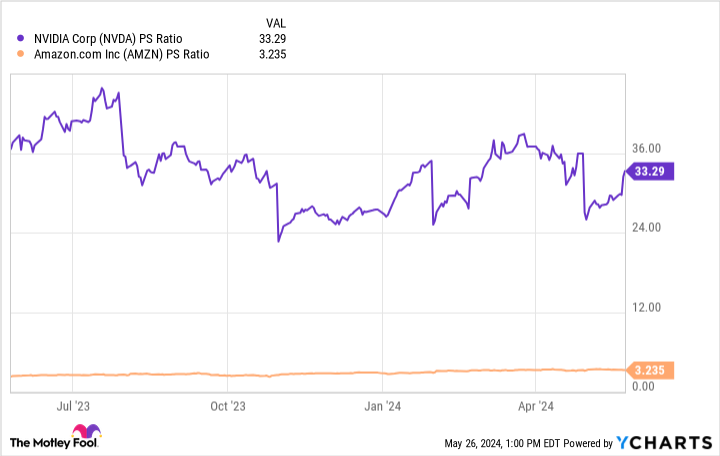

Contemplating the disparity between valuation multiples, I would scoop up shares of Amazon and plan to carry them for the long term. Nvidia is buying and selling at a noticeable premium, thereby suggesting some future development could also be priced into the inventory. To me, Amazon’s place within the AI realm is underappreciated, and the inventory seems grime low-cost proper now. I would encourage traders to benefit from this low cost and proceed monitoring the corporate’s progress.

Must you make investments $1,000 in Amazon proper now?

Before you purchase inventory in Amazon, take into account this:

The Motley Idiot Inventory Advisor analyst workforce simply recognized what they imagine are the 10 finest shares for traders to purchase now… and Amazon wasn’t considered one of them. The ten shares that made the lower might produce monster returns within the coming years.

Contemplate when Nvidia made this checklist on April 15, 2005… in case you invested $1,000 on the time of our suggestion, you’d have $671,728!*

Inventory Advisor offers traders with an easy-to-follow blueprint for fulfillment, together with steering on constructing a portfolio, common updates from analysts, and two new inventory picks every month. The Inventory Advisor service has greater than quadrupled the return of S&P 500 since 2002*.

See the ten shares »

*Inventory Advisor returns as of Might 28, 2024

John Mackey, former CEO of Entire Meals Market, an Amazon subsidiary, is a member of The Motley Idiot’s board of administrators. Randi Zuckerberg, a former director of market improvement and spokeswoman for Fb and sister to Meta Platforms CEO Mark Zuckerberg, is a member of The Motley Idiot’s board of administrators. Adam Spatacco has positions in Amazon, Meta Platforms, and Nvidia. The Motley Idiot has positions in and recommends Superior Micro Units, Amazon, Meta Platforms, and Nvidia. The Motley Idiot recommends Intel and recommends the next choices: lengthy January 2025 $45 calls on Intel and brief Might 2024 $47 calls on Intel. The Motley Idiot has a disclosure coverage.

Prediction: This “Magnificent Seven” Synthetic Intelligence (AI) Inventory May Be a Higher Funding Than Nvidia Over the Subsequent 5 Years was initially revealed by The Motley Idiot

Dips in Worth After Undertaking Delays Protocol Improve")