Dilok Klaisataporn

Chubb Restricted (NYSE:CB) has had an outstanding monetary efficiency after my earlier evaluation, posting growing margins and stable income progress past my earlier evaluation’ expectations. Extra just lately in Q1, Warren Buffett appears to have famous the inventory as a great shopping for alternative, as a current 13F submitting reveals Berkshire Hathaway’s (BRK.A) (BRK.B) newly purchased stake in Chubb.

I beforehand wrote an article on Chubb titled “Chubb: A Comparatively Low cost Savehaven”, score the inventory at purchase as a consequence of a seeming undervaluation with Chubb’s steady earnings. The textual content was printed on the eleventh of September in 2023. Since, the inventory has had a complete return of 34% in comparison with an S&P 500 appreciation of 18%. The corporate continues to submit good financials, and the inventory continues to be undervalued regardless of a better inventory worth.

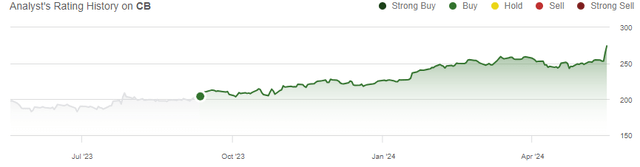

My Ranking Historical past on CB (Looking for Alpha)

Chubb’s Monetary Efficiency Has Been Nice

Chubb has had an extremely good monetary efficiency after my earlier evaluation, posting nice progress all through Q3/2023 to Q1/2024. Most just lately in Q1, Chubb confirmed a 14.2% year-over-year progress in web premiums written with a continually good efficiency between segments. Most notably within the quarter, life insurance coverage premiums written confirmed a progress of 26.3%.

Together with good income progress, Chubb has posted growing margins. Chubb had a 20.3% year-over-year progress in core working earnings in Q1, elevating the margin in comparison with written premiums to 18.1% in comparison with 17.2% in Q1/2023. Chubb continues to see beneficial results from greater pricing contributing each to progress in written premiums in greenback phrases and better margins.

The Q1 financials comply with a great second half of 2023, the place Chubb additionally managed to develop written premiums and working margins past my earlier evaluation’ DCF mannequin expectations. Whereas pricing will increase cannot be extrapolated additional very a lot, they nonetheless look to sustainably elevate Chubb’s working margin stage expectations. As Chubb’s earnings have grown effectively, the corporate just lately raised its dividend right into a quarterly fee of $0.91, making the inventory’s present dividend yield a comparatively low 1.33%.

Warren Buffett’s Berkshire Hathaway Buys a Stake in Chubb

With a current 13F submitting launched on the fifteenth of Could, Warren Buffett’s funding agency Berkshire Hathaway disclosed a 25.9 million share stake in Chubb price round $7.1 billion on the time of writing. The inventory rose by 5% on the sixteenth of Could following the 13F disclosure as Berkshire Hathaway has taken a major place within the firm, representing round 6% of Chubb’s whole shares.

Berkshire Hathaway had been constructing a place within the firm in earlier quarters beneath a confidential submitting. It appears that evidently the place has now been constructed with no important additional add-ons seemingly as Berkshire Hathaway has not seeked confidentiality for the inventory purchases. With Berkshire Hathaway already holding important positions in insurance coverage, I do not count on that an acquisition is probably going as a consequence of regulatory points – Warren Buffett’s place within the firm does not look more likely to concretely have an effect on the funding case for Chubb, though a vote of confidence from the funding mogul strengthens religion within the funding.

Aggressive Trade

The property and casualty insurance coverage business has a lot of opponents. For instance, publicly traded The Progressive Company (PGR), The Vacationers Corporations (TRV), and The Allstate Company (ALL) have a mixed market capitalization of $218 billion. Insurance coverage is general a difficult business to drive differentiation from opponents in, because the service is extremely standardized with pricing being the clearest type of differentiation.

Nonetheless, in comparison with the talked about giant publicly traded opponents, Chubb has managed to develop earnings extra constantly. Whereas the opponents appear to even have benefited from elevated pricing in current quarters elevating margins, Chubb’s progress within the business has general been extra steady. Chubb boasts a clearly higher underwriting ratio in comparison with a number of opponents, making the corporate very aggressive within the business.

Total, the P&C insurance coverage business is predicted to have a great 2024. The Swiss Re Institute estimates premiums to indicate a progress of seven.0% within the 12 months pushed by private strains. Easing inflation and higher funding returns are additionally anticipated to enhance the business’s profitability right into a ROE of 9.5% in 2024 and 10.0% in 2025, which might already be seen in Chubb’s and its opponents’ margins.

Valuation Continues to Have Important Upside

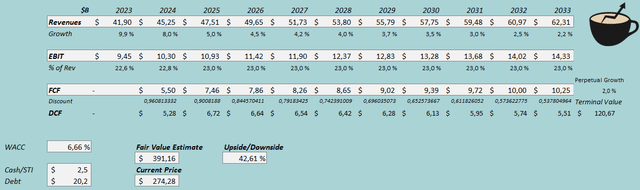

On account of Chubb’s nice financials in current quarters, my DCF mannequin’s assumptions see room for change. I now estimate revenues primarily based on web premiums written in P&C and estimate a CAGR of 4.0% from 2023 to 2033, in comparison with a CAGR of three.7% from 2022 to 2032 in my earlier DCF mannequin. The perpetual progress charge is unchanged at 2%. On account of Chubb’s greater reported margins, I now estimate the corporate’s working earnings at a considerably greater stage – for instance for 2024, I now estimate an EBIT of $10.3 billion as a substitute of $8.2 billion in my earlier DCF mannequin representing a margin of twenty-two.8% in 2024 and 23.0% from 2025 ahead. I adjusted the money circulate conversion downwards.

With the talked about estimates, the DCF mannequin estimates Chubb’s honest worth at $391.16, round 43% above the inventory worth on the time of writing. The inventory continues to have a seeming undervaluation because the current earnings trajectory has raised my money circulate estimates considerably.

DCF Mannequin (Creator’s Calculation)

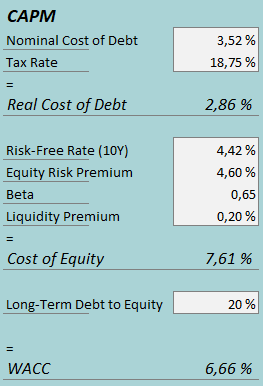

A weighted common price of capital of 6.66% is used within the DCF mannequin. The used WACC is derived from a capital asset pricing mannequin:

CAPM (Creator’s Calculation)

In Q1, Chubb had $178 million in curiosity bills. With the corporate’s present quantity of interest-bearing debt, Chubb’s annualized rate of interest comes as much as 3.52%. I hold my long-term debt-to-equity ratio estimate the identical at 20%. For the risk-free charge on the price of fairness aspect, I exploit the USA’ 10-year bond yield of 4.42%. The fairness threat premium of 4.60% is Professor Aswath Damodaran’s newest estimate for the USA, up to date on the fifth of January. I exploit the identical beta estimate of 0.65 as within the earlier CAPM. Lastly, I add a small liquidity premium of 0.2%, creating a price of fairness of seven.61% and a WACC of 6.66%. The WACC is down from a earlier estimate of seven.38% as a consequence of a decrease fairness threat premium estimate.

Dangers

Whereas Chubb is comparatively proof against macroeconomic turbulence, the corporate is not fully resistant to macroeconomic components. Chubb has a great quantity of debt on the corporate’s stability sheet – rates of interest affect the corporate, though the impact is kind of modest.

Chubb’s current excessive margins might additionally solely be excessive briefly, and potential margin deterioration might worsen the funding case significantly. A major disaster might trigger Chubb important losses resulting in worsening earnings – for instance, the corporate has misplaced a major quantity because of the Baltimore bridge collapse. Chubb does have a worldwide and diversified insurance coverage portfolio with solely 19% of premiums coming from giant company industrial P&C, although, making very important one-off funds unlikely to trigger an excessive amount of earnings turbulence.

Takeaway

Chubb’s monetary efficiency after my earlier evaluation has been nice, characterised by good progress and excessive margins with the corporate’s worth will increase. Warren Buffett’s Berkshire Hathaway has additionally taken discover of Chubb’s good financials, as the corporate has purchased a stake price $7.1 billion within the firm as per a current 13F submitting. Whereas concrete modifications within the funding case is not altered by the Berkshire Hathaway stake, the corporate’s stake in Chubb solidifies religion within the funding. The valuation continues to supply a great worth for traders, and as such, I hold my score for Chubb at purchase.

")

")

This fall 2024 Earnings Name Transcript")