Takako Hatayama-Phillips

Earnings of Westamerica Bancorporation (NASDAQ: NASDAQ:WABC) will most probably decline this 12 months due to a lackluster development of the steadiness sheet and a decline within the web curiosity margin. General, I’m anticipating the corporate to report earnings of $5.40 per share for 2024, down 10.8% year-over-year. My valuation evaluation reveals that the market has overreacted to the prospects of an earnings dip this 12 months. There could also be some cash to make right here as the worth corrects and will get nearer to its truthful worth. Because of this, I’m adopting a purchase ranking on Westamerica Bancorporation.

Anticipating a Steady Steadiness Sheet

Though WABC’s mortgage portfolio continued to say no within the first quarter, the corporate managed to extend its asset dimension in the course of the quarter. That is fairly an achievement because the asset dimension has been lowering for the final two years.

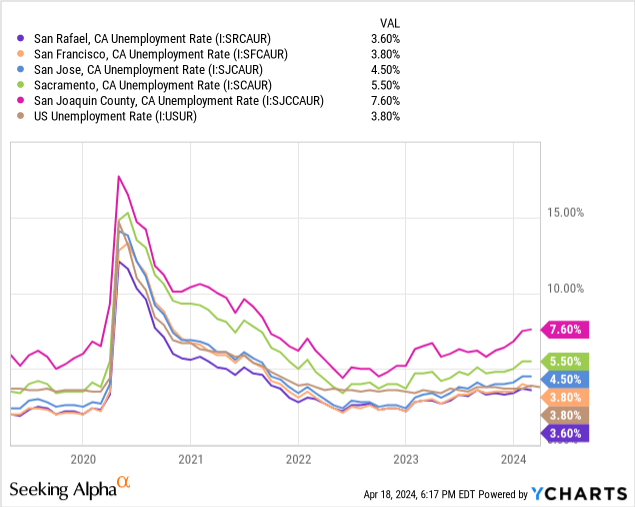

Nonetheless, I don’t assume the steadiness sheet can proceed to develop on the first quarter’s fee within the 12 months forward as a result of the working atmosphere continues to be difficult. Westamerica Bancorporation principally operates in Northern and Central California, from Mendocino, Lake, and Nevada Counties within the north to Kern County within the south. Unemployment charges within the main cities and counties in Northern and Central California have been trending upward in current months and are principally worse than the nationwide common, as proven beneath.

Because of this, I feel the steadiness sheet dimension will possible stay principally unchanged for the rest of this 12 months. Additional, I consider that loans will improve whereas securities will lower due to the anticipated rate of interest development. I’m anticipating the Fed funds fee to dip by 50-75 foundation factors this 12 months, which is able to improve the demand for loans.

General, I’m anticipating the mortgage guide to develop by 1.2%, and securities to dip by 2.9% in 2024. The next desk reveals my steadiness sheet estimates.

Monetary Place FY19 FY20 FY21 FY22 FY23 FY24E Web Loans 1,107 1,232 1,045 938 850 860 Progress of Web Loans NA 11.3% (15.2)% (10.2)% (9.4)% 1.2% Different Incomes Property 3,817 4,579 4,945 5,248 4,878 4,830 Deposits 4,813 5,688 6,414 6,225 5,474 5,315 Borrowings and Sub-Debt 31 103 146 58 58 254 Widespread fairness 731 845 827 602 773 964 E-book Worth Per Share ($) 27.1 31.3 30.8 22.4 28.9 36.1 Tangible BVPS ($) 22.5 26.8 26.2 17.8 24.4 31.6 Supply: SEC Filings, Earnings Releases, Creator’s Estimates(In USD million until in any other case specified) Click on to enlarge

Additional Margin Compression Probably

After a development of 120 foundation factors final 12 months, the web curiosity margin shrank by 11 foundation factors within the first quarter of 2024. I feel the margin can proceed to slide within the 12 months forward as a result of funding prices are stickier than asset yields. The funding prices are downward sticky as a result of WABC has a really low-cost deposit base. In actual fact, the corporate’s funding price was simply 0.22% in the course of the first quarter of the 12 months. Because of this, it could’t fall a lot decrease when rates of interest begin declining this 12 months.

The common asset yield will possible dip this 12 months due to loans, which make up round 15% of the corporate’s whole incomes property. I’m anticipating the Fed funds fee to say no by 50-75 foundation factors this 12 months. Because of this, I’m anticipating the web curiosity margin to dip by round six foundation factors within the final 9 months of 2024.

Anticipating Earnings to Dip Due to a Unfavourable Outlook on the Margin and Steadiness Sheet

I’m anticipating the earnings of Westamerica Bancorporation to say no this 12 months as a result of the incomes property will most likely dip. Moreover, the web curiosity margin will possible development downwards, which is able to harm earnings. My margin and steadiness sheet estimates (mentioned above) result in a web curiosity revenue of $261 million. Additional, I am anticipating that the declining development for non-interest revenue will proceed and the non-interest expense will proceed to develop at a standard fee. For provisioning bills, I am anticipating the primary quarter’s fee to proceed.

These assumptions result in an earnings estimate of $5.40 per share for 2024, down 10.8% year-over-year. The next desk reveals my revenue assertion estimates.

Earnings Assertion FY19 FY20 FY21 FY22 FY23 FY24E Web curiosity revenue 157 164 171 220 280 261 Provision for mortgage losses – 4 – – (1) 1 Non-interest revenue 47 46 43 45 44 41 Non-interest expense 99 99 98 99 103 106 Web revenue – Widespread Sh. 80 80 87 122 162 144 EPS – Diluted ($) 2.98 2.98 3.22 4.54 6.06 5.40 Supply: SEC Filings, Earnings Releases, Creator’s Estimates(In USD million until in any other case specified) Click on to enlarge

Dangers Attributable to the Securities Portfolio

As a result of most of Westamerica Bancorporation’s property are in securities, the unrealized mark-to-market losses on the Out there-For-Sale securities portfolio are the most important supply of threat. These unrealized losses amounted to $271.5 million on the finish of December 2023, which is round 34% of the overall fairness guide worth, in keeping with particulars given within the 10-Okay submitting. (Observe: this determine isn’t out there but for the March-ending quarter.

Aside from the unrealized mark-to-market losses on securities, Westamerica Bancorporation’s threat stage seems subdued. Non-performing loans made up simply 0.18% of whole loans on the finish of March 2024, as talked about within the earnings launch.

WABC is Providing a Dividend Yield of three.8%

Westamerica Bancorporation is providing a dividend yield of three.8% on the present quarterly dividend fee of $0.44 per share. Regardless of the adverse earnings outlook, I feel the dividend payout is safe. The earnings and dividend estimates counsel a payout ratio of 32.6% for 2024, which is far beneath the five-year common of 45%. Furthermore, the corporate is well-capitalized, subsequently, there’s barely any likelihood that regulatory necessities would power a dividend minimize. The corporate reported a complete capital ratio of 15.64% for the tip of December 2023 versus a minimal regulatory requirement of 10.50%. (This ratio hasn’t been up to date for the March-ending quarter as but.)

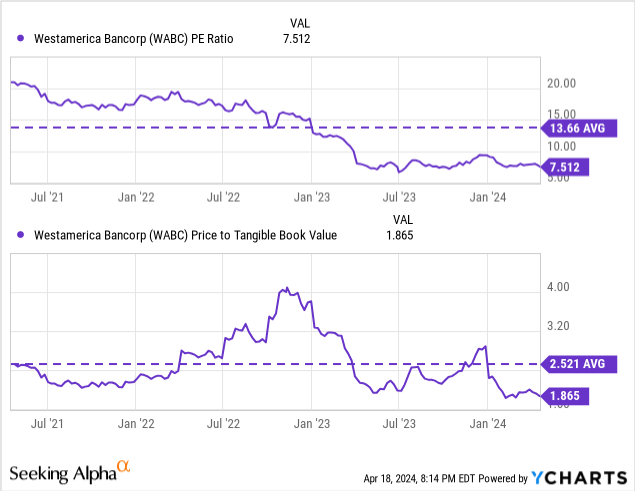

WABC Seems Undervalued

Historic evaluation reveals that WABC is at present buying and selling at a giant low cost to its historic multiples.

Because the historic multiples seem a bit excessive, I’ve determined to make use of the peer common price-to-tangible guide (“P/TB”) and price-to-earnings (“P/E”) multiples to worth Westamerica Bancorporation. Friends are buying and selling at a median P/TB ratio of 1.38 and a median P/E ratio of 10.8, as proven beneath.

WABC NBHC HOPE BUSE SYBT Common P/E (“ttm”) 7.52 8.82 9.39 10.03 11.71 9.99 P/E (“fwd”) 8.56 10.1 9.85 10.64 12.74 10.83 P/TB (“ttm”) 1.81 1.46 0.76 1.32 1.96 1.38 P/B (“ttm”) 1.57 1.02 0.59 0.95 1.47 1.01 Supply: Searching for Alpha Click on to enlarge

Multiplying the typical P/TB a number of with the forecast tangible guide worth per share of $31.6 offers a goal worth of $43.4 for the tip of 2024. This worth goal implies a 7.2% draw back from the April 19 closing worth. The next desk reveals the sensitivity of the goal worth to the P/TB ratio.

P/TB A number of 1.18x 1.28x 1.38x 1.48x 1.58x TBVPS – Dec 2024 ($) 31.6 31.6 31.6 31.6 31.6 Goal Value ($) 37.1 40.3 43.4 46.6 49.7 Market Value ($) 46.8 46.8 46.8 46.8 46.8 Upside/(Draw back) (20.7)% (13.9)% (7.2)% (0.4)% 6.3% Supply: Creator’s Estimates Click on to enlarge

Multiplying the typical P/E a number of with the forecast earnings per share of $5.40 offers a goal worth of $58.5 for the tip of 2024. This worth goal implies a 25.2% upside from the April 19 closing worth. The next desk reveals the sensitivity of the goal worth to the P/E ratio.

P/E A number of 8.8x 9.8x 10.8x 11.8x 12.8x EPS 2024 ($) 5.40 5.40 5.40 5.40 5.40 Goal Value ($) 47.7 53.1 58.5 64.0 69.4 Market Value ($) 46.8 46.8 46.8 46.8 46.8 Upside/(Draw back) 2.0% 13.6% 25.2% 36.7% 48.3% Supply: Creator’s Estimates Click on to enlarge

Equally weighting the goal costs from the 2 valuation strategies offers a mixed goal worth of $51.0, which means a 9.0% upside from the present market worth. Including the ahead dividend yield offers a complete anticipated return of 12.7%. As Westamerica Bancorporation seems undervalued, I’m adopting a purchase ranking on the inventory.

(NASDAQ:OGI)")