18 housing traits that outlined the 12 months, together with report mortgage charges, depleted stock, and dwindling dwelling gross sales

2023 was a tough 12 months for the housing market. It began with a continuation of destructive traits from the tip of 2022 and changed into the least inexpensive 12 months for dwelling shopping for on report.

Seasonal traits buckled. The spring homebuying season by no means occurred, housing stock remained traditionally low all year long, and gross sales plummeted.

The market was so tough that greater than half of current homebuyers believed shopping for a house was extra hectic than courting, and almost 40% of homebuyers beneath 30 obtained cash from their household to afford a down fee.

So what occurred? Briefly: Document mortgage charges, excessive inflation, and persistently excessive housing and rental costs. However there was much more to it as effectively.

Beneath are traits, knowledge factors, and visuals that outlined the 2023 housing market.

All knowledge is aggregated from January by November 2023, and doesn’t embody December except in any other case acknowledged. December knowledge is thru the fifteenth of the month. All knowledge is from Redfin, FRED, NAR, and/or public data. For questions on metrics, learn our metrics definitions web page.

1. Residence costs rose to near-record highs

The U.S. median sale worth peaked at $425,000 in June, just under final 12 months’s report excessive of $433,000. Nevertheless, when averaging over the complete 12 months, 2023’s common median sale worth was larger than any earlier 12 months in historical past, rising from $407,000 in 2022 to $409,000.

“The bizarre mixture of low provide and low demand induced dwelling costs to stay elevated all year long, which was unhealthy information for just about everybody,” laments Daryl Fairweather, Redfin Senior Chief Economist. “The market was extraordinary; it felt sizzling, although only a few properties modified arms.”

2. San Francisco was the costliest metro space for homebuyers in 2023

Nonetheless the costliest metropolitan space (metro) within the nation, the median sale worth of a house in San Francisco was $1,446,000 in 2023, down 4.2% 12 months over 12 months.

The highest six costliest metros have been all in California.Milwaukee noticed the most important year-over-year worth enhance within the nation, rising 8.8%.Three Florida metros have been among the many ten metros with the most important year-over-year will increase: Miami (8.4%), West Palm Seashore (7.6%), and Fort Lauderdale (7.2%).

The highest ten costliest metros to purchase a house in 2023

MetroMedian sale priceYear-over-year changeSan Francisco, CA$1,446,000 -3.4%San Jose, CA$1,431,250+0.5%Anaheim, CA$1,029,000+3.9%Oakland, CA $903,000-4.8%Los Angeles, CA$846,000-0.7%San Diego, CA$845,000+3.5%Seattle, WA$766,000-1.3%New York, NY$684,500+0.4%Boston, MA$677,500+4.4%Nassau County, NY$617,400+1.8%

Information contains the yearly median sale costs out of all properties offered in every of the 50 largest metropolitan areas. Information doesn’t consider native median incomes and residential affordability.

3. Detroit was the least costly metro space for homebuyers in 2023

The median sale worth for a house in Detroit was $173,450 in 2023, down 2.7% 12 months over 12 months. Despite the fact that costs fell in 2023, properties in Detroit are costlier than they have been earlier than the pandemic, as an inflow of individuals trying to find affordability have pushed up costs.

“Residence costs remained pretty secure in Detroit and even rose in some areas,” says Anne Loehr, a Detroit Redfin agent. “Nevertheless, throughout the town, not too long ago up to date properties went for probably the most cash.”

Eight of probably the most inexpensive U.S. metros noticed costs rise as homebuyers pounced on inexpensive housing.9 of the ten least costly metros have been all situated within the Rust Belt, a geographic area close to the Nice Lakes and Appalachians.Three pandemic homebuying boomtowns noticed the most important year-over-year worth drops: Austin (-9.7%), Oakland (-4.8%), and Phoenix (-3.9%).

The highest ten least costly metros to purchase a house in 2023

MetroMedian sale priceYear-over-year changeDetroit, MI $173,450-2.7%Cleveland, OH $204,800+2.3%Pittsburgh, PA$218,400+1.1%St. Louis, MO$246,700+3.6%Philadelphia, PA$264,150-1.9%Cincinnati, OH$270,400+7.5%Warren, MI$285,600+4.1%Indianapolis, IN$290,350+5.2%Milwaukee, WI $299,250+8.8%Kansas Metropolis, MO$310,200+3.9%

Information contains the yearly median sale costs out of all properties offered in every of the 50 largest metropolitan areas. Information doesn’t consider native median incomes and residential affordability.

4. Lease costs remained traditionally excessive however stopped wanting new report

The median U.S. lease worth hit $2,050 in August 2023, matching the report worth of $2,050 set in August 2022. Yr-over-year worth modifications have been flat till November after they dropped considerably, as a rise in stock and vacancies pressured landlords to carry rents regular or drop them. Different contributors to the quieter rental market: Robust new building within the condominium trade, and fewer new households forming (two or extra individuals dwelling collectively).

“November supplied probably the most aid for renters,” says Maggie McCombs, managing editor of Lease., a Redfin firm. “Costs dropped by 2.1%, marking the first time in additional than three and half years that costs fell by greater than a single %. We count on decreases to proceed into 2024.”

This was in stark distinction to the previous two years, which went from sudden development throughout the pandemic to a free-fall within the second half of 2022.

“One of many largest modifications in comparison with 2022 was the slowdown within the rental market,” provides Fairweather. “Final 12 months, lease costs skyrocketed within the first half of the 12 months as a result of low provide and excessive demand. Nevertheless, in 2023, provide started to catch up, inflicting many landlords to maintain costs flat amid larger emptiness charges.”

Despite the fact that development slowed, the typical lease worth for all months by November in 2023 rose $10 to $1,992, the very best in historical past. This solely worsened the affordability disaster throughout the nation, particularly for decrease earnings households. Lease development has outpaced wages for many years, however the latest knowledge states that the typical renter now spends 30% of their earnings or extra on lease.

The U.S. at present has a scarcity of seven.3 million inexpensive housing items for individuals who want them, and no state has an enough provide.

Information contains the 2023 common aggregated median lease costs for every of the 50 largest core-based statistical areas (CBSAs) in comparison with 2022 knowledge from the identical interval.

5. Inflation remained stubbornly excessive earlier than lastly falling

The costs of products and companies rose 6.6% 12 months over 12 months in February, just under 2022’s excessive and the second-highest inflation stage since August 1982. Inflation then fell steadily all year long, albeit nonetheless above wholesome ranges.

As rates of interest hovered round 0.5% for everything of the pandemic, inflation took off as a result of provide crunches and elevated shopper demand. The Fed raised its benchmark charge in 2022 to fight inflation and funky the economic system – that started working this 12 months, however larger rates of interest led to larger mortgage charges, which slowed the housing market. Curiosity stays excessive as we finish 2023, however economists count on them to begin coming down subsequent 12 months.

Because the Fed started elevating the goal charges in March 2022, they’ve elevated it 11 instances to the present vary of 5.25-5.5%.Inflation remained highest in pandemic boomtowns due partly to the sudden soar in home costs, which is a key contributor to inflation.

Information courtesy of FRED. Information measures CPI (much less meals and power) by November 2023.

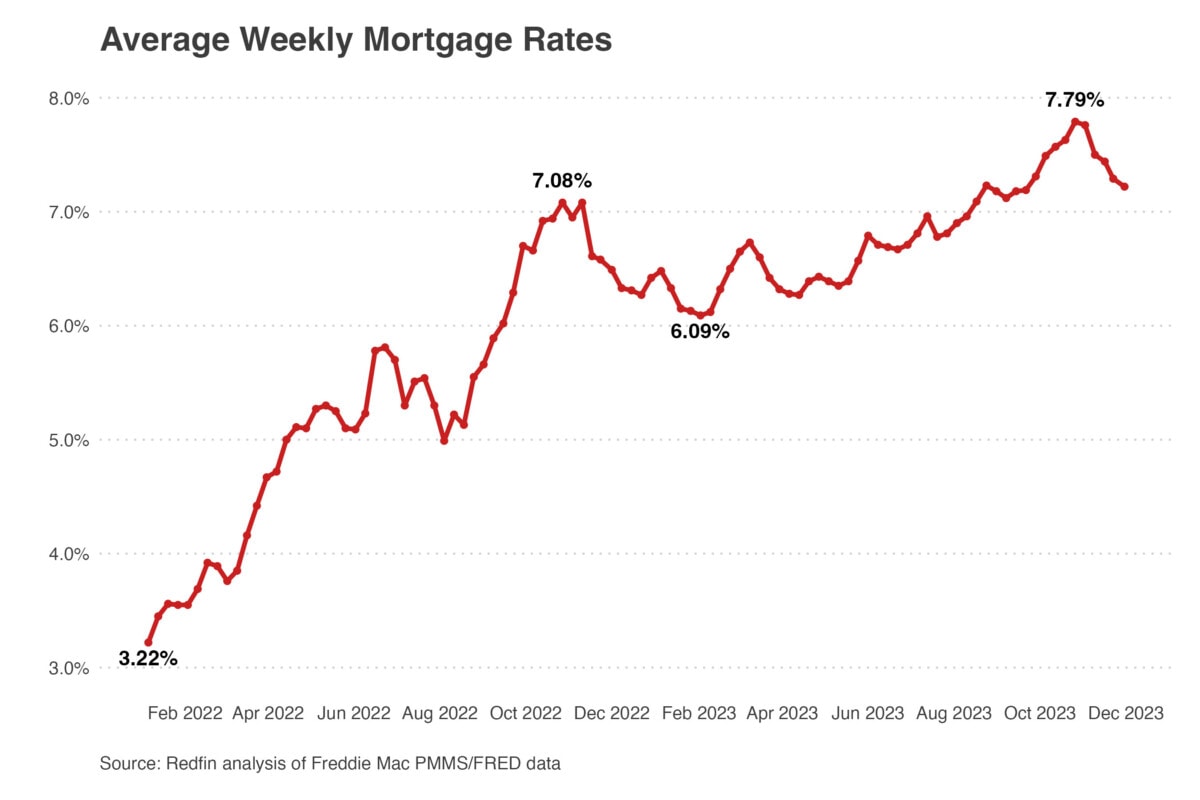

6. Mortgage charges ballooned past 8% for the primary time in over 20 years

“Mortgage charges have been the secret this 12 months as report inflation helped push every day common 30-year fastened charges previous 8% for the primary time since 2000, pricing many patrons and sellers out of the market,” says Fairweather. “Residence patrons didn’t wish to pay twice as a lot for a house than they’d have three to 4 years in the past, and residential sellers didn’t wish to hand over their pre-pandemic charges.”

Greater mortgage charges impacted affordability throughout the market, straining already sapped budgets. In July, the typical month-to-month mortgage fee reached $2,637 and grew greater than twice as quick as wages (12.6% in comparison with 5.2%). Each have been report highs. Affordability (or lack thereof) additionally immediately impacts housing inequality, which is wider now than it was within the Sixties.

Importantly, mortgage charges fell noticeably earlier than the tip of the 12 months as a result of inflation easing up, the Fed holding charges regular, and the labor market rising slower than anticipated. Whereas rates of interest aren’t predicted to fall till halfway by subsequent 12 months (three charge drops are predicted in 2024), mortgage charges may proceed to fall sooner.

“Wanting forward, whether or not rates of interest will fall depends upon two issues: the energy and resiliency of the economic system, and shopper habits,” notes Matt Birdseye, Govt Vice President at Bay Fairness, a Redfin firm. “Till unemployment rises and the economic system slows, charges are unlikely to fall.”

Simply 16% of properties have been inexpensive for the everyday family in 2023, probably the bottom for the foreseeable future.

Graph exhibits aggregated common mortgage charges, not every day charges, which is why the graph doesn’t depict the 8% excessive. Each day charges are extra variable.

7. Homebuyers trying to relocate favored solar and affordability

A report 26% of homebuyers regarded to maneuver to a unique metro space within the three months ending August 2023, up from 24% throughout the identical three months in 2022 and 25% firstly of this 12 months.

“Typically talking, the proportion of patrons trying to relocate was larger in 2023 than in 2022,” notes Chen Zhao, Redfin Senior Economist. “Regardless of purchaser demand falling total, those that regarded to purchase sought extra inexpensive areas to get extra for his or her cash.”

Surprisingly, the chance of pure disasters didn’t push dwelling costs down in lots of at-risk metros. “We count on this to alter within the close to future, although,” continues Zhao.

Lots of the prime migration hotspots have been sunny, extra inexpensive metros which grapple with extreme local weather dangers corresponding to warmth, drought, and flooding. This isn’t new; in actual fact, from 2021-2022, migration into probably the most flood-prone areas doubled in comparison with the prior two years. This comes as 2023 set a brand new report for billion-dollar climate disasters.

“It’s human nature to concentrate on present advantages over prices that would rack up in the long term,” admits Daryl Fairweather. “Briefly, the implications of local weather change haven’t totally sunk in. That is partly as a result of most owners don’t foot the invoice when catastrophe strikes. However as insurers proceed to tug out of disaster-prone areas, individuals could really feel a larger sense of urgency to mitigate local weather risks – particularly if their dwelling’s worth is susceptible to falling.”

The highest 5 hottest metros individuals regarded to maneuver to in 2023

MetroNumber of individuals trying to transfer to the realmLas Vegas, NV5,565Miami, FL5,240Sacramento, CA5,125Phoenix, AZ4,770Orlando, FL4,595

The highest 5 hottest metros individuals regarded to go away in 2023

MetroNumber of individuals trying to go away the realmSan Francisco, CA28,365New York, NY23,710Los Angeles, CA20,640Washington, D.C.15,590Louisville, KY5,195

Information is the % of Redfin.com customers trying to find properties exterior their metro. Information is the annual median combination of a number of three-month rolling aggregates. Sustain with the newest migration information right here.

8. Housing stock remained effectively under common

There was a mean of 1.015 million properties listed on the market each month in 2023, down 0.1% from final 12 months. Month-to-month stock peaked at 1.1 million properties, under 2022’s 1.26 million and much under historic normals.

Cincinnati (-41.9%), Newark (-24.3%), and New Brunswick (-21.9%) noticed the largest stock declines, with Chicago coming in fourth.

Mortgage charges have been the first motive why stock was so sluggish. Practically 1 / 4 of all owners had an rate of interest under 3%, and round 90% of householders had charges under 6%, main many would-be sellers to remain put to keep away from taking up a better charge.

Stock is calculated in rolling 90-day intervals, e.g., January 2023 knowledge is the three-month interval from November 1, 2022, by January 31, 2023. Redfin stock data date again to 2012.

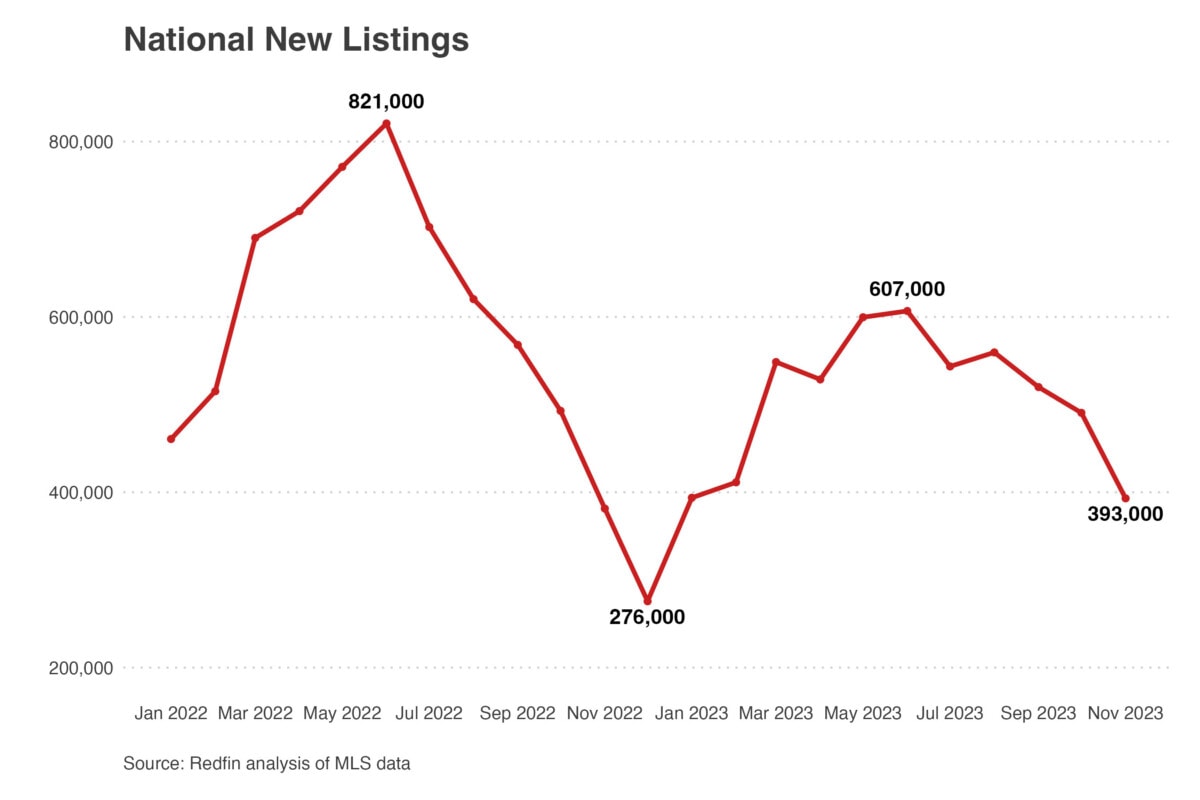

9. New listings dropped to their lowest stage on report

There have been simply 5.4 million new listings in 2023, the bottom stage on report and a large 16.4% drop from 2022. Common month-to-month new listings additionally posted sharp declines, falling from 585,000 in 2022 to 520,000 this 12 months.

New listings are one issue that make up whole housing stock. The dramatic drop in new listings was primarily as a result of skyrocketing mortgage charges, preserving patrons and sellers on the sidelines.

Yr over 12 months, new listings fell each month in 2023 till November, after they started to rise for simply the second time since July 2022. That very same month, in addition they posted their largest enhance since 2021 as mortgage charges fell to beneath 7.4%, effectively under the excessive of 8%. Listings continued to rise into December.

This 12 months, new listings have been additionally a significant factor in figuring out native market traits. For instance, new listings dropped a large 24% throughout New York State in 2023, inflicting a ripple impact. “The drop in new listings created a surge in competitors amongst patrons in search of inexpensive properties,” says Kimberly Hogue, a Rochester Redfin agent. “Sellers have been capable of profit massively in lots of Upstate markets as patrons competed over the few properties left, resulting in a spike in costs.”

Joey Keeler, a Redfin Premier agent in Seattle, agrees, however says that favorability depends upon the property. “Typically, our market favors sellers, nevertheless it depends upon the itemizing,” he says. “Some well-priced properties can see a number of bidding wars, whereas others could sit available on the market for weeks.”

New listings posted year-over-year beneficial properties to shut out the 12 months, offering hope for 2024.

New listings are calculated in rolling 90-day intervals, e.g., January 2023 knowledge is the three-month interval from November 1, 2022, by January 31, 2023. Redfin listings data date again to 2012.

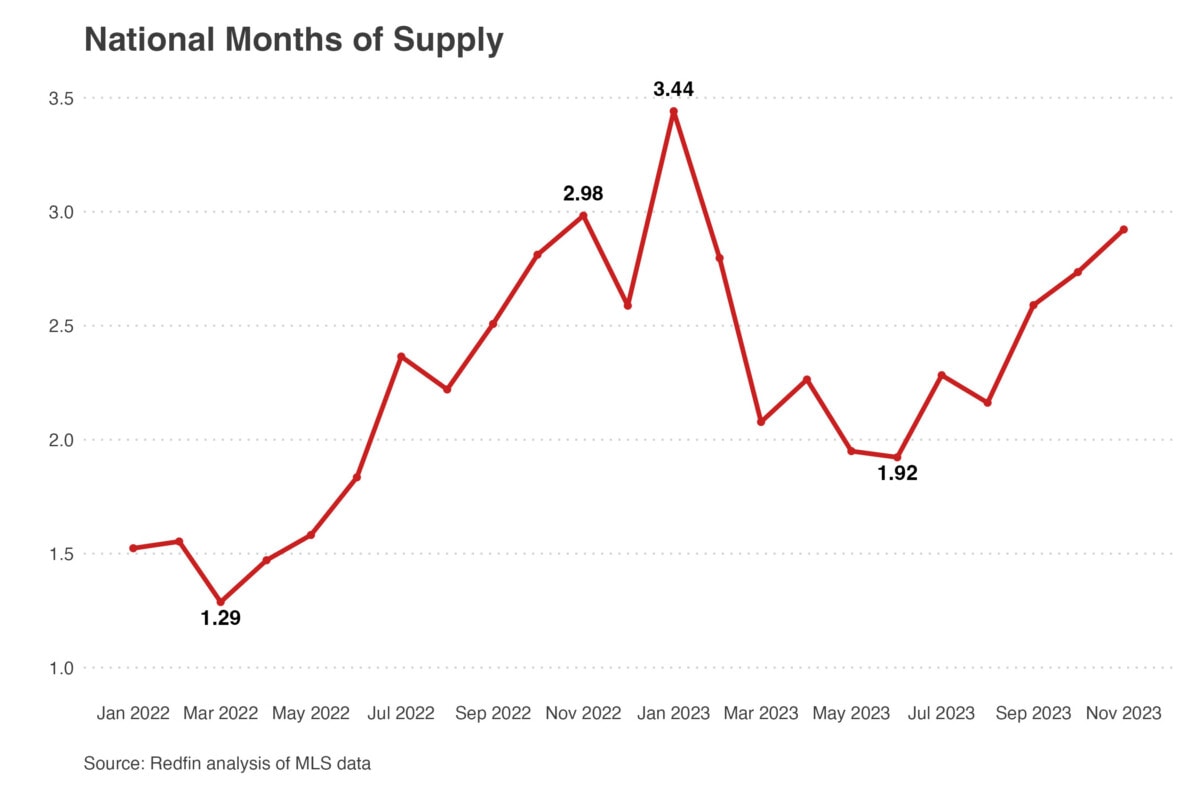

10. Months of provide reached 3.4 months, its highest stage since 2019

Whereas stock measures the variety of properties at present accessible on the market, months of provide measures the period of time it might take these properties to promote. Six months of housing provide is taken into account a wholesome benchmark, with fewer than six indicating a vendor’s market and greater than six indicating a purchaser’s market.

The typical inventory of housing provide throughout each month in 2023 was 2.4 months, up from 2.1 months in 2022.

Despite the fact that months of provide rose in 2023, it was nonetheless a really tight market; by the primary six months of the 12 months, simply 1.4% (14 out of 1000) of the nation’s properties modified arms, the bottom share in a minimum of a decade. The pandemic homebuying increase depleted provide, which has solely barely began to get well.

“Months of provide gained some floor this 12 months in comparison with final, reaching above 3 months in January, however nonetheless remained far under a balanced market,” provides Fairweather. “Nevertheless, native market traits decided whether or not or not patrons or sellers had a bonus.”

Months of provide grew at its quickest charge 12 months over 12 months in historical past in January earlier than falling till April.Despite the fact that months of provide started rising to shut out the 12 months, it nonetheless remained under a balanced market.

Provide is calculated in rolling 90-day intervals, e.g., January 2023 knowledge is the three-month interval from November 1, 2022, by January 31, 2023. Redfin provide data date again to 2012.

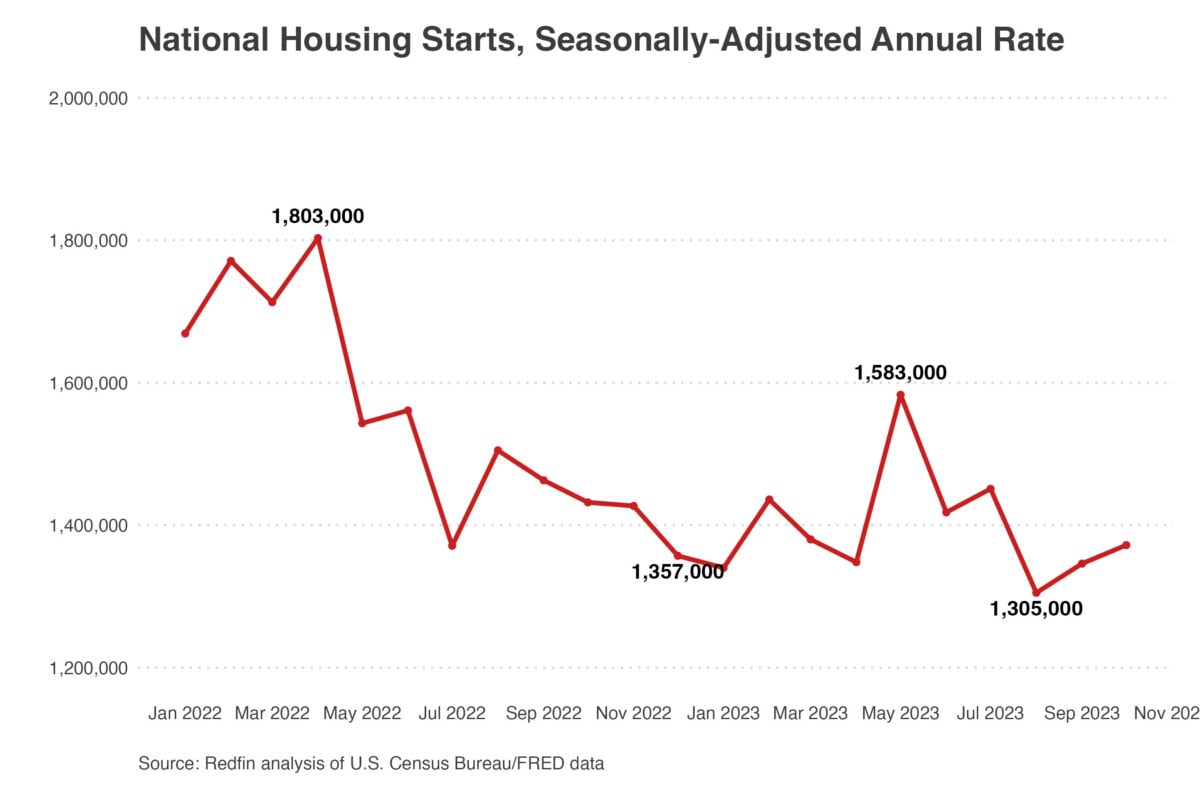

11. New building fell as builders have been left caught with inflated stock

There have been 1.41 million privately-owned new properties constructed within the U.S. by November 2023, down from 1.55 million in 2022.

Many dwelling builders who snatched up land throughout the pandemic to capitalize on the provision crunch have been left caught with properties they couldn’t promote this 12 months. It is a stark distinction from 2022, when new building blossomed following the pandemic provide crunch.

“In the event you’re a purchaser, take into account new building properties,” advises Kim Stearns, a Northern Idaho Redfin agent. “Due to a list buildup, many builders have one to 4 properties they’d love to shut on and can usually supply incentives.”

New building slowed earlier than rising later within the 12 months, as inflation cooled and extra homebuyers entered the market. Specialists predict new building will proceed rising into subsequent 12 months.

Over 73% of latest builds have been single-family properties, up 8% 12 months over 12 months.

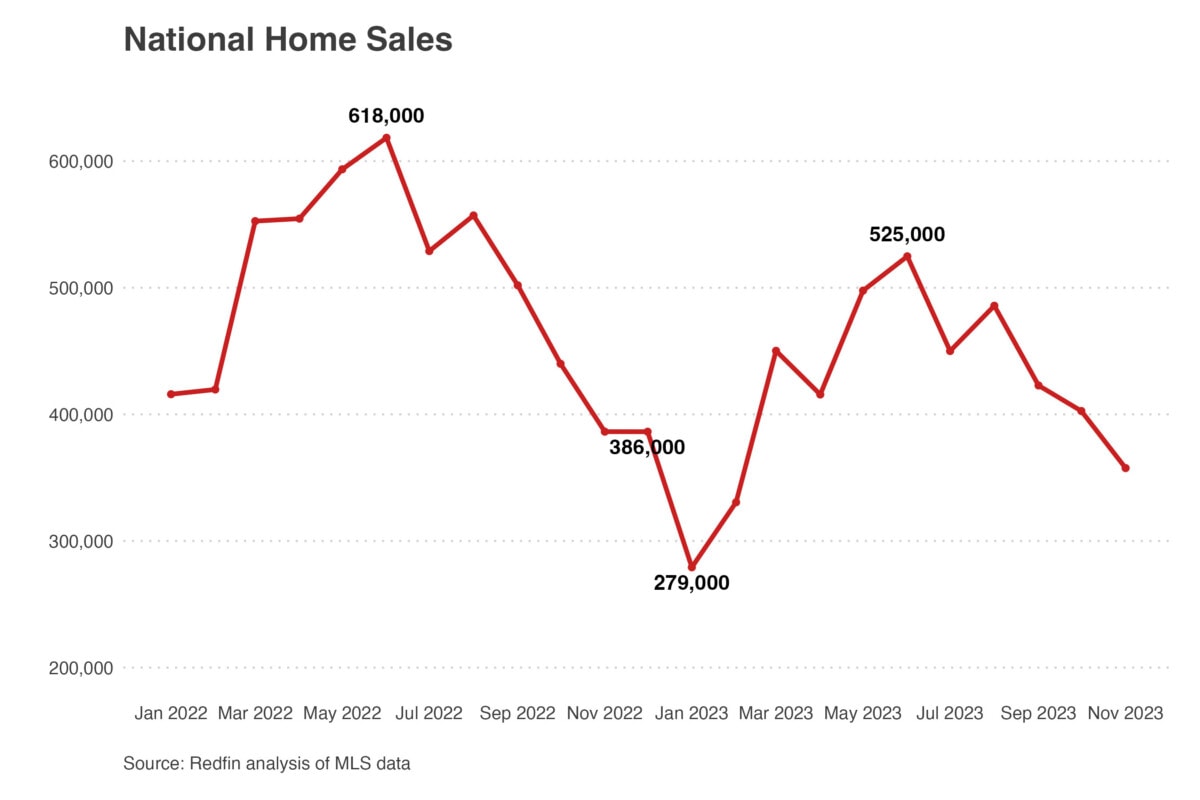

12. Residence gross sales fell greater than 18%, hitting report lows

Simply 4.59 million U.S. properties offered by November, an unimaginable 18.3% drop from the 5.62 million offered in 2022 throughout the identical interval.

Yr-over-year dwelling gross sales have been destructive each month in 2023. Nevertheless, the declines shrunk from a low of -37.5% in January to only -4.8% in November, displaying a promising upward development main into 2024.

Sadly, current dwelling gross sales, a measure of what number of properties which have offered a minimum of as soon as are anticipated to promote in a 12 months, have fared a lot worse. Basically, between 4 and 7 million current properties promote per 12 months, with the historic common sitting at simply over 5 million. In 2023, specialists predict simply 3.82 million current dwelling gross sales, a 7.3% drop from 2022 and the lowest annualized quantity since August 2010.

Simply 278,000 properties offered in January, the bottom quantity since 2012.In Could, the variety of lively listings dropped to 1.4 million, its lowest stage on report. Fewer listings helps enhance bidding wars and additional deter patrons, impacting gross sales. Whereas pending gross sales rose in November, closed gross sales fell by at a report charge to shut out the 12 months.

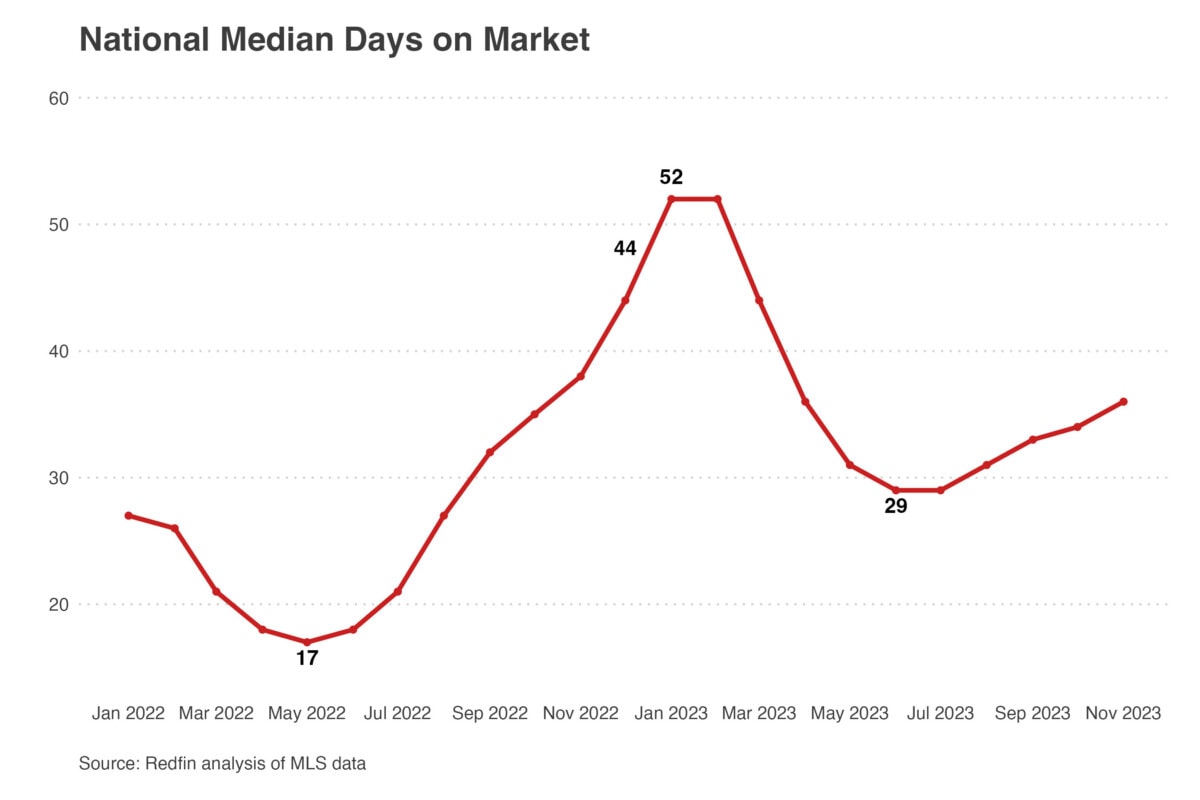

13. Median days on market soared past one month because the market cooled

In 2023, properties spent a mean of 37 days available on the market, a full ten days greater than 2022.

Provide began dropping dramatically throughout the pandemic as a result of provide chain points, rising demand, and a continual lack of homebuilding. Nevertheless, provide started inching upwards half method by 2022, as mortgage charges rose and fewer individuals entered the market.

In 2023, slowly rising provide paired with excessive dwelling costs and mortgage charges led to a rise in time on market in most metros. Nevertheless, extra inexpensive areas noticed the alternative impact; halfway by 2023, homes in Buffalo and Rochester offered over six instances quicker than properties in Austin.

“Stock for Austin is at present sitting at an 8-year excessive, which corresponds with a rise in time on market,” observes Chris Daniels, a Redfin Gross sales Supervisor in Austin. “Stock has climbed step by step all through 2023, however many indicators are pointing in the direction of this being the height as a result of decrease mortgage charges luring individuals again to the market.”

June and July have been the busiest months of the 12 months, with properties spending 29 days available on the market.By far, the slowest month was January, with properties spending a mean of 52 days available on the market.

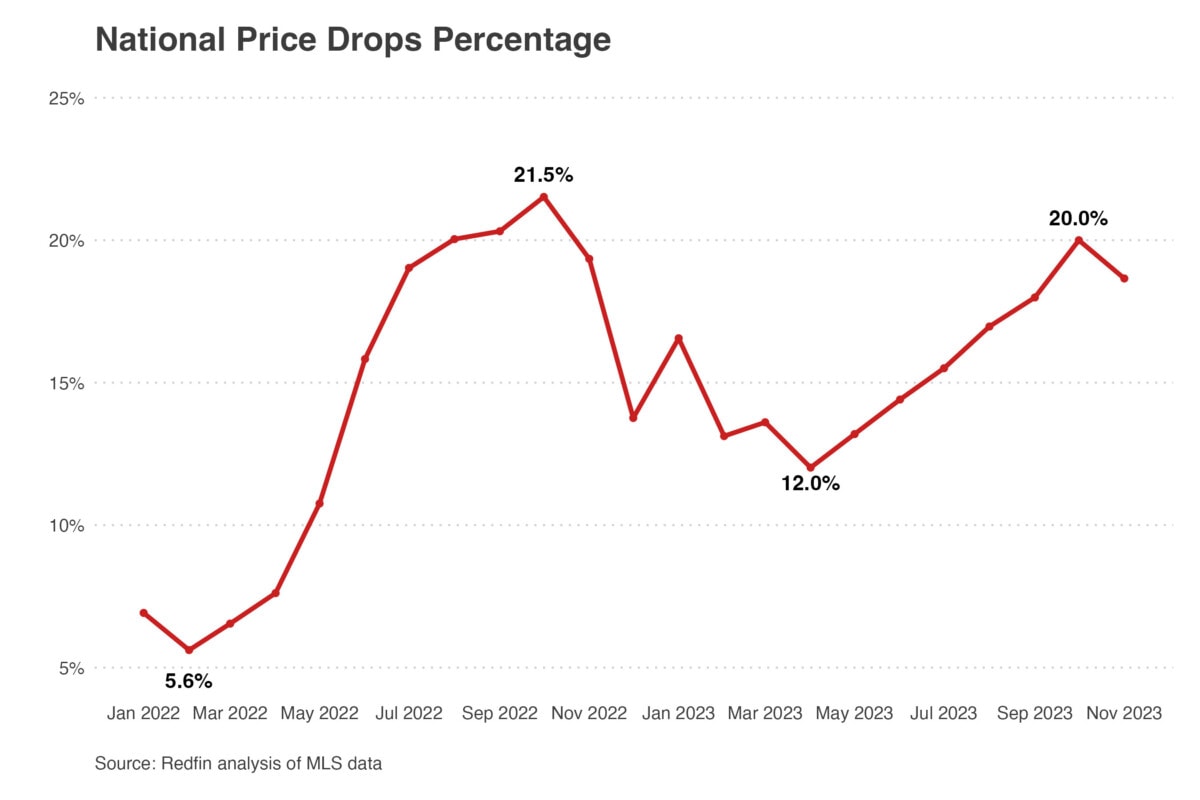

14. 15% of lively listings skilled worth drops

15.3% of listings skilled worth drops in 2023, up from 13.9% in 2022.

As affordability worsened and fewer patrons entered the market, extra sellers have been pressured to decrease costs. In some markets, sellers additionally needed to supply further concessions as a result of very restricted demand. In reality, by November, greater than one-third of all dwelling sellers gave concessions – down from the report 45.6% in February however up from 27.6% two years prior.

“A good way patrons can decrease the price of a house is thru vendor concessions and buydowns,” advises Mike S. Rafii, a Regional Gross sales Supervisor at Bay Fairness. “A standard method to do that is by negotiating vendor concessions to incorporate cash towards the client’s closing prices. The customer can then use this cash to purchase down their rate of interest – both completely (for the complete mortgage time period), or quickly (for as much as 3 years).”

In lots of markets, sellers have to do all the pieces they will to safe a purchaser. “To make a property extra interesting, sellers have to have their properties in pristine situation to draw patrons,” suggests the Redfin Premier brokers in Las Vegas. “In Las Vegas, sellers needed to do all the pieces beneath the solar, from paying closing prices to providing repairs, to get a luxurious purchaser this 12 months.”

On common, worth drops remained extra frequent than any 12 months on report, as restricted affordability hampered patrons’ budgets. Of all sellers who dropped their unique itemizing costs in 2023, the typical vendor dropped costs by 4.5%.

The highest 5 metros with the very best share of worth drops in 2023

Information contains the aggregated common share of worth drops out of all lively listings in every of the 50 largest metropolitan areas.

15. Practically 33% of properties have been bought with money in 2023

32.7% of properties have been bought with all money in 2023, up from 30.7% final 12 months and the highest share in a decade. Nevertheless, whereas the share of all-cash purchases continued rising, the variety of money gross sales fell 12 months over 12 months alongside all different gross sales metrics.

Prosperous dwelling patrons who can afford to pay money are extra apt to purchase when mortgage charges are excessive. By paying all money, they keep away from rates of interest altogether and safe a greater deal. Whereas these are useful advantages, in addition they exacerbate inequality between individuals who personal properties and individuals who don’t.

Money purchases have been particularly frequent at larger worth factors. “The posh market skilled a big inflow of money patrons this 12 months, as a result of larger mortgage charges,” notes Jonathan Huffer, a Redfin Premier agent in Palm Seashore.

In September, 1 in 3 homebuyers have been paying all-cash, the very best share since 2014. Cheap metros and prime migration locations noticed the very best share of money purchases.Lots of the costliest metros noticed the fewest all-cash purchases, together with Oakland (17.3%), San Jose (19.1%), and Seattle (20.4%).

The highest 5 metros with the very best share of all-cash purchases in 2023

Information is from a Redfin evaluation of county data throughout 39 of probably the most populous U.S. metropolitan areas, courting again by 2011.

16. Luxurious dwelling gross sales skilled their largest year-over-year decline on report

In 2023, there have been 549,750 luxurious properties offered, down 23.8% 12 months over 12 months.

In January, luxurious dwelling gross sales fell a report 45% to their second-lowest stage ever, persevering with a fast decline from 2022. Yr-over-year gross sales remained destructive each month, however slowly rose because the 12 months went on. A mean of 53,200 luxurious properties offered per 30 days in 2023, down 10.5% 12 months over 12 months.

Whilst gross sales fell, luxurious home costs continued to develop this 12 months, topping $1.15 million in September, a brand new report and better than any level in 2022. Nationwide, luxurious dwelling costs grew almost thrice quicker than non-luxury costs however dropped in costly metros as individuals migrated to extra inexpensive areas.

Greater costs additionally meant much less competitors. “Greater costs weeded out many patrons within the luxurious market and dropped competitors nationwide,” notes Sam Chute, a Redfin Premier agent in Miami. “Nevertheless, properties that did promote usually offered rapidly.”

Luxurious properties are outlined as the highest 5% of listings by worth in a given market. Values are three-month rolling aggregates ending on the date proven, e.g. November 2023 spans September, October, and November 2023. Information doesn’t embody the three months ending December 31.

17. Bidding wars fell in 2023

51.6% of properties had a bidding battle in 2023, down from 54% in 2022. Basically, bidding wars have been dropping as mortgage charges have elevated. This has been particularly pronounced in pandemic boomtowns.

In lots of markets, bidding wars have been nearly nonexistent. “As a consequence of excessive mortgage charges and low competitors, patrons didn’t really feel as a lot strain to compete,” notes Desiree Bourgeois, a Detroit Redfin agent. “Sellers have to know that patrons are much less tolerant of an overpriced dwelling.”

Fort Price (-23%), Austin (-17%), and San Antonio (-15.6%) noticed the most important decreases in bidding wars 12 months over 12 months.

The highest 5 metros with the very best share of bidding wars in 2023

Redfin defines a bidding battle as when a house faces a minimum of one competing bid.

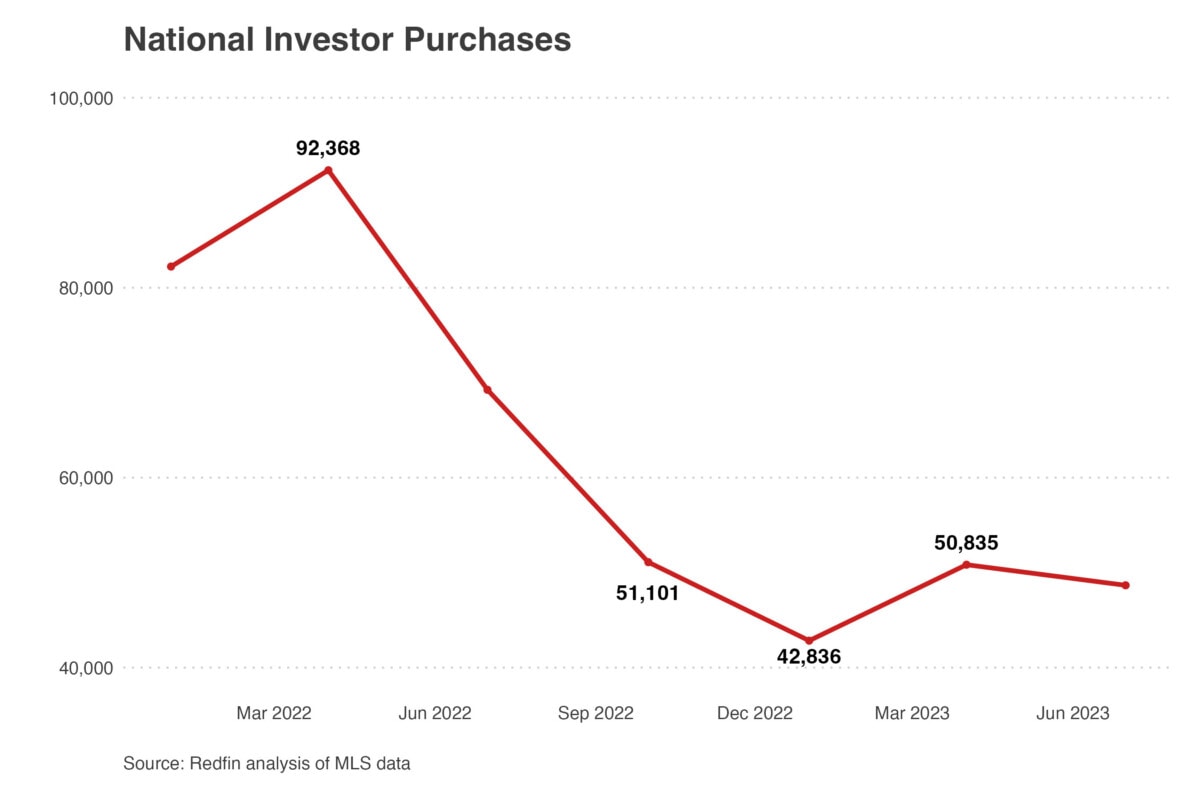

18. Traders purchases dropped at a report charge

Investor purchases plummeted by a report 48.6% 12 months over 12 months within the first three months of 2023, which adopted a 46.2% fall on the finish of 2022. Each drops exceeded the earlier 45.1% report fall throughout the 2008 subprime mortgage disaster. (Investor buy data date again to 2000.) Nevertheless, investor market share remained comparatively secure all year long, hovering round 17%, under final 12 months’s 19%.

The drop in purchases continued till the final quarter of 2023 however eased barely as mortgage charges started to stabilize. Investor exercise isn’t anticipated to rebound within the close to future.

These sharp drops got here simply months after the report surge in investor exercise that occurred within the aftermath of the pandemic. In reality, the entire most dramatic falls occurred within the Solar Belt, the place investor exercise jumped probably the most post-pandemic.

Atlanta, one of many prime metros for buyers final 12 months, noticed a 60% lower in investor purchases, the most important fall within the nation – however issues are beginning to search for. “Following a decline for many of those previous two years, investor exercise has ticked up in Atlanta,” says Angie Lawson, a Redfin agent in Atlanta. “They’re now focusing extra on shopping for land, flipping properties, and buying properties for rental earnings.”

Traders typically purchase properties both to promote or lease and capitalize on low building prices and excessive demand. Nevertheless, when prices are excessive and demand is low, buyers normally decelerate purchases. That’s what occurred this 12 months; excessive mortgage charges, a lackluster rental market, and rising dwelling costs left many buyers with properties they couldn’t promote or lease.

Multi-family properties continued to be the most well-liked amongst buyers, with single-family properties coming in second. A report 40.5% of all investor purchases have been starter properties (lower than 1,400 sq. toes).

The highest 5 metros with the most important investor market shares in 2023

Information is analyzed on a quarterly foundation and contains all property varieties except in any other case acknowledged. Information is thru September (Q3).

Wanting ahead

The 2023 housing market was laborious for a lot of owners and renters, however what does Redfin predict for 2024? Learn our 2024 Housing Market Predictions to be taught extra.

.jpg "Shares that may see motion as we speak: December 28, 2023")