Kameleon007

By Padhraic Garvey, CFA, Regional Head of Analysis, Americas and Benjamin Schroeder, Senior Charges Strategist

US yields are off their highs, and we doubt the temper is there to maneuver increased instantly. Inflation knowledge to resolve

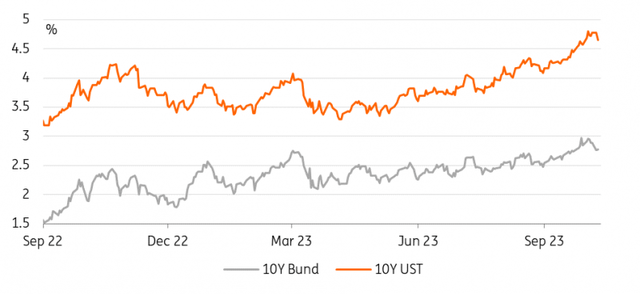

The US 2-year is now again to ranges first seen in June this yr when the funds charge was 25bp decrease. The ten-year is off its latest highs, however nonetheless virtually 80bp above the place it was in June. The curve has clearly steepened over this era.

Issues have modified because the weekend although. The bear market bubble has burst within the 10-year, and the market has downsized the speed hike danger forward. Inflation readings within the subsequent couple of days could have a say, with month-on-month readings nonetheless coming in a tad scorching on the CPI. That’s the most definitely impulse for resumed upside to yields.

Attention-grabbing that the 3-year public sale tailed yesterday. There was a robust market on the time, which can assist to tame negatives from this. However on the similar time, the oblique bid (which incorporates central banks) was remarkably subdued, which is indicative of comparatively weak end-investor demand.

All eyes clearly stay on the tragic scenes out of Israel, and there may be deep concern over what’s to return. Doubtless this story goes quiet for some time, but it surely’s clearly removed from over. Extra probably the start, the truth is, given the voices out of Israel.

Even when it stays localised, there might be concern that it turns into a lot larger and extra harmful. That may stay a rationale for core bond yields not straying an excessive amount of increased from right here. They’re at the moment effectively off latest highs (extra so within the US), and the temper for attaching 5% has waned.

There’s a 4.5% danger forward for the 10-year, until the inflation knowledge is excessive sufficient to trigger a reversal increased in yields.

The Bond Bear Market Bubble Has Burst (Refinitiv, ING)

At the moment’s occasions and market view

Though the flight-to-quality transfer has abated, the US CPI knowledge forward may nonetheless be motive sufficient for some to remain on the sidelines. We’ll already get the US PPI knowledge at present and, within the night, the minutes of the final Federal Reserve assembly, the place charges have been saved on maintain however projections have been considerably raised. We will additionally anticipate a variety of feedback from central bankers popping out of the IMF/Worldbank conferences in Marrakech. The primary focus within the eurozone with an in any other case empty calendar would be the European Central Financial institution client expectations survey on inflation.

In authorities bond major markets, Germany is lively with 30-year faucets, and later, the US Treasury will faucet its 10-year word.

Content material Disclaimer

This publication has been ready by ING solely for data functions no matter a selected consumer’s means, monetary scenario or funding goals. The knowledge doesn’t represent funding advice, and neither is it funding, authorized or tax recommendation or a proposal or solicitation to buy or promote any monetary instrument. Learn extra.

Authentic Put up

Editor’s Notice: This text covers a number of microcap shares. Please concentrate on the dangers related to these shares.

| Looking for Alpha")

")