Kameleon007/iStock by way of Getty Photos

By Brian Nelson, CFA

The whole lot is relative with regards to sovereign well being. The power of a sovereign rests partly on its capability and willingness to proceed to pay its money owed and meet its future anticipated liabilities. To take action, sovereigns usually might have to “print cash” at instances to handle the budgetary cycle. The downside of “printing cash,” nevertheless, is the danger of inflation and ensuing weak point of their forex.

If a sovereign’s forex stays sturdy relative to a basket of different currencies, nevertheless, there could also be little danger that the sovereign is not going to meet its future anticipated liabilities. In any case, the sovereign can preserve “printing cash” to fulfill such liabilities as they arrive due and generate little impression on the well being of its currency–and little change to the buying energy of its forex on the world stage.

To a big diploma, this “cash printing” then turns into net-neutral. Although there could also be a lot that goes into assessing the credit score well being of a sovereign, from our perspective, it usually boils all the way down to the view that the stronger a sovereign’s forex relative to different currencies, the negligible impression that “printing cash” to fulfill money owed will have–and due to this fact, the stronger its credit standing must be.

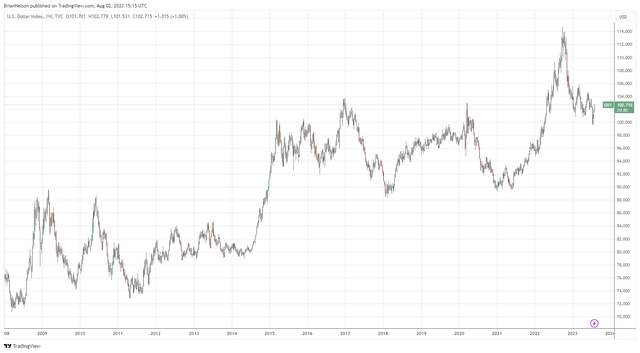

The U.S. Greenback Index has strengthened significantly because the Nice Monetary Disaster. (Buying and selling View)

On August 1, Fitch downgraded the credit standing of the U.S. one notch to AA+. Right here is the rationale:

The ranking downgrade of the US displays the anticipated fiscal deterioration over the following three years, a excessive and rising common authorities debt burden, and the erosion of governance relative to ‘AA’ and ‘AAA’ rated friends during the last 20 years that has manifested in repeated debt restrict standoffs and last-minute resolutions.

The power of the U.S. greenback, nevertheless, is plain and stays a secure haven, in our view (see picture above). One solely has to suppose again just a few months when many market individuals have been touring the world utilizing sturdy U.S. {dollars} to buy overseas items and leisure on a budget. For a sovereign to expertise weakening monetary well being, we’d anticipate that to present itself in a weakening forex as investor property flee the nation looking for different currencies, however the U.S. stays the place to be with regards to the worldwide stage. Fairly merely, U.S. fairness returns, as measured by the market-cap weighted S&P 500 (SPY), have dominated the worldwide stage, and we do not anticipate that to vary anytime quickly.

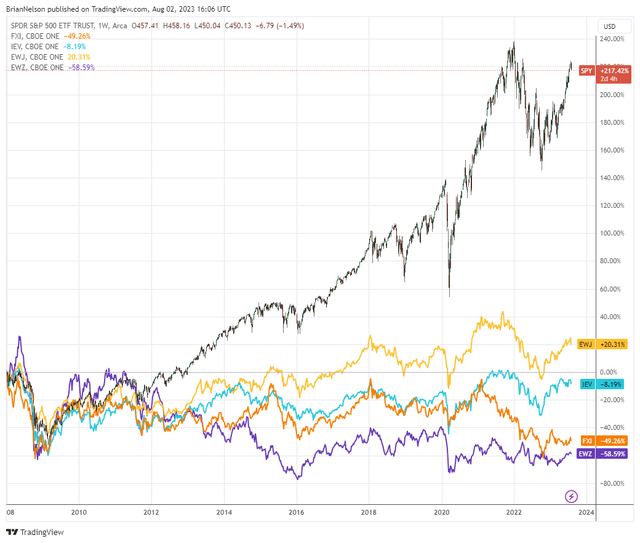

The U.S. markets (high) have trounced European, Chinese language, Japanese, and Brazilian equities because the Nice Monetary Disaster. (Buying and selling View)

Although many consider gold (GLD) and Bitcoin (BITO) could also be viable options to the U.S. greenback, each gold and Bitcoin lack what’s wanted in a reliable forex. For one, you possibly can’t purchase groceries on the native grocery store with gold, and companies usually do not settle for cryptocurrencies for cost given their volatility and the uncertainty surrounding the SEC’s crackdown on a lot of them as securities. Gold and Bitcoin additionally do not generate future anticipated free money flows, so estimating their intrinsic values turns into a really tough proposition. In lots of respects, each gold and Bitcoin are “higher idiot” property as most personal them for worth appreciation (diversification) potential, to not conduct enterprise. Their costs are then extra a mirrored image of what any individual else can pay for them than anything. A inventory, then again, is exclusive.

Not like different investments similar to classical artwork, nice wine, or classic baseball playing cards, for instance, shares signify a declare on all of the property of the corporate, significantly their future enterprise free money flows. Whereas the costs of a uncommon Picasso, the most effective Bordeaux cash can purchase, or an genuine, gem-mint Cracker Jack “Shoeless” Joe Jackson could also be nearly totally primarily based on what another person can pay for them, shares are totally different, and it’s on this distinction that enterprise valuation is distinguished from speculative, illogical frenzy. Shares can even have intrinsic financial worth, along with what somebody can pay to take it off your palms.

Now that isn’t to say that intrinsic worth estimation just isn’t half artwork and half science–both arguably of equal importance–but it’s the very concept {that a} share of inventory isn’t just a chunk of canvas or cardboard or a fermented grape that very a lot issues. For one, a nice Picasso can not intrinsically generate enterprise free money flows, a Bordeaux can not both, nor can one of the crucial sought-after treasures of the 1914/1915 Cracker Jack baseball card assortment. As a result of a inventory is an possession declare on an organization’s property (and, by definition, these very property’ future enterprise free money movement stream), a inventory has tangible financial worth, no matter one’s opinion of the corporate.

Within the case of shares, intrinsic value–not to be confused with price–is due to this fact not all the time within the eye of the beholder. A greenback of enterprise free money movement generated by the corporate rightly belongs to the shareholders, and it’s due to this that shares will not be, in substance, simply items of paper, whilst this truism could also be obscured throughout manias or in instances of panic, when ranks of the grasping or fearful develop, respectively. Somewhat, shares have intrinsic, financial and foundational price. Shares generate money (i.e. free money movement), and this can be a large distinction between them and different investments that don’t (supply: Worth Entice, used with permission).

As we take into consideration Fitch’s downgrade of the credit standing of the U.S., we do not essentially disagree that the flexibility of the U.S. to pay its money owed has develop into extra convoluted given rising future anticipated liabilities, a better rate of interest on these liabilities (given charge hikes), and uncertainty concerning the willingness to fulfill its money owed in mild of the seemingly endless debt ceiling debates which have gone to the deadline. We perceive that there is extra danger right now than earlier than, however buyers should not fear a couple of very, very modest enhance in an assessed chance of the U.S. technically defaulting on its debt. The ranking of a AA+ is definitely an excellent one, and the distinction between a AAA and AA+ is kind of negligible within the grand scheme of issues.

For us, we expect the AAA ranking that must be downgraded is definitely a company within the type of Johnson & Johnson (JNJ). The corporate holds a web debt place, has unsure talc liabilities, in addition to issues concerning its split-off of Kenvue (KVUE). How the U.S. can now have a AA+ ranking whereas J&J can proceed to sport a AAA ranking speaks to the subjectivity of credit score rankings, themselves. AAA-rated firms ought to match the invoice extra like a Microsoft (MSFT), which has AAA company credit standing thanks partly to its large web money place and large free money movement producing ability–two of a very powerful sources of cash-based intrinsic worth. Ranking sovereigns and ranking corporates are two various things, after all, however the ranking, itself, usually measures chance of default. J&J’s chance of technical default is larger than that of the U.S., in our view.

Although Fitch’s downgrade of the credit standing of the U.S. to AA+ might, in some ways, be warranted, as fairness buyers it is essential to maintain all of it in context. What a AA+ ranking means relative to a AAA ranking is that there’s solely a minor–perhaps miniscule–higher assessed chance of a technical default of the money owed of the U.S. over the lengthy haul. Nevertheless, a have a look at the power of the U.S. greenback because the Nice Monetary Disaster speaks of a sovereign that maybe has grown stronger on the world stage, not weaker. Bear in mind, sovereign credit score well being is all relative, and until there could also be a rustic with a powerful democratic authorized system that emerges stronger and bigger than that of the U.S. whereupon the U.S. greenback is bought in droves, there’s little or no danger in the long term of a technical default by the U.S.–as it may simply preserve “printing cash.” With that stated, we do not disagree with Fitch’s ranking move–we simply need long-term fairness buyers to maintain it in context.

The U.S. fairness markets will possible have to take a breather after experiencing an enormous run larger up to now in 2023, and Fitch’s downgrade in all probability offers a purpose for some revenue taking, however we expect the sell-off will probably be short-lived. The 2 areas which have dominated returns year-to-date stay large cap tech and huge cap progress, and we anticipate these areas to proceed to carry out properly. Shares in these areas are likely to have incredible sources of cash-based intrinsic worth, together with giant web money positions on the stability sheet and robust expectations of free money movement era. If the markets are in any respect involved concerning the credit score well being of the U.S.–and reverberations within the credit score markets–the areas of massive cap tech and huge cap progress are secure havens. Many in these areas can proceed to run their companies successfully, even when the fairness and credit score markets have been to shut for years due to large stability sheets and appreciable free money movement era.

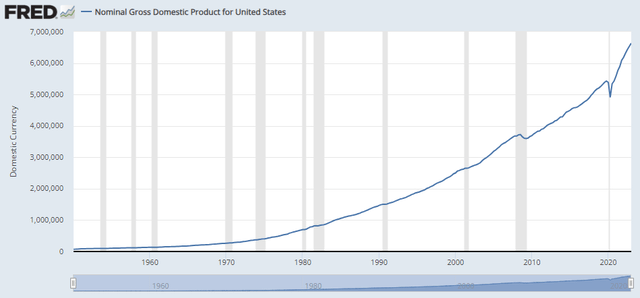

Nominal U.S. GDP continues to surge. (Worldwide Financial Fund, Nominal Gross Home Product for United States [NGDPSAXDCUSQ], retrieved from FRED, Federal Reserve Financial institution of St. Louis)

We just lately wrote an article about how buyers could also be excited about the P/E ratio and different valuation multiples incorrectly, because the asset-light nature of most of the market leaders right now from Apple (AAPL) to Alphabet (GOOG) (GOOGL) to Microsoft and past warrant higher-than-typical valuation multiples than up to now, particularly in mild of their large web money positions on the stability sheet. Internet money is an add-back to the current worth of estimated future free money flows within the enterprise valuation context, so we usually favor equities with web money positions over these with web debt positions. We additionally proceed to love what the catalyst of synthetic intelligence means for future free money movement era of massive cap tech and huge cap progress in coming years, whereas nominal GDP within the U.S. continues to growth larger (as proven within the picture above). We do not suppose Fitch’s downgrade of the credit score well being of the U.S. will derail this bull market, and we level to 5 of our favourite concepts to think about on this article.

")